Global| Mar 11 2014

Global| Mar 11 2014Italy and Europe Turn the Corner on Growth- But Slowly

Summary

Italian GDP edged up ever so slowly in the fourth quarter, registering a gain of 0.3% at an annual rate. Public consumption was up in the fourth quarter along with capital formation while net exports were a positive contributor as [...]

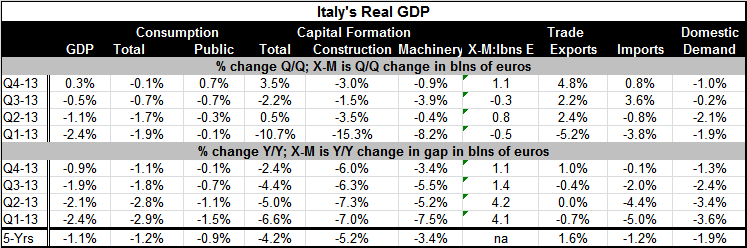

Italian GDP edged up ever so slowly in the fourth quarter, registering a gain of 0.3% at an annual rate. Public consumption was up in the fourth quarter along with capital formation while net exports were a positive contributor as exports outpaced imports. Still, on balance, domestic demand was negative.

Italian GDP edged up ever so slowly in the fourth quarter, registering a gain of 0.3% at an annual rate. Public consumption was up in the fourth quarter along with capital formation while net exports were a positive contributor as exports outpaced imports. Still, on balance, domestic demand was negative.

Looking at trends year-over-year, GDP is lower by nearly one percentage point over four quarters with total consumption down at a 1.1% pace, slightly faster than GDP overall. Public consumption is lower but only by 0.1%, buffering the decline of GDP. Capital formation is lower year-over-year by 2.4%. Construction is off a sharp 6%; however, like capital formation, it is declining at a slightly slower pace than it had been. Net exports are positive but have become a slightly less positive contributor to GDP as the year has progressed. Exports are up 1% over four quarters while imports are down by 0.1%. Clearly, part of the trade progress has come from weak GDP and the resulting restraint on imports. Over four quarters domestic demand is falling by 1.3%, but that too is showing a diminishing pace of decline.

On balance, there are not a lot of positive trends in the Italian economy, but there has been enough to create positive growth in the fourth quarter. There has been a one quarter turnaround in several of the GDP components and more broadly what we see are slower rates of decline year-over-year in many of the GDP categories.

When viewed as one country among the members of the European Monetary Union- among the original members plus Greece- Italy has the third lowest quarterly gain in GDP in the fourth quarter among the reporters (Greece and Luxembourg have not yet reported). Viewed against that same group over the last year, Italy has the biggest decline in GDP among these members at -0.9%. Finland is second with a -0.5% GDP drop; Spain is behind Finland with a -0.2% GDP decline.

However, GDP is not roaring ahead in any of the countries of the European Monetary Union. Portugal has a year-over-year pace of 1.7% followed by Germany at 1.4%. Looking at growth in the fourth quarter alone, the Netherlands has posted a nice rise of 2.8% followed by Portugal at 2.5%. After them we have Austria at 2.1% and Belgium at 2.0% rather ordinary rates of growth, not the sort of surges you would expect in a real economic recovery from recession. Europe seems to be embarked upon the same sort of lethargic recovery that the US has had.

Among reporting original EMU members plus Greece, only Denmark shows a deceleration in its year-over-year growth in the fourth quarter compared to the third quarter. In the third quarter, only France had showed a deceleration on that basis. In the second quarter of 2013, only the Netherlands had showed a deceleration on that basis whereas in the first quarter of 2013, trends looked grim in the Monetary Union. Back in the first quarter, nine of the 13 countries reporting GDP were showing a deceleration in year-over-year GDP growth compared to the previous quarter. In addition, 11 of those countries were showing outright declines in year-over-year GDP.

There can be no doubt that large strides have been made in the EMU over the course of 2013. Growth is now the order of the day with only three of the reporting countries showing year-over-year GDP declines in the fourth quarter and only one country (a different one from those three) showing a deceleration in year-over-year growth in the fourth quarter compared the third quarter. These trends are clear improvements compared to the trends of Q1 2013.

While there's plenty of evidence that the European Monetary Union is turning the corner on growth, the Union as a whole has only one consecutive quarter of year-over-year GDP growth. Its recent annualized quarterly growth rates are all modest with the most recent Q4 rate at just 1.1% at an annual rate. Energy uncertainty and new developments in geopolitics put these growth rates and this progress on uneven footing. While there is a clear shift to improve growth, it's also a slow turn with a lot of work left to do. Financial fragility is still an issue. Every time we have evaluated progress in the EMU over the past several months, we have noted that there has been improvement while also noting that the improvement has been slow and that the environment continues to be fragile. With the new developments in geopolitics along Europe's eastern border, we have to further emphasize that risks remain.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.