Global| Jul 28 2009

Global| Jul 28 2009Italy's Recovery In Confidence Continues... Still A Ways To Go

Summary

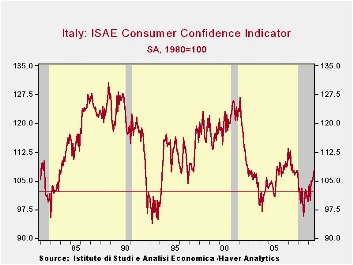

Confidence is UP! Consumer confidence in Italy is at its highest since November 2007. Still since January 1992 the reading stand is at the 40th to 41st percentile of its range and in terms of the ranking among all previous [...]

Confidence is UP! Consumer confidence in

Italy is at its highest since November 2007. Still since January 1992

the reading stand is at the 40th to 41st percentile of its range and in

terms of the ranking among all previous observations. This it is some

10 percentage points below its middle position in terms of range or

ranking percentiles. Ranking percentiles position a reading in a queue

of values while range percentiles position the reading in a range

bounded by the high and low readings. Both readings have some merit.

Past 12 month - Rating the past twelve

months, the overall situation is rates as a -68 which puts it in the

55th percentile in terms of rankings. Prices trends at -48 are the

worst in this period by either range of ranking methods.

The expected future - Looking ahead the

next twelve months overall situation is assigned a value of +2 leaving

it in the top 92nd percentile by ranking, but only the 65th percentile

according to the position of the reading in its range. Obviously among

all rankings this reading is relatively strong but there must be a

strong reading that lies at a much, much higher level to depress the

range reading so much. That would be a reading from June 2001, as from

April to Sept of 2001 readings on this score soared then dipped back to

a more normal range. Unemployment readings are still elevated at a +8

reading. That leaves the reading in the moderated 55th percentile by

range but at a much higher 94th percentile by ranking. Those two

readings tell us that the unemployment reading is rarely higher than

this but it has spiked much higher in the past. The response to the

household budget situation remains weak by any measure at a +1.

Current/Future comparisons - Households

assess their current and future situations as about to be much improved

in the next twelve months with their range and ranking percentile

readings rising from a bottom quarter or third position currently to a

50% to two-thirds position in the outlook. Current savings are

considered high, future savings are expected to be low. Similarly,

major purchase environment was construed as middling over the past

12-months abut is expected to improve sharply to top 4% or better in

the future.

Summing up - On balance these responses by

Italian households show a clear disappointment with past trends. In

that respect the expected future improvement is harder to read. Some of

the future readings are more middling some are strong. It is still not

clear if consumers simply are optimistic that things will improve from

the dregs of the last 12 months or if things are expected to improved

to true strong readings. As current conditions improve we will monitor

these future readings and see if they continue to show the strength

that some of the categories currently exhibit. If much better

conditions are expected then as the current readings improve the future

readings should remain high. If the future is simply expected to be

‘normal’ as the current situation normalizes the expectations readings

in the survey will recede to a region of boredom.

| Jul-09 | Jun-09 | May-09 | Apr-09 | Percentile | Rank | percentile | |

|---|---|---|---|---|---|---|---|

| Consumer Confidence | 107.5 | 105.4 | 104.9 | 104.9 | 41.3 | 126 | 40.3% |

| Last 12 months | |||||||

| OVERALL SITUATION | -68 | -68 | -73 | -74 | 63.2 | 93 | 55.9% |

| PRICE TRENDS | -48 | -40.5 | -45 | -43 | 0.0 | 211 | 0.0% |

| Next 12months | |||||||

| OVERALL SITUATION | 2 | -8 | -17 | -26 | 65.1 | 16 | 92.4% |

| PRICE TRENDS | 1.5 | 8.5 | 10 | 9.5 | 3.1 | 112 | 46.9% |

| UNEMPLOYMENT | 8 | 15 | 17 | 21 | 55.9 | 11 | 94.8% |

| HOUSEHOLD BUDGET | 1 | 0 | 5 | 1 | 17.0 | 199 | 5.7% |

| HOUSEHOLD FIN SITUATION | |||||||

| Last 12 months | -40 | -37 | -34 | -37 | 32.7 | 155 | 26.5% |

| Next12 months | -2 | -4 | -5 | -11 | 67.3 | 91 | 56.9% |

| HOUSEHOLD SAVINGS | |||||||

| Current | 60 | 60 | 59 | 60 | 72.7 | 13 | 93.8% |

| Future | -30 | -25 | -29 | -29 | 38.3 | 170 | 19.4% |

| MAJOR Purchases | |||||||

| Current | -40 | -39 | -43 | -41 | 42.1 | 99 | 53.1% |

| Future | 4 | 3 | 1 | 3 | 96.8 | 3 | 98.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief