Global| Mar 07 2019

Global| Mar 07 2019Italian Retail Sales Show Lifeless Bounce While Italy Shows Bounce-Less Life As the ECB Re-thinks the Future

Summary

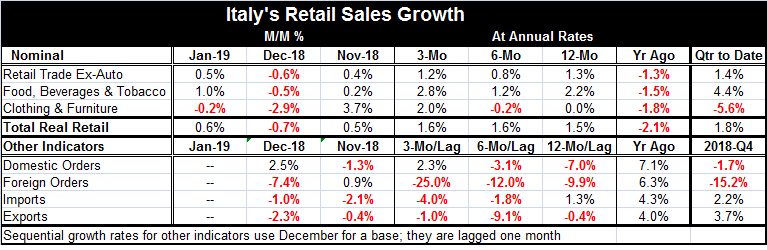

Italian retail sales jumped 0.5% in January, a strong-looking gain made less so by the recognition that sales also fell by -0.6% in December. Expressed in real terms, Italian sales log a 0.6% rise in January against a drop of 'only' [...]

Italian retail sales jumped 0.5% in January, a strong-looking gain made less so by the recognition that sales also fell by -0.6% in December.

Italian retail sales jumped 0.5% in January, a strong-looking gain made less so by the recognition that sales also fell by -0.6% in December.

Expressed in real terms, Italian sales log a 0.6% rise in January against a drop of 'only' 0.7% in December.

Sequential growth rates on either real or nominal data do not produce clear trends on growth rates from 12-months to six-months to three-months. However, all those horizons show very moderate-to-weak growth for Italian retail sales be they nominal or real. Sales may not be 'clearly' trending but by no means are the patterns encouraging. And as the year-ago column shows, sales have been weak for some time with real sales down by a sizeable 2.1%. Year-over-year one year ago at this time and now from that weak performance, year-over-year sales are up by only 1.5% in real terms – that a net drop over two years.

In the quarter to date, real retail sales are rising at a 1.8% annual rate; nominal sales are up at a 1.4% pace. Those calculations annualize the growth rate for the January level of sales relative to the fourth quarter level for sales.

We can also peruse other Italian indicators to get a sense of how conditions are unfolding. The quick look is not encouraging as three of the four metrics we log in the table show declines or flatness in December; none of them yet post January observations. Domestic orders, show a December gain while foreign orders, imports and exports all show December drops; In Q4 2018, domestic and foreign orders are plunging while imports (reflecting domestic demand) make a small gain and exports (subject to the tug of forces abroad rather than those at home) show the strongest year-on-year growth of 3.7%. Imports which track domestic demand are up by just 4.3% over 12 months and up at a 2.2% pace in the fourth quarter.

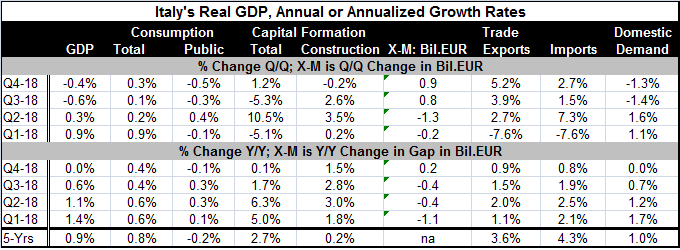

Finalized data on euro area GDP leave us with these trends for Italy. GDP in Italy has fallen for two quarters in a row, triggering the rule-of-thumb recession call. And adding some meat to the bones of that call, Italian GDP growth is at a dead flat zero over four quarters. That sort of stagnation is not good news. The metrics in the retail sales table point to more weakness coming in Q1. Everyone knows about the political turmoil in Italy with the ascension of the Five Star Movement and its clash with the EU Commission over policy options. In addition to Italy's fiscal problem it has a legacy of poor growth. The chart at the top show that real retail sales in Italy have trailed the EMU total persistently since 2010. In addition many Italian banks are undercapitalized and Italy is pushing back at the EU Commission to try to get the bail-in rule reversed. That rule was adopted when Cyprus had its problems and the ECB did not want to 'bail out' a lot of foreign depositors, many of them Russian. But both Germany and France had orchestrated their own bailouts of their banks at an earlier time, before this rule was adopted to protect them for the coming Greek crisis. Now Italian banks need infusions and many are in bad enough shape that they will probably not be able to get them from the credit markets. Italy does not want to trigger a series of bail-ins.

Italy's growth challenges are well laid out in the table of GDP components below. Domestic demand has been dead flat over 12 months. Capital formation is up by just 0.1%. Public consumption is down by 0.1%. Total consumption, which has been running at an annual rate of 0.6%, stepped down to 0.4% over the last two quarters. The export/import balance has been close meaning the international impact on growth has been small.

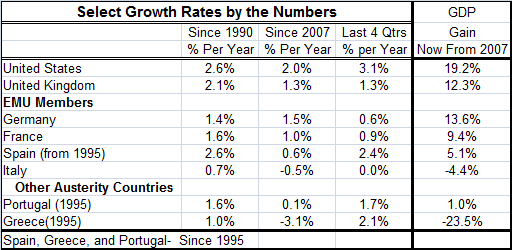

Italy needs a plan. It has lagged the rest of the euro area badly. And it is hard to imagine that what it needs after all this time of less than acceptable growth is a dose of EU-Commission-style austerity. Only Greece has done worse and the austerity countries of Spain and Portugal have outdone Italy with Spain logging 5.1% growth since 2007 and Portugal eking out 1 percentage point of growth; these results compare to -4.4% for Italy on that same timeline. Italy may still have a 'bad' culture for growth that is too dependent on the government and a culture of tax evasion. But the weak growth in Europe and the weakening growth now are not providing Italy with any of the regional support that it could badly use.

Today the ECB has acknowledged the severe state of EMU growth and has pushed off its plan for rate hikes and set a new round of TLTROs to begin in September. Italy has averaged less than three quarters of one percentage point of annual growth over the last 18 years. It is not surprising that this has been a period that has strained government finances. Italy is now a bit of a chicken and egg problem as, at this point, it is not clear where a virtuous circle for stimulus might have success. Italy is again the very sick man of Europe. Only its bright cheery responses to consumer confidence surveys belie its sorry state of affairs. But if Italians are really so 'happy' why is Italian politics in such turmoil?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief