Global| Feb 26 2021

Global| Feb 26 2021Japan's Industrial Sector Mounts a Comeback

Summary

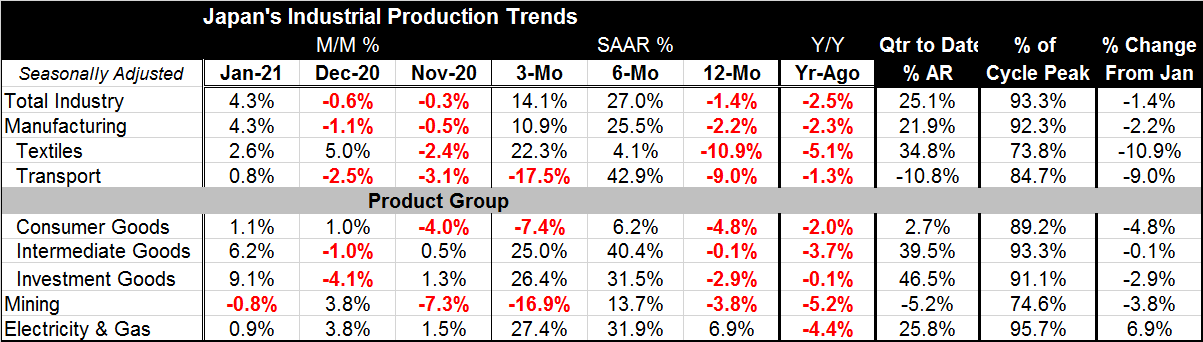

Japan's IP surged in January gaining 4.3% compared to December; that breaks a two-month slide in output. Total industry output is still lower by 1.4% over 12 months. The robust gain gets the new quarter off to a strong start with [...]

Japan's IP surged in January gaining 4.3% compared to December; that breaks a two-month slide in output. Total industry output is still lower by 1.4% over 12 months.

Japan's IP surged in January gaining 4.3% compared to December; that breaks a two-month slide in output. Total industry output is still lower by 1.4% over 12 months.

The robust gain gets the new quarter off to a strong start with output now rising at a 25.1% annual rate in Q1 2021.

All three main sectors of manufacturing showed gains in January led by the output surge in investment goods. There, output ratcheted higher by 9.1% month-over-month as intermediate goods output gained by 6.2% and consumer goods output rose by 1.1%. Each of these sectors has output higher month-to-month in two of the last three months. For consumer goods, the gains are back-to-back gains in January and December. For intermediate goods and capital goods, the gains are in January and November.

Mining shows a decline in January and a fall over the most recent three months as well as a year-over-year decline in output.

Utilities (electricity & gas) show a 0.9% rise in output in January as well as in the two preceding months. Utilities have not had three-monthly gains in a row like this since July 2018.

Japan's experience with the virus continues to hammer the economy, but manufacturing has been able to recover even in the grip of a lockdown. Infections peaked in Japan early in January then had a second less intense spike to a lover level at mid-month. The pace of infections fell off sharply through late-January and that has continued through February. The death rate curve followed this with lag generating the highest single day death toll on February 11. The death toll is now falling sharply.

Still, Japan had planned to extend its lockdown through the end of February. Japan will lift its COVID-19 state of emergency for six prefectures at the end of this month, but the Tokyo metropolitan area will have to wait for further signs that its situation is improving enough.

Most of the economy struggled against the virus and the various lockdowns in January. Retail sales values fell by 0.5% in January. Japan's housing starts fell by 3.1% and that was after falling by 9% in December. Core CPI prices in Tokyo fell by 0.3% in February. But as we have seen globally, manufacturing seems to be able to detach itself from virus issues and to continue to expand. In Japan, the extensive use of robots certainly aids in this effect. For example, Kawasaki Robotics started commercial production of industrial robots over 40 years ago. About 700,000 industrial robots were used worldwide in 1995, 500,000 of them in Japan (Source here). Robotics can help; however, even when the virus does not interrupt production directly, it can impact it by undercutting demand.

Japan is also one of the most robot-integrated economies in the world in terms of “robot density”—measured as the number of robots relative to humans in manufacturing and industry. Japan led the world in this measure until 2009, when Korea's use of industrial robots surged and Japan's industrial production increasingly moved abroad (Source here). Japan also had the second largest installation of robots globally in 2019, second only to China (Source here).

Most of Japan's economy has not fared as well while the virus abatement programs were engaged. The Economy Watchers index for January weakened and sits at a very low value. The Markit services index for Japan has slipped for two months in a row as of January and was last lower in August of last year. The Teikoku survey shows weakness in services, retailing and wholesaling.

Still, in the face of all that weakness, manufacturing has held up and recovered in January. But Japan is a global economy and it trades most with China and second most with the United States. Its factory sector will respond to international as well as to domestic conditions. In PMI terms, Japan's manufacturing sector has struggled. It has been contracting (below a level of 50) for its PMI manufacturing index for every month since April 2019 with the sole exception of a reading at 50 (dead neutral) in December 2020. That's 21 months without a monthly increase in manufacturing. Japan's manufacturing revival has been a long time coming. It will need more help if recovery is to continue. Continued progress on the virus is essential.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief