Global| Jun 11 2020

Global| Jun 11 2020Italian IP Takes a Walloping As Much of Europe Takes a Beating

Summary

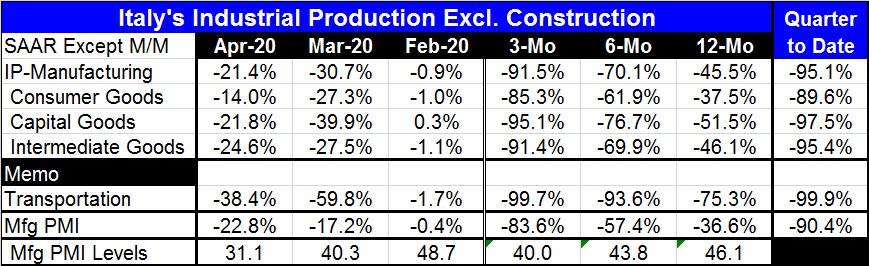

Italian industrial production has been decimated over the last two months, falling by 30.7% in March then falling again by 21.4% in April. Both are month-to-month percentage changes. Over three months, IP is falling at a 91.5% annual [...]

Italian industrial production has been decimated over the last two months, falling by 30.7% in March then falling again by 21.4% in April. Both are month-to-month percentage changes. Over three months, IP is falling at a 91.5% annual rate. In the new quarter-to-date, IP is falling at a 95.1% annual rate. Previously, back to 1981 the largest two-month fall in Italian IP was 8.3% in March 2009; however, there also a large two-month drop of 7.2% in June 1982. But nothing in the past compares to the 45.5% two-month drop Italy has just registered in IP in March and April of 2020.

Italian industrial production has been decimated over the last two months, falling by 30.7% in March then falling again by 21.4% in April. Both are month-to-month percentage changes. Over three months, IP is falling at a 91.5% annual rate. In the new quarter-to-date, IP is falling at a 95.1% annual rate. Previously, back to 1981 the largest two-month fall in Italian IP was 8.3% in March 2009; however, there also a large two-month drop of 7.2% in June 1982. But nothing in the past compares to the 45.5% two-month drop Italy has just registered in IP in March and April of 2020.

The pace of the decline is astonishing. And while it is for March and April the periods when other countries have been showing their excessive weakness, Italy's weakness is simply record-setting. Among the nine EMU countries that have reported IP, plus Sweden and Norway, Italy leads the pack in two-month IP losses. Italy's 45.5% two-month decline is challenged by Luxembourg's 41.4% two-month drop. Spain and France both post drops slightly larger than 36% over two months. Germany has IP falling by 30% over two months and Belgium by 25%. Among all eleven countries, there is an average drop of 23.2% and median drop of 25.2%. Italy has been hit extremely hard.

From extreme weakness to even more weakness

The EU still does not have a support program in place. Its most recent statement is that any help provided should support growth. Northern European countries do not want monies thrown into a sink hole. But Italy is surely in need of help with the sort of weakness it is experiencing. The coronavirus may be the same thing in all places, but it hit some places harder and earlier than others and that in turn helped those that were later affected to craft better policies to deal with it.

Year-on-year the Italian decline at the same 45.5% pace is also the largest drop with Luxembourg again second at a decline of 43.9%. Spanish IP is down by nearly 38% over 12 months German IP by 37% and so on. The median 12-month drop for this group of eleven countries is 26.6%. Once again Italy sticks out like sore thumb since Luxembourg's drop, which rivals that of Italy, comes from a country that does not have much manufacturing activity at all.

The correlation between the two-month and the 12-month drops is 0.99, extremely high. Four of the five countries most adversely affected in terms of two-month drops and 12-month IP drops are the four largest EMU economies: Germany, France Italy and Spain. Of course, Luxembourg, one of the smaller member states, is also in that grouping. But the large countries seem to have been affected more possibly because they are harder to manage and control because of their size. Or perhaps it is because their global integration is more advanced. Among the least affected countries were Finland, Norway, Malta, the Netherlands and Sweden, a concentration of countries from Northern Europe.

The virus continues to be front and center on any economic analysis. Since its path cannot be known, no forecast can be reliably made. Just yesterday the OECD pitched a number of double-digit GDP declines as forecasts for European countries. It did that on the assumption that there would not be a second wave of infection. The potential for something quite a bit worse is clear. But no one can be sure of the nature of a threat for a second wave. It is pretty clear that there will not be a vaccine in time to ward off a second wave if one comes and yet public sentiment is so relieved to finally be out from under lockdown it is not clear if a lockdown strategy could be as effectively employed again.

Italy shows some deep weakness created by an effort to short-circuit the spread of the virus. Italy's weakness is pronounced and widespread across manufacturing. The prospect for recovery is quite uncertain… as is the prospect for help for needy Europe from the rest of Europe. The ECB has pitched in from the start, but the EU Commission has been unable to get an agreement on help since the rich countries in the North are eager that the EU not become a transfer union. Yet, that is more or less how the virus has struck. They apparently do not wish to deal with it.

Of course, this is another example of how far countries in the North will go to pursue financial probity. They already have subjected a number of countries of Southern Europe (plus Ireland) to their version of austerity, a program that did help to reduce inflation but has also helped to damage those same economies. Germany has been in such dogged pursuit of its fiscal surpluses that it has stone-walled repeated U.S. requests and demands for a larger contribution to NATO. Germany has fallen back on a pledge to contribute 2% of GDP by 2031. And that was a goal set by NATO leaders in 2014. So now U.S. President Donald Trump has become so frustrated that he is going to reduce U.S. troop presence in Germany. It seems to me that one should put security above financial probity unless a country is looking to get invaded and wants to be sure that its 'books are in good order' for when that happens. Such are the trade-offs and values in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief