Global| May 20 2015

Global| May 20 2015Japan's GDP Posts Upside Surprise; Ignore the Year-Over-Year Weakness

Summary

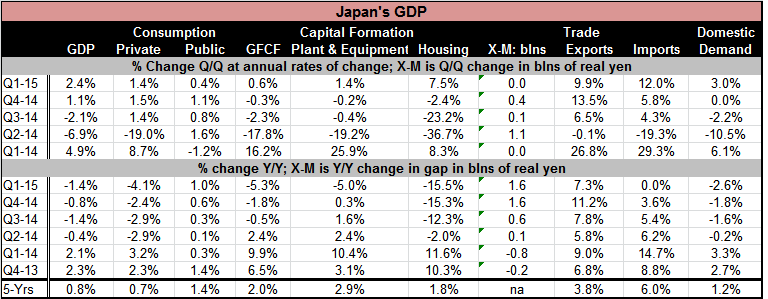

Japan's GDP rose at a 2.4% annual rate in Q1, better than expected. Still, the GDP components are uneven. This is Japan's strongest quarterly GDP rise in one year. One year ago GDP rose by 4.9% as it was boosted by spending ahead of [...]

Japan's GDP rose at a 2.4% annual rate in Q1, better than expected. Still, the GDP components are uneven. This is Japan's strongest quarterly GDP rise in one year. One year ago GDP rose by 4.9% as it was boosted by spending ahead of the announced consumption tax hike. That helps to explain why year-over-year Japan's GDP was weaker in Q1 2015 than it was in Q4 2O14 as GDP fell by 1.4% year-over-year. Next quarter Japan should post a very strong GDP result expressed year-over-year since it will compare GDP with the year ago quarter when GDP shrank at a sharp 6.9% annualized rate in the quarter.

Japan's GDP rose at a 2.4% annual rate in Q1, better than expected. Still, the GDP components are uneven. This is Japan's strongest quarterly GDP rise in one year. One year ago GDP rose by 4.9% as it was boosted by spending ahead of the announced consumption tax hike. That helps to explain why year-over-year Japan's GDP was weaker in Q1 2015 than it was in Q4 2O14 as GDP fell by 1.4% year-over-year. Next quarter Japan should post a very strong GDP result expressed year-over-year since it will compare GDP with the year ago quarter when GDP shrank at a sharp 6.9% annualized rate in the quarter.

Because of the year-over-year distortions, we will stick to the quarterly numbers to try to understand Japan's GDP evolution.

Private consumption rose at a 1.4% pace in Q1 after rising at a 1.5% pace in Q4. Public consumption slowed more sharply, rising at just a 0.4% pace compared to 1.1% in Q4. After three straight quarters of declines, gross fixed capital formation rose at a modest but positive pace of 0.6%. Investment in plant and equipment rose by 1.4% and housing investment expanded at a robust 7.5% annual rate.

The trade account was neutral in its impact on GDP, but exports grew at a still impressive 9.9% pace while imports were even more impressive, rising at a 12% annual rate. That pace is impressive because of the weakness in domestic demand, but Japan is still importing a lot of oil. Japan's total domestic demand did rise at a 3% pace in the quarter well short of supporting a 12% gain in imports.

On the whole, the quarterly GDP figures look pretty good. They pale when placed in a year-over-year format because of the adverse base-quarter when sales soared ahead of the consumption tax hike. Still, we look for further context to understand Japan's GDP.

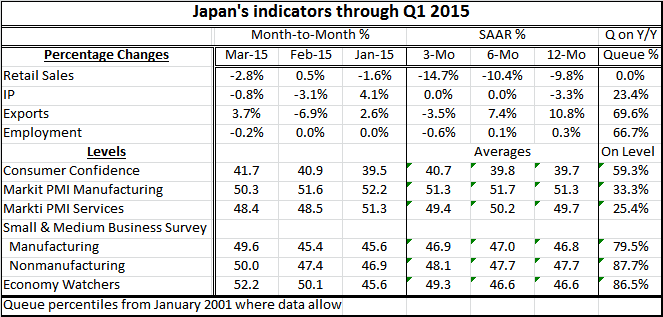

While GDP has consumption reviving in the quarter, the March retail sales change ranked in terms of its year-over-year performance is the worst result since January 2001. The industrial output year-over-year drop places it in the bottom quartile of all performance over the same period. Exports and employment each fare a bit better. Their year-over-year gains rank around the top third of their respective historic queues of data. While these are better sector results, they still are not impressive.

Consumer confidence is a diffusion reading and is below its neutral level of 50 in March as the first quarter ended. Still, that weak reading ranks in the top 40% of all confidence readings since January 2009. Manufacturing and nonmanufacturing PMIs are in the bottom one third to one quarter of their respective histories, but these histories date only from January 2010. Still, those are weak readings over this more recent time horizon. Small and medium sized businesses claim to be doing better in manufacturing and nonmanufacturing than the overall sector if we compare the respective queue standings. On this gauge, small businesses are doing quite well in Japan with 79- to 88- percentile standings. The economy watchers index, a services sector gauge, shows a stronger reading than does the services PMI. The economy watchers gauge has a much longer history for comparison than the services PMI (the PMI only extends back to January 2010, not January 2001).

On balance, Japan's GDP has made a better recovery in Q1 that we had expected. Still, the relevant indicators suggest there are still some considerable holes in that performance. We warn that next quarter's year-over-year GDP gain will look large because of its beneficial base for comparison. We continue to judge Japan as struggling. A few of the indicators in the table above have more recent readings available and none is showing a clear pick up in Q2 compared to Q1. While GDP had an upside surprise in Q1, its Q2 performance is still not in the clear.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief