Global| Sep 15 2004

Global| Sep 15 2004Japan: Demand for Credit "Less Weak" in Q2

Summary

The Bank of Japan today published "flow of funds" accounts for Q2. These comprehensive data are similar in structure to the Federal Reserve's accounts for the US. In Haver databases, the Japanese figures are maintained in the [...]

The Bank of Japan today published "flow of funds" accounts for Q2. These comprehensive data are similar in structure to the Federal Reserve's accounts for the US. In Haver databases, the Japanese figures are maintained in the "Financial" menus of the "JAPAN" database.

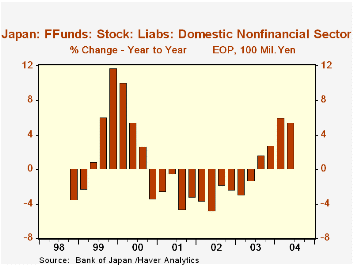

One of the hallmarks of protracted recessionary conditions in the Japanese economy from mid-2000 was a general contraction in financial values. The reduction in real economic activity and the general price deflation reduced the nominal amounts need to carry on business. This situation was most severe through mid-2002; it then began to turn around slowly. More forward-looking equity prices began to rise in the spring of 2003, leading in Q3 2003 to the first year-on-year gain in financial obligations of the nonfinancial sector since before the recession had started. This is evident in the first graph, which shows growth rates in liabilities outstanding; those increases have strengthened in the first two quarters this year.

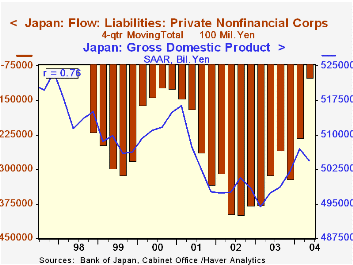

However, demand for financial resources in Japan is still not robust. In the second graph, the use of financial resources by private non-financial corporations is seen to continue shrinking. We can say, though, that the second-quarter's erosion in financial activity is the smallest in the seven-year history of these data. This could reduce the financial drag on economic activity; in the limited, 7-year history of these flow-of-funds data, the use of funds by private corporations in Japan has had a 76% correlation with nominal gross domestic product. While liquidation of liabilities probably shouldn't be interpreted as a "prop" to activity, the much reduced pace of this contraction surely lowers a barrier to renewed nominal growth. Households, though, remain shy about incurring new debt, and in fact have decreased their debt positions more rapidly so far this year than they did during 2003.

| Net New Liabilities, 4-Quarter Totals,Trillion Yen | Q2 2004 | Q1 2004 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|

| Domestic Nonfinancial Sector | 49.925 | 41.743 | 20.290 | -7.480 | 16.931 |

| Private Nonfinancial Corporations | -10.114 | -23.114 | -32.064 | -37.864 | -33.268 |

| Households | -4.362 | -4.143 | -2.846 | -8.738 | 0.320 |

| Memo: TOPIX Stock Price Index, EOP | 1189.60 | 1179.23 | 1043.69 | 843.29 | 1032.14 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief