Global| Dec 12 2016

Global| Dec 12 2016Japan Continues to Struggle

Summary

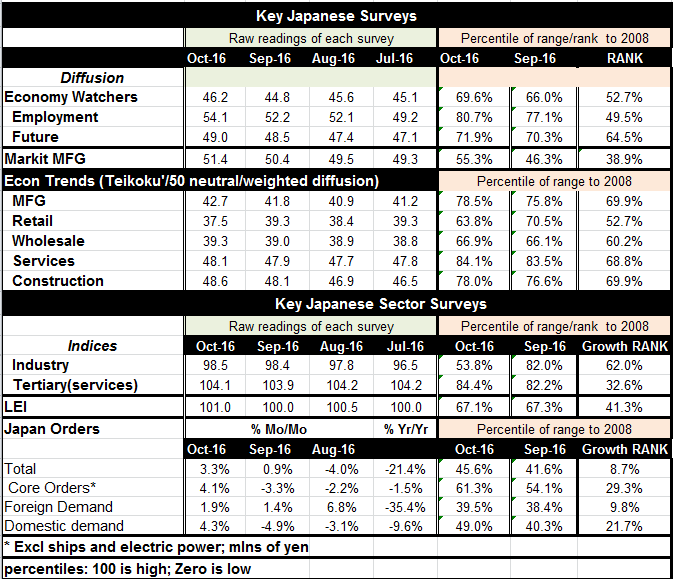

Japanese trends remain listless whatever their angle New readings today for Japanese orders and core orders as well as for its tertiary index (services) leave key trends in the doldrums. All of the surveys have different ways of [...]

Japanese trends remain listless whatever their angle

Japanese trends remain listless whatever their angle

New readings today for Japanese orders and core orders as well as for its tertiary index (services) leave key trends in the doldrums. All of the surveys have different ways of assessing the sectors. That makes them hard to compare. Teikoku and economy watchers indices are diffusion measures. The sector indices for industry and services are volume indices on levels of activity. Orders are nominal yen amounts express in yen terms. However, we achieve some degree of 'commonality' by taking each at its own method and presenting in the far right hand column where each topical reading ranks in its historic profile of data. On that method none of the measure is strong and the Teikoku (diffusion) indices have the relative strongest readings but all of those reside below their respective 70th percentiles... more ominously, all of the Teikoku readings are below the 50 mark. Regardless of their "standings", all the Teikoku readings refer to some degree of reduction in economic activity.

Still somewhat different assessments by different methods

The economy watchers diffusion indices which focus on the services sector show rank standings ranging from the 49th to 64th percentiles all very middle-of-the-pack readings. By comparison the Teikoku service sector reading is stronger; the economy watchers "strongest" index standing is for its outlook or future index. That reading is more comparable to Teikoku as it also has an upper 60th percentile reading. The topical economy watcher's current activity index shows contraction with a level of reading below 50. In terms of growth rates the sector indices show services (tertiary) at a low 32 percentile standing, quite weak although the industry ranking at its 62nd percentile is much closer to the Teikoku manufacturing 69th percentile standing. The Teikoku index assesses manufacturing as declining while the sector index actually has some slight growth year-on-year.

Orders are uniformly weak and dismal

The orders series is simply unique although it pertains to industry and manufacturing. It shows total orders at an 8.7% standing it terms of the ranking of its year-on-year growth rate (lower historically less than 9% of the time...); the less volatile core orders series elevates to a 29th percentile standing, still quite weak. Japan shows a weaker standing for foreign orders than for domestic orders. That is the impact of its relatively tight ties to China where economic conditions have slowed markedly.

Little optimism for Japan

This set of Japanese indicators does not show much that is upbeat either in terms of the levels of the readings or their respective momentum. Despite aggressive stimulus by the BoJ there is little to show for it at all in terms of activity, momentum or the inflation that the BoJ seeks to ignite. The Teikoku and economy watchers diffusion indices have too many of their readings that are below 50 (signaling contraction) to be taken as truly neutral news, although the ranking standings assign a more 'normal' standing to them. This is simply the result of Japan have been so weak for so long. Mild contraction has become normal in this nation where population is contracting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief