Global| Nov 25 2016

Global| Nov 25 2016Italian Economy Weakens Ahead of Italian Referendum

Summary

Italy is showing some weakening economic trends ahead of its early December referendum. And while everyone is still buzzing about Brexit and the Trump election in the U.S., the Fed continues to talk of potential Brexit risks as though [...]

Italy is showing some weakening economic trends ahead of its early December referendum. And while everyone is still buzzing about Brexit and the Trump election in the U.S., the Fed continues to talk of potential Brexit risks as though they are still the next threat to European stability. Yet, the referendum in Italy could prove to be even more important and more destabilizing to Europe if things go the wrong way. Italy's burgeoning Five Star political movement wants to exit the EMU (Itxit?/or EMUXit?) and relaunch the Lira. Because Italy is in the core of the EMU, anything destabilizing in Italy has much greater potential consequences for economic disruption than Brexit which only involves the U.K. leaving the EU. The U.K. never adopted the single currency and will have no currency entanglements to unwind with the ECB as Italy would should it leave. If that were to happen, putting toothpaste back in the tube or untangling the post Lehman Bros. mess in the U.S. would look like child's play in comparison to what would need to be done in Europe. Will that prospect keep Italian voters on Renzi's side?

Italy is showing some weakening economic trends ahead of its early December referendum. And while everyone is still buzzing about Brexit and the Trump election in the U.S., the Fed continues to talk of potential Brexit risks as though they are still the next threat to European stability. Yet, the referendum in Italy could prove to be even more important and more destabilizing to Europe if things go the wrong way. Italy's burgeoning Five Star political movement wants to exit the EMU (Itxit?/or EMUXit?) and relaunch the Lira. Because Italy is in the core of the EMU, anything destabilizing in Italy has much greater potential consequences for economic disruption than Brexit which only involves the U.K. leaving the EU. The U.K. never adopted the single currency and will have no currency entanglements to unwind with the ECB as Italy would should it leave. If that were to happen, putting toothpaste back in the tube or untangling the post Lehman Bros. mess in the U.S. would look like child's play in comparison to what would need to be done in Europe. Will that prospect keep Italian voters on Renzi's side?

As Italy's voters prepare for their referendum which is formally about legislative reform, it is also thought to be about supporting the government and agenda of Prime Minister Matteo Renzi. That is why a rejection of the proposed legislative streamlining is so crucial. Renzi's reforms would make it easier for Italian lawmakers to pass new legislation. The reforms are designed to reduce the size and power of the senate, which currently carries as much clout as the lower house, and to grab back power from Italy's 20 regional governments. But this vote comes at a time that centralization is under attack at least as far as having Italy under the thumb of the EU and the EU Commission and leaving it without its own independent central bank. The popularity of the Five Star movement suggests that these reforms may be heading in the wrong direction given the country's current leanings although the issues here are complex and not simply about centralization. The economy is sinking as people get ready to cast their votes. Being in poor economic spirits usually is not helpful to attaining the goals of the sitting administration. Let's look at the trends.

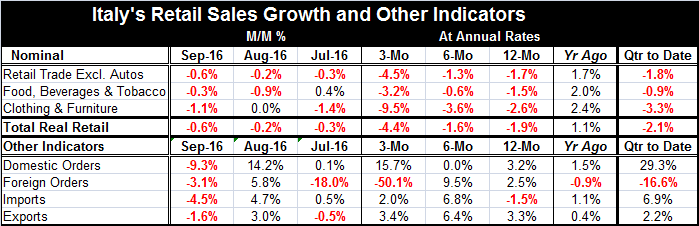

Retail sales slump: Retail sales dropped yet again

Italian retail sales as of September have dropped for three consecutive months and the drop is getting larger. While sales only fell by 0.3% in July and 0.2% in August, in September there was a drop of 0.6%. The three-month drop is at a -4.5% pace in nominal terms and a -4.4% pace in real terms. Sales also are falling over 12 months by 1.7% in nominal terms and by -1.9% in real terms.

Consumer confidence: Slippity-do-dah

Italian consumer confidence has been slipping too. For a while, Italy was a real oxymoron with a clearly weak and underperforming economy yet rising and relatively strong consumer confidence. But that has changed. Confidence peaked around the turn of the year and has since been falling rather rapidly. The peak growth rate in nominal retail sales and the peak in the consumer confidence index are pretty much in sync as are the weakening trends that are in play this year.

Industrial orders: Mixed orders trends

Italian industrial orders also were released today and they show a drop in September, but domestic orders generally have been expanding nicely although the overall picture has been weakened by falling foreign orders which have been especially weak over the last three months.

Trade: Weakness in exports and imports

Italian imports and exports both dropped in September but show some modest gains over three months and six months and mixed performance over 12 months.

Summing up

On balance, Italy is struggling in a way that will make the referendum harder for people to swallow. Italy also is a target country for migrants and that has added pressure on the economy as well as on costs at a time that the European Commission has not been understanding about special factors that may have impeded countries' abilities to achieve their budget targets. Italy is experiencing many of the same issues and pressures as was the U.K. when it took its Brexit poll. Still, we have seen enough surprises to know that it is hard to handicap how people are going to vote on these things. Will the lack of Turmoil over the Brexit vote embolden the Italian voter or will the clear political disarray in the U.S. after the Trump election line them up behind Renzi's reforms? While the Italian referendum is not a referendum on the EU or EMU membership, it has implications for that because any weakening of the Renzi administration will boost the Five Star movement and possibly bring it to power. Five Star already has control of the political apparatus in two large Italian cities. In the U.S., the Fed seems to want to pretend that everything is fine and is trying not to not direct any attention toward Italy. But there will be no ignoring the Italian vote. And it could have blowback with tailwinds that reach across the Atlantic- don't let the Fed's low-key approach fool you. The vote is set for December 4, just a little more than one week away. It is a very important international event with consequences potentially well beyond those affecting just Italy. If Italy does reject the referendum, historians are going to have a field day dealing with the rejection of the elites and their pet policies in the U.S., the UK and Italy, and who know what would come after that?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief