Global| Nov 16 2020

Global| Nov 16 2020Japan's GDP Springs Back to (toward) Life

Summary

Japan's third quarter growth result is a step in the right direction. Of course, it does not get Japan out of the hole dug in Q2 (…and Q1…and Q4). Japan has been struggling for some time with a variety of issues. Quite distressingly, [...]

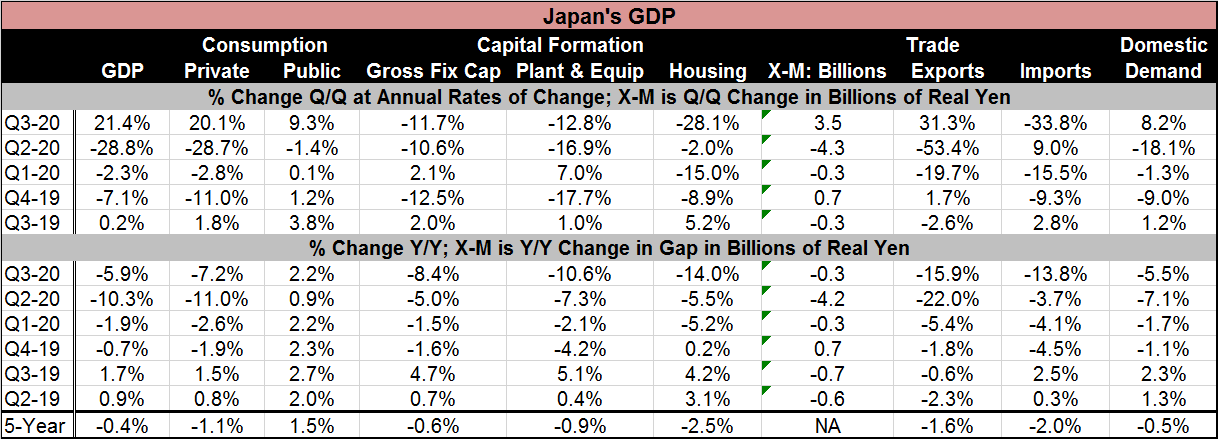

Japan's third quarter growth result is a step in the right direction. Of course, it does not get Japan out of the hole dug in Q2 (…and Q1…and Q4). Japan has been struggling for some time with a variety of issues. Quite distressingly, the five-year growth rate for Japan as of Q3 is a negative number (-0.4%). GDP in Q3 2020 is lower than it was in Q3 2015. Japan has been in a morass with its population shrinking and deflation lurking at the doorway and reeling as part of the ‘collateral damage' in the U.S.-China trade war. The coronavirus has been a sucker-punch to a convalescing patient.

Japan's third quarter growth result is a step in the right direction. Of course, it does not get Japan out of the hole dug in Q2 (…and Q1…and Q4). Japan has been struggling for some time with a variety of issues. Quite distressingly, the five-year growth rate for Japan as of Q3 is a negative number (-0.4%). GDP in Q3 2020 is lower than it was in Q3 2015. Japan has been in a morass with its population shrinking and deflation lurking at the doorway and reeling as part of the ‘collateral damage' in the U.S.-China trade war. The coronavirus has been a sucker-punch to a convalescing patient.

In Q3 Japan's private spending rebounded at a 20% annualized rate but only after it fell at a nearly 29% annualized rate in Q2. Public spending was a real source of stimulus as it rose at a 9.3% pace in Q3 after falling at a 1.4% pace in Q2. Capital formation continued to be a drag on GDP as it fell at a 10.6% annualized rate in Q2 and fell at a faster 11.7% pace in Q3. With a shrinking domestic economy and weak global demand, there is not much appetite for capital spending. Spending on both plant and equipment and on housing decline in Q3 on top of Q2 declines. For housing, the setback is at a substantially stepped up pace. For plant and equipment, the pace of decline is slightly less in Q3 than it was in Q2, but it is still negative in double digits. Japan's exports fell sharply in both Q1 and Q2 so that the Q3 expansion is not even close to offsetting the two-quarter decline. Imports rose in Q2, but had fallen in Q1 but then they turned to fall again in Q3 2020. Japan's domestic demand rose at an 8.2% annualized pace in Q3 but only after falling even faster in Q2 as well as in Q4 and having fallen for three quarters in a row. Clearly, Japan's weakness and struggles are about so much more than just the virus.

Looking backward over the last five years, every components of Japan's GDP in this table is lower over five years except public spending. Even exports and imports are lower on balance.

Japan certainly has a problem with the virus. Its infection curve and daily case load continue to rise and its count of active cases is higher too. Daily cases in Japan peaked on August 3 at 1,998. But as of November 15, they are rising and back up to 1,694. Except for the one day in early-August when daily infections peaked just below 2,000, in the last two days Japan has had the highest infection rates so far this year. Japan saw two previous peaks in the number of active cases: one peaking in April 29 and the other on August 12. The current active case load is above the April peak but below the August peak. However, it is still rising fast. However, the good news is that the daily death total in Japan is below the April and August peaks.

While Japan's infection rate is much lower than in other developed countries, it is still experiencing its own spread. Globally, the United States, the United Kingdom, Germany and Canada lead the count of new confirmed cases per million (population). All four of those countries still show sharply rising infection curves. Japan is not in their league. But the infection is still out-there depressing the international economic demand, consumer spending, income generation, and so on. The virus remains a global anti-economic event. The fact that it not being experienced so intensively in Japan does not make Japan immune from the broad collateral damage created by the virus and by national policies reacting to it. Japan is fortunate to not be hit harder by the virus directly, especially at a time that it clearly is dealing with so many other issues that have threatened and pummeled its GDP growth over the past five years.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief