Global| Nov 11 2014

Global| Nov 11 2014Japan Loses Momentum

Summary

Japan's consumer confidence and economy watchers indices both have fallen in October. The economy watchers judgment of future conditions, their assessment of current conditions as well as their judgment on current employment [...]

Japan's consumer confidence and economy watchers indices both have fallen in October. The economy watchers judgment of future conditions, their assessment of current conditions as well as their judgment on current employment conditions all have slipped. The economy watchers index focuses on Japan's services sector.

Japan's consumer confidence and economy watchers indices both have fallen in October. The economy watchers judgment of future conditions, their assessment of current conditions as well as their judgment on current employment conditions all have slipped. The economy watchers index focuses on Japan's services sector.

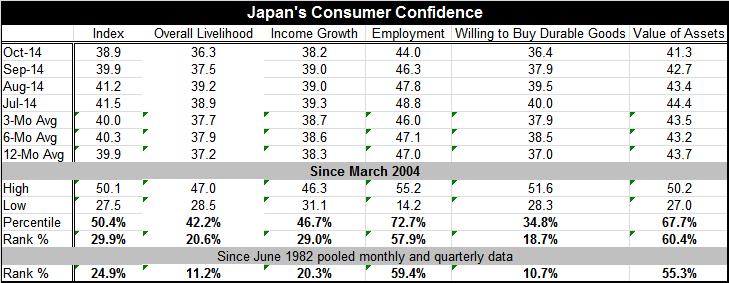

Consumer confidence continues to erode, having fallen for the third straight month in October. The confidence index fell to 38.9 in October from 39.9 in September. The assessment by households of their overall likelihood fell to 36.3 from 37.5. Income growth slipped to 38.2 from 39.0. Assessments of employment conditions fell to 44.0 from 46.3. The willingness to buy durable goods slipped to 36.4 from 37.9. Households' assessment of the value of their assets fell, too, to a reading of 41.3 in October from 42.7 in September.

We see slippage in all the main categories of consumer confidence in October. Not only have categories slipped but they currently reside at low levels historically. The bottom of the table ranks these various indicators in their longest time series back to 1982, which mixes in more modern monthly observations with the historical quarterly observations that the series used to employ.

On that basis, overall confidence stands in the lower quarter of its historic range, in the 24.9 percentile. Overall livelihood is in the 11.2 percentile, weaker only about 11% of the time. Income growth stands in its 20th percentile; historically employment growth is better off, as it stands in its 59th percentile and it's one of only two components standing above their respective historic medians, which occurs at the 50th percentile reading. The willingness to buy durable goods is also extremely low in the 10.7 percentile. Consumers assess the value of assets in the 55th percentile of their historic queue.

Japan's economy continues to struggle even as the Bank of Japan has just announced another round of stimulative quantitative easing. The notion that Prime Minister Abe may delay the second planned sales tax increase has excited Japan's financial markets. The Japanese economy is currently reeling from the first round of sales tax increases that are an attempt to increase government revenues and reduce the fiscal deficit as well as to reduce the accumulation of debt. Japan's debt as percent of GDP is massive. The attempt to end deflation and at the same time to cure Japan's long-term fiscal imbalance stemming from excessive public debt is proving to be a difficult exercise to pull off all at once.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief