Global| Mar 10 2014

Global| Mar 10 2014IP Holds On To Recovery Trend...Can It Last?

Summary

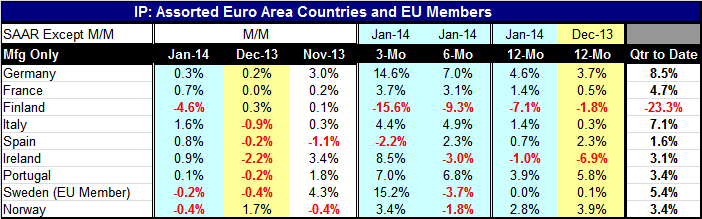

More countries in Europe reported industrial production with the net result showing an upswing in Europe. In January, only three of these early-reporting countries in the table showed declines in output. Finland's 4.6% drop was the [...]

More countries in Europe reported industrial production with the net result showing an upswing in Europe. In January, only three of these early-reporting countries in the table showed declines in output. Finland's 4.6% drop was the sharpest and the most alarming result. Two other Scandinavian countries, Sweden and Norway, showed significant drops in industrial production as well. Still, this is better than December when five of the 10 countries show drops in output.

More countries in Europe reported industrial production with the net result showing an upswing in Europe. In January, only three of these early-reporting countries in the table showed declines in output. Finland's 4.6% drop was the sharpest and the most alarming result. Two other Scandinavian countries, Sweden and Norway, showed significant drops in industrial production as well. Still, this is better than December when five of the 10 countries show drops in output.

However, when we step back and take a broader look, over three months, only Finland and Spain have net declines in industrial output. Spain's drop is at a 2.2% annual rate while Finland's is at an eye-popping 15.6% annual rate. Finland shows progressively deeper declines from 12 months to six months to three months. Meanwhile, Spain's decline is present over three months but Spain still logs increases over six months and 12 months. While the monthly numbers can sway to and fro, the clear signal from the sequential growth rates is that growth in Europe is gaining footing and continues to expand.

Europe still shows differences in growth rates among countries. The countries in the table are only a subset of the economies that matter for Europe and for the euro area. However, these countries are representative in the sense that they do show ongoing progress.

In the quarter to date, every country in the table, except Finland, shows increases in output. This calculation takes the growth rate in January over the fourth quarter base and annualizes it. On this basis, the weakest growth rate is in Spain at 1.6% while the strongest is Germany at 8.5% followed by Italy at 7.1%.

While Spain shows relatively weak growth in the new quarter, Spain's state-backed development bank sees stronger recovery and is now looking to shift its lending practices. The new focus will be on the quality of new credits instead of increasing the quantity of credits. This is an important step for Spain and further evidence that recovery is indeed spreading.

For EMU as a whole, the Sentix investor sentiment index has risen this month, hitting its highest level since the second quarter of 2011. However, with the new developments, in Ukraine and in Crimea, we have to wonder how Europe is going to be viewed. To some extent, the question is whether markets will want to bet that Putin is willing to cut off his nose to spite his face- or not.

Europe depends on energy exports from Russia. Russia depends on the revenue from these energy sales to Europe. Were Russia to cut of shipments to Europe, European economies would be severely impacted.but so would Russia with the loss of revenue. It may also be that certain financial entities have been unwilling to take aggressive short-Russia positions because they themselves have other investments in Russia they do not wish to imperil. Certainly the growth of investment in Russia from the West makes the notion of sanctions on Russia more of a two-edged sword and carries the a promise that when it cuts the sword will have a blunt edge.

The West is now confused on Russian intentions. In the wake of perestroika, actions in Crimea seem to be a step back. Viewed against the notion that Russia and the U.S. had a reset in their relationship this looks like the old Russia, before the reset. While Obama looks for an off-ramp from this crisis, he must be wary of the neighborhood in which he finds himself when he exits. Russian logic leaves the US few roads to explore and more reason to distrust Russian actions and motives elsewhere where it has said it would act as a partner, such as in Syria.

Russia's Crimea grab (the Crime in Crimea) is being handled in a delicate way and it is being seen as a potential Lehman moment for the international economy. Russia is not as wound in a matrix of transactions as was Lehman, but it is importantly connected especially with its energy sector. And energy pipelines are not quickly or easily rerouted. Everyone is afraid of pulling the pin of a hand grenade in an enclosed space. While the US will be looking for the right sanctions on Russia, the wrong choice could send a cascade of negative economic effects though global markets and yet, too light a touch could encourage Russia and others to grab more.

Putin is already reported to have evicted moderates from his inner circle of advisors, relying instead with those who have his same world view. In the wake of what he has does in Crimea, how he has done it, and how he has justified it, we cannot be too sure of what his next steps will be. That means that Europe may find itself out on more of a limb than it had expected at a time that its economic recovery seemed to be finding firmer footing. With Russia and Putin now ensconced in Crimea, a new air of uncertainty has been injected into the global economic environment. I wonder what the next Sentix survey will show.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.