Global| Oct 10 2013

Global| Oct 10 2013IP in Italy and France Lags: How Sustainable Is This?

Summary

In Italy industrial production trends are weak while in France there is less sense of ongoing progress and there is a big setback over the past few months. French IP is falling at an 8.3% annual rate over three-months compared with [...]

In Italy industrial production trends are weak while in France there is less sense of ongoing progress and there is a big setback over the past few months.

In Italy industrial production trends are weak while in France there is less sense of ongoing progress and there is a big setback over the past few months.

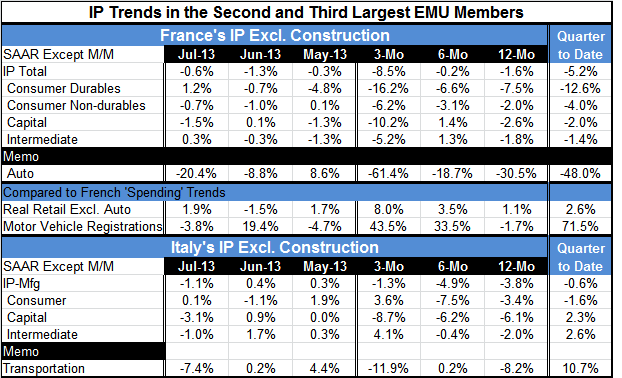

French IP is falling at an 8.3% annual rate over three-months compared with annualized rate of growth of -0.2% and -1.6% over 6-months and 12-months respectively.

In Italy IP is making progress, but is still in a state of decline. IP is falling at a rate of -1.3% over three months of -4.9% over 6-months and by -3.8% over 12-months. The trend shows some progress. Italy's progress is even more evident on the chart of 12-month growth rates.

In the quarter to date IP in both France and Italy is falling: in France at a -5.2% annual rate, and in Italy at a -0.6% annual rate. In the presentation yesterday "German IP Rises as EMU-wide IP Stirs", we showed the opposite result that IP was a rising in the quarter in most EMU members. But Italy and France belong to the lagging club and they are the second and third largest EMU members. Even Spain and Portugal are outperforming Italy and France in the quarter.

Consumer goods industries are performing relatively poorly in both France and in Italy. In Italy capital goods output is rising, while is France it is only less weak that consumer goods output. Intermediate goods have the strongest output in both countries in the quarter.

The OECD leading indicators through August confirm that Italy has better momentum than France overall, not just for the industrial sector. Both countries are still showing progress over 6-months and 12-months.

The evidence still seems to point to EMU and EU recovery. But the lagging performance in Italy and France remains an issue from the standpoint of sustainability. Europe will have a hard time keeping harmony in the eurozone if Germany is doing well but if other members are still struggling. Letting up on austerity may not be enough.

The US has slowed more than expected this year. The IMF has cut its outlook for world growth. But both the US and IMF views are that things will get better. But the degree of improvement should still be questioned. The global growth paradigm is sifting and this is putting a lot of pressure on developing countries that used strategies of export-led growth. Nowhere is this more evident than in China. China used capital investment projects to sustain growth over the past year but to make its shift complete it must develop real sustainable domestic demand. That is not in the works. It will require higher wages for workers and will China in terms of competitiveness. China is still in denial over this fate.

But fate it is. Debt levels in the most industrialized countries will keep them from returning to their past growth paths. That means developing nations will have to look elsewhere for growth -exports will not carry them. The developing nations have their own problems with still floundering financial sectors. Historically low interest rates are not having much effect. Thus, too much optimism for the year ahead is not well founded. While every nation feels it should be able to do better and while there is a tendency to look for progress toward historic rates of growth, there is little logic in the optimism currently being displayed.

For the US the premise is that fiscal tightening will let up - but will it? The US still has a future profile of deficits and debt rising relative to GDP that needs attention. Republicans are worried; Democrats are not - in fact they seem to want more revenue. The US does not have a pro-growth program but it has pro-growth optimism.

Banks and financial sectors are still weak globally and are not about to finance a debt-led expansion in the US or in Europe.

Japan's progress has largely been made on the back of a weakening exchange rate. That channel will be limited in the future.

We do see some improvement ahead but we also are wary of how widespread it will and if it will be a case of building to a better future or an artificial pick up that will not be sustainable. The jury is still out on that one.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief