Global| Jun 10 2021

Global| Jun 10 2021IP Rises Broadly Across Euro Area

Summary

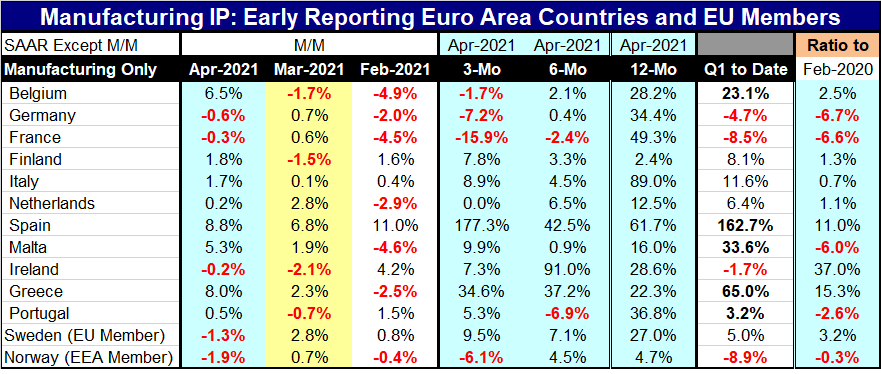

In April manufacturing industrial production (IP) grew in eight of thirteen early IP reporters in Europe. IP fell in Germany, France, Ireland, Sweden, and Norway. Output rose in Italy and Spain, the third and fourth largest EMU [...]

In April manufacturing industrial production (IP) grew in eight of thirteen early IP reporters in Europe. IP fell in Germany, France, Ireland, Sweden, and Norway. Output rose in Italy and Spain, the third and fourth largest EMU economies, and across an assortment of smaller European economics. In March IP fell in four economies and rose in nine. In February IP declined in seven economies and rose in only six. The breadth of IP increases seems to be improving.

In April manufacturing industrial production (IP) grew in eight of thirteen early IP reporters in Europe. IP fell in Germany, France, Ireland, Sweden, and Norway. Output rose in Italy and Spain, the third and fourth largest EMU economies, and across an assortment of smaller European economics. In March IP fell in four economies and rose in nine. In February IP declined in seven economies and rose in only six. The breadth of IP increases seems to be improving.

IP rose in all 13 economies over 12 months and in 11 of 13 over six months. IP rose in eight over three months while falling in four as output in the Netherlands was unchanged.

These data are for April putting the year-ago comparison in a deep pit of Covid-caused weakness a year ago. This inflates the year-on-year gain. However, calculations over the shorter spans continue to reveal broad increasing trends. Output is clearly still on an upswing across the EMU.

However, there is lingering weakness in the EMU’s two largest economies Germany and France. Both France and Germany show output declines over three months as well as in two of the three most recent months. France also shows a decline in IP over six months, a period in which German IP rises at an annual rate of only 0.4%, the third weakest result in the table.

Italy and Spain, the next two largest EMU economies, are not plagued by weakness in IP. Both show strong gains over three months as well as over six months. But clearly the weakness in Germany and France will hold back gains for the EMU as a whole when that total is reported.

In the quarter-to-date, IP is falling in Germany, France, Ireland and Norway. IP is growing at double-digit rates in Belgium Italy, Spain, Malta, and Greece.

Over the last three years the divergence in monthly rates of growth for this group of countries has been wide; divergence has been greater than this only six times (17% of the time) and all of those occasions have come since Covid struck. This suggests that the Covid process is still creating differences across European economies that are greater than usual despite the big swings in output being relatively widely shared (see graph).

The ratio of current output-to-output levels in February 2020 finds five of these 13 countries with manufacturing output still lower on balance. The countries that are weaker on balance since Covid struck are Germany, France, Malta, Portugal, and Norway. Ireland, Greece and Spain have output up by double digits on this timeline. The median increase for this group of countries is a gain of 1.1%. The Netherlands is the median country on this measure.

A great deal of similarity in the Covid/post-Covid period

The Markit manufacturing PMI data and the EU Commission diffusion indexes for Industry show a great deal of strength for this same period. The EU data show Germany with the strongest raw reading among the large economies. Yet, actual output data do not match the results of the diffusion style surveys. Ranked on diffusion data back to May 1990, April is the strongest EMU diffusion reading for Germany on record; that is not so for German output gains over 12 months, however. France also scores a high diffusion ranking despite its current IP struggles.

Diffusion data again seem to overstate the degree of strength in the rebound for manufacturing. The rebound is real and it is ongoing, but this is not a fine-tuned automobile firing on all cylinders. Yet, enough cylinders are firing well enough to keep the recovery in motion. And substantial country differences remain as Covid continues to leave its mark on recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief