Global| Sep 18 2015

Global| Sep 18 2015Italian Exports and Imports Slow As Global Theme of Weakness Plays Out

Summary

Italy's current account surplus shrank in July as exports and imports both fell. Declining trade flows may get greater scrutiny now that the U.S. Federal Reserve has put its rate hike plans on hold. Judging from market reactions, [...]

Italy's current account surplus shrank in July as exports and imports both fell. Declining trade flows may get greater scrutiny now that the U.S. Federal Reserve has put its rate hike plans on hold. Judging from market reactions, forecasters and investors are more willing to mark down their own forecasts and expectations under the cover of the Fed marking down its expectations.

Italy's current account surplus shrank in July as exports and imports both fell. Declining trade flows may get greater scrutiny now that the U.S. Federal Reserve has put its rate hike plans on hold. Judging from market reactions, forecasters and investors are more willing to mark down their own forecasts and expectations under the cover of the Fed marking down its expectations.

The Federal Reserve put its policies on hold because of instability in foreign markets and weak foreign growth. Italy's trade release today keeps that theme in play. Apparently many prognosticators do not have their own ideas as much as they piggy back on the Fed's forecasts. Fed forecasts for economic variables were not cut nearly as much as the Fed's own assessment of the path of its future policy.

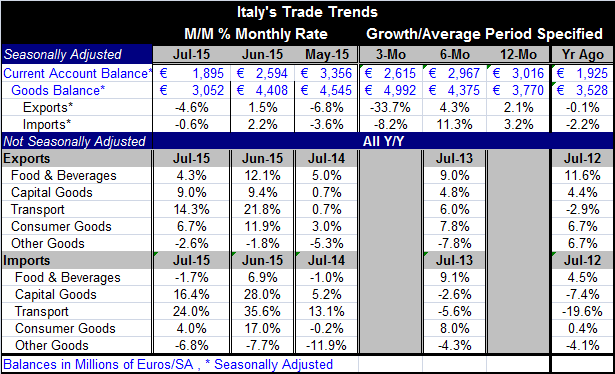

Italy shows a declining surplus which will subtract from its growth. Exports are sharply weaker, dropping by 4.6% as imports fall by a more modest 0.6%.

Over three months Italian exports are falling at a 33.7% annual rate and this is with steady weakness in the euro. Improved competitiveness- at least for trade outside the euro area- has not been able to keep Italy's trade or current account balance steady. A weak euro has not been compensation enough for austerity.

Year-over-year Italian imports are outpacing Italian exports with imports up by a modest 3.2% and exports up by a more modest 2.1%.

Year-over-year export categories find some strength in food and in consumer goods. Capital goods exports continue to show modest growth with other exports falling. Import categories also showed strength in food and in consumer goods. But imports of capital goods, transportation equipment and other goods fell.

On balance, these are weak trade flows. Italy, of course, is still under the yoke of austerity and all countries in the EMU are being held to their Maastricht deficit requirements. Today Finland of all countries has had a strike that has closed its ports as the people in that fiscally conservative country with huge social benefits are fed up.

It will be interesting to watch trade and other economic developments in all the countries of Europe. With this flare up in austerity protests in an expected place, Finland, it will be interesting to see if there is push back anywhere else in Europe. The Fed's non-move and its rationale act like a blank check for other nations. They may now expect something special to be done to boost growth, since all European pro-growth policies to this point have failed. It will be interesting to see if this winds up putting more pressure on Germany to reflate or to back down on its austerity hard line (I know, when das-hell freezes over).

In some ways, the game has changed with the recent developments in China, the unhinging of oil and commodity prices, and the increased burden all this has placed on developing economies. It is as though the FOMC poked its head up opened its eyes and noted that the emperor had no clothes. It has an impact and paves the way for others to make similar observations without seeming to be off base or sticking their necks out.

The world has changed. It has changed more for policymakers that for actual economic developments. But policymakers now may have a chance to reconfigure policy in a way that can affect the real economy. It will be an interesting thing to watch. The Fed move will put the German position on trial as it now becomes clear that a policy of austerity in Europe has held back growth and that all the king's horses and all king's men of monetary policy have been unable to move growth ahead again. Of course, German policymakers have been saying just that: that monetary policy can't solve these problems. The question now is if that admission will backfire on Germany as more EMU nations may want to see more rapid progress rather than waiting further years for German-led austerity to bear fruit. Is Finland a catalyst? Are the Germans able to bend or not? I think that those questions will next be on the table in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief