Global| Aug 21 2017

Global| Aug 21 2017Japan's All-Industry Index Bounces Back in June

Summary

Japan's three main sectors industry (manufacturing), construction and tertiary (services) all show ongoing progress in June if not month-to-month, then in terms of trend. The chart on the left shows the indexes plotted in level [...]

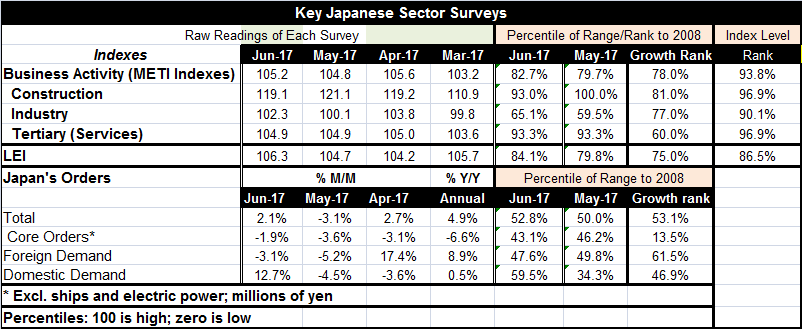

Japan's three main sectors industry (manufacturing), construction and tertiary (services) all show ongoing progress in June if not month-to-month, then in terms of trend. The chart on the left shows the indexes plotted in level format. The chart on the right shows them as year-on-year growth rates. The chart on the left (as well as the table below) shows some considerable recent 'turbulence' in the indexes themselves. They have moved up sharply, backtracked, and then recovered. As a result, the headline index of 105.2 in June is higher than in May but below its April reading yet strongly above its March reading of 103.2.

The headline index is up by 2.2% over 12 months which is less lift than in May or April but stronger than any other year-on-year gain back to March 2014. The message is clear and that is that Japan has a real revival in progress. That point should not be lost in the recent volatility of the readings. And that point is most clearly made by looking at the chart on the right that plots year-on-year rises in the METI sector indexes. Japan has its best multisector advances in place since later 2013 and early 2014. In 2013 and 2014, there was clear leadership by the construction sector. At this time, the construction sector and industrial sector are maintaining more or less equal gains with leadership changing hands depending on the month of observation. The services sector is making the sort of steady gains it is mostly known for.

In the table below, I present rankings of the indexes by index level as well as by year-on-year growth rates. The ranking on both bases are largely similar with the exception of the tertiary index. That is because the tertiary index tends to climb steadily over time; thus, its index standing is high, in its 93.3 percentile while its actual one-year growth rate is more midstream with a ranking standing in its 60th percentile. The industry index has an index standing in its 65th percentile with a growth standing in its 77th percentile. For that sector, the year-on-year growth is more impressive than the level of the index itself. Construction has a 93rd percentile standing for its index and an 81st percentile standing for its growth rate- both are strong readings. The differences more or less balance out for the headline where the index standing at its 82.7 percentile is quite similar to its growth rate standing in its 78th percentile.

The leading economic index has a slightly stronger index standing at its 84th percentile than its growth standing in its 75th percentile, but both are firm or strong readings. The June data on Japanese orders are less robust with index standings that are midstream at best and growth rates that range from middling to quite weak when ranked. Core orders have a growth ranking in their 13.5 percentile while overall orders have a 53rd percentile growth standing and nearly the same index standing.

On balance, these data show some upside to Japan's growth prospects. However, there is also some unevenness and the orders data suggest that there may still be some lingering weakness. The LEI suggests that growth is going to continue to move ahead more or less as it has been doing. The METI sector data, however, are having a relatively stronger run than the LEI suggests.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief