Global| Aug 11 2016

Global| Aug 11 2016Italian Inflation Shows Little Pickup, But the Thrill Is Gone

Summary

We can identify four key measures of Italian inflation. By two these measures month-to-month inflation was stable in July; by two others inflation ticked higher month-to-month. On a year-over-year basis, inflation is stable on three [...]

We can identify four key measures of Italian inflation. By two these measures month-to-month inflation was stable in July; by two others inflation ticked higher month-to-month. On a year-over-year basis, inflation is stable on three of these four measures and lower on one.

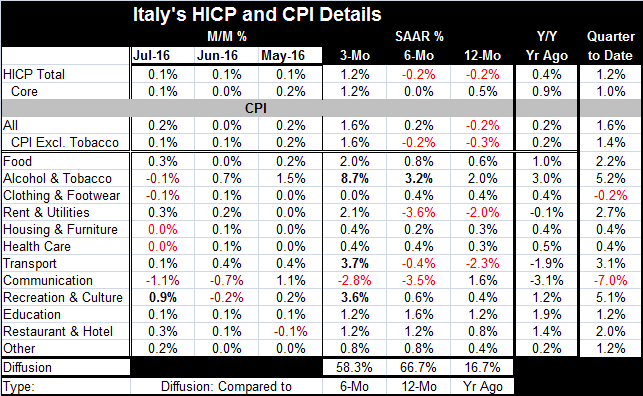

The four Italian inflation measures are the HICP headline plus its core (which excludes energy and unprocessed food) and the same headline and core measure for the Italian domestic CPI. The CPI and HICP measures are constructed somewhat differently and produce slightly different results. Yet each is a solid gauge in its own right when used for its own purpose. The four measures largely agree that Italian inflation is under control.

We can identify four key measures of Italian inflation. By two these measures month-to-month inflation was stable in July; by two others inflation ticked higher month-to-month. On a year-over-year basis, inflation is stable on three of these four measures and lower on one.

The four Italian inflation measures are the HICP headline plus its core (which excludes energy and unprocessed food) and the same headline and core measure for the Italian domestic CPI. The CPI and HICP measures are constructed somewhat differently and produce slightly different results. Yet each is a solid gauge in its own right when used for its own purpose. The four measures largely agree that Italian inflation is under control.

Moreover, Italian core and headline HICP inflation is still running below the comparable measures for Germany. On balance, we judge Italian inflation to be very stable and under control.

The table shows the results by price index plus provides inflation detail for the Italian CPI and a timeseries for each metric in the table. Based on these results, several factors are clearly true.

* Price level drops have become less common.

* For the last three months, `core' and `headline' inflation measures show little divergence.

* Despite the `run-up' in oil prices, inflation (as measured by diffusion) is not clearly accelerating.

* To the extent that pressure is evident in the aggregate, it is mostly a three-month phenomenon.

* In July alone, a cluster of flat inflation rates and month-to-month declines again has emerged.

Italian inflation: maybe not the seventh wonder of the modern world, but impressive

Italian inflation whether measured by the core or headline HICP measures is still below the comparable gauge for Germany over the past year (see chart for headline HICP measure). Italian inflation, once one of the higher rates on a consistent basis in the EMU, has been below German inflation on the same measure consistently (although not uniformly) since mid-2013. Austerity in Italy has `worked' to cap inflation and has also helped to control domestic fiscal spending. But in controlling domestic fiscal spending, it has deprived the government of the flexibility needed to deal with its banks.

Unequal treatment in the guise of equal treatment

Well after the Cyprus crisis, the adoption of the no bailout rule for banks has put Italy behind the eight ball. In remarks today the Chief of the EU's Single Resolution Board - the body charged with monitoring bank rescues- Elke Koenig, said that she did not see any need at present to suspend the bail-in rules. Last month Italy had been denied an exemption for troubled lender bank Monte dei Paschi. But it is hardly the only Italian bank in need of some sort of assistance. It is not clear if the EU chief's statement today is meant to leave the door open with its disclaimer phase `any need at present' or if this is just rhetoric and the continuation of the EU's hard line will keep that door slammed shut. Of course, in the wake of the financial crisis, many national banking systems in the EU received bailouts including German banks. But these actions were taken before new rules were put in effect at the time of the Cyprus banking crisis when Europeans did not want to pump monies into banks that were substantially supported by Russian and other foreign investors.

No rest for the weary here?

Italy finds itself having been a `good citizen' and controlled its rate of inflation. However, there are troubles percolating in Italy as austerity has armed some new dissenters. The EU separatist (anti-migration) party, Five Star Movement, now has its members holding the position of mayor in two large Italian cities, Turin and in Rome, as well as in seventeen others. In one recent poll, it has been called the most popular party in Italy. In the wake of Brexit, the continued hard line against allowing Italy any added scope to recapitalize its banks will intensify pressures in Italian politics, especially on Italy's Prime Minister Matteo Renzi.

The hip bone is connected to the leg bone...and so on

Italy's banking and budget problems are linked. Italy's progress on inflation is also linked to its control of its fiscal spending. But this constellation of linked processes is under pressure and how it is dealt with will be a huge force in Italian politics. Something will have to give. It is hard to imagine Italy sticking to EU rules and allowing its banks to be `resolved' by bail-ins, a process that will bankrupt many shareholders and bond holders who are important forces behind the scenes in Italian politics, just as such a group would be in any other country.

The thrill is gone

Italy has made progress especially on inflation. However, Italian sector PMI activity gauges remain weak and with negative momentum. The EU has just cut special deals for Spain and Portugal deciding not to pursue excess deficit penalties on them for broaching their promised debt parameters while engaged in their austerity programs arguing that they made good effort and progress. The question is if there will be any slack cut for Italy on its banking sector dilemma. Without it, Italy could either rebel against EU rules or find its political process under a great deal of heat. At some point, when an economy fails to respond to rounds of economic stimulus, there is political backlash. Voters run out of patience and look for new economic managers. Italy is getting close to it. The U.K. voted to exit the EU. Spain has its Podemos party. The rise of dissent in the EU/EMU over the pressure cooker of the austerity progresses as migrant issues become increasingly hot issues and have stepped up discord within the EU and euro area. These regions than once, during the worst of the financial crisis, argued that they were mostly a political union that would find its way to economic solutions now finds underlying political differences and economic problems that pit members against other member on key social and economic issues. The sense of European unity is severely diminished if not gone. And the thrill clearly is gone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief