Global| Sep 10 2009

Global| Sep 10 2009IP In France Edges Higher In July

Summary

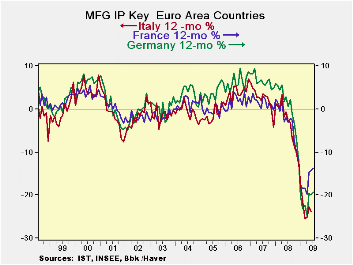

French industrial production rose by a thin margin of 0.1% in June, less than expected. Auto production contracted after a strong spurt in earlier months. Still, France has showed one of the stronger rebounds in EMU IP. It did not [...]

French industrial production rose by a thin margin of 0.1% in

June, less than expected. Auto production contracted after a strong

spurt in earlier months. Still, France has showed one of the stronger

rebounds in EMU IP. It did not sink as far as German IP but it has

rebounded just as much.

In France consumer durables output fell by a sharp 2.6% in

July. For nondurables consumer output was up by 1.1%. Capital goods

output took a set back despite what has been a solid run of growth for

that sector. Intermediate goods output rose strongly in July.

Trends in French IP are up strongly and across the board with

the exception of consumer durables.

In the current quarter output is rising at a 7.7% annual rate

with all main sectors doing better than that except, again, consumer

durables which is contracting in the new quarter and weighing down the

headline. On balance the rebound is robust and seems well entrenched.

The lack of progress in consumer durable goods is however a fly in the

recovery ointment. It suggests that consumers are able to be coaxed out

to buy some things but that they do not have the fundamental confidence

to take on the bigger-ticket items.

| French IP Excluding Construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Jul-09 | Jun-09 | May-09 | 3-mo | 6-mo | 12-mo | Quarter -To-Date |

| IP total | 0.1% | 0.2% | 3.0% | 13.9% | -0.7% | -13.0% | 7.7% |

| Consumer Dur | -2.6% | -2.9% | 0.8% | -17.8% | -20.9% | -21.5% | -23.3% |

| Consumer Ndur | 1.1% | 0.3% | 0.0% | 5.9% | -3.4% | -2.3% | 11.1% |

| Capital | -0.2% | 1.1% | 4.0% | 21.0% | 7.4% | -15.0% | 11.1% |

| Intermed | 1.6% | -0.1% | 3.7% | 22.7% | 4.4% | -19.6% | 17.9% |

| Memo | |||||||

| Auto | -1.9% | 14.3% | 12.5% | 154.2% | 23.2% | -29.8% | 87.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief