Global| Mar 20 2009

Global| Mar 20 2009IP In Zone In Record Drop

Summary

It is the largest drop in e-Zone IP since records have been kept. Intermediate goods, capital goods and consumer goods output trends are being clobbered. Each sector is worsening sequentially. Each of the countries displayed: Germany, [...]

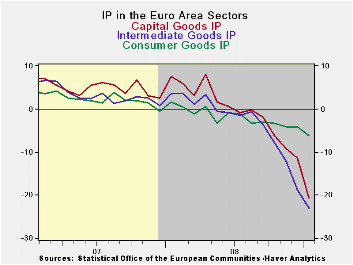

It is the largest drop in e-Zone IP since records have been

kept. Intermediate goods, capital goods and consumer goods output

trends are being clobbered. Each sector is worsening sequentially. Each

of the countries displayed: Germany, France, Italy, and the UK, is

experiencing sequentially worsening rates of growth for their selected

measures of IP.

It is getting worse. The EU is in the belly of the beast and

beast is recession.

Statements for Germany today confirm that things are getting worse there and that there are no signs of a turnaround. In France INSEE is now looking for Q1-2009 to be weaker than Q4-2008. In France despite the lobbying Sarkozy has done for more stimulus and relaxation within the Area, French workers are striking as if he could DO SOMETHING about the severity of the recession. They are in fact wanting him to do more to mitigate it. But France, like other EMU members, has to be mindful of the Maastricht rules that apply to budget deficits. Europeans, despite seeing this worsening in their respective economies, are amazingly blasé about doing more to mitigate the effects. Moreover, within the Group of 20 European member are far more interested in rules and regulations for the future than in dealing with current issues. If they were firemen they’d be calling in the arson investigators instead of dousing the still-raging and expanding flames. Europeans are different.

| E-zone MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Jan 09 |

Dec 08 |

Jan 09 |

Dec 08 |

Jan 09 |

Dec 08 |

|||

| E Area Detail | Jan 09 |

Dec 08 |

Nov 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-1 |

| Consumer | -1.3% | -0.3% | -0.9% | -9.2% | -5.0% | -7.0% | -5.6% | -6.2% | -4.1% | -9.9% |

| C-Durables | -2.6% | -2.6% | -3.4% | -29.6% | -25.8% | -21.0% | -19.8% | -17.2% | -12.4% | -- |

| C-Non-durables | -1.1% | 0.4% | -0.8% | -6.2% | -0.6% | -3.6% | -3.1% | -4.7% | -2.4% | -- |

| Intermediate | -3.6% | -6.0% | -4.2% | -43.1% | -42.1% | -33.3% | -29.2% | -23.1% | -18.8% | -42.6% |

| Capital | -6.0% | -2.6% | -3.2% | -38.2% | -28.6% | -27.7% | -19.3% | -20.6% | -11.4% | -41.8% |

| Main E-zone Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Jan 09 |

Dec 08 |

Jan 09 |

Dec 08 |

Jan 09 |

Dec 08 |

||||

| MFG Only | Jan 09 |

Dec 08 |

Nov 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2- Date |

| Germany: | -8.5% | -4.8% | -4.2% | -51.4% | -36.4% | -33.7% | -23.1% | -20.7% | -12.2% | -55.9% |

| France: IPxConstruct'n | -3.1% | -1.5% | -2.8% | -26.0% | -27.1% | -21.3% | -15.3% | -13.8% | -10.2% | -26.6% |

| Italy | -0.2% | -2.7% | -3.2% | -21.9% | -28.1% | -20.7% | -22.8% | -14.6% | -13.1% | -17.2% |

| Spain | -8.4% | 3.8% | -9.5% | -45.1% | -29.8% | -38.0% | -8.2% | -23.7% | -15.5% | -44.0% |

| UK: EU member | -2.8% | -1.9% | -3.0% | -26.8% | -22.9% | -19.9% | -15.9% | -12.8% | -10.0% | -26.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief