Global| May 17 2021

Global| May 17 2021Inflation in Italy Surges then Heads Lower

Summary

Italy is one the early member of the Euro Area, of the EU, and of its precursor organizations. It was long one of the typical high inflation Mediterranean countries. But in the wake if the global financial crisis, Italy underwent [...]

Italy is one the early member of the Euro Area, of the EU, and of its precursor organizations. It was long one of the typical high inflation Mediterranean countries. But in the wake if the global financial crisis, Italy underwent austerity and has become a chronic low-inflation country. Over the last five years it has averaged inflation lower than Germany, France, and Spain the other three of the four largest Euro-Area economies. Its core inflation has averaged less than half of core inflation in Germany over the same period.

Italy is one the early member of the Euro Area, of the EU, and of its precursor organizations. It was long one of the typical high inflation Mediterranean countries. But in the wake if the global financial crisis, Italy underwent austerity and has become a chronic low-inflation country. Over the last five years it has averaged inflation lower than Germany, France, and Spain the other three of the four largest Euro-Area economies. Its core inflation has averaged less than half of core inflation in Germany over the same period.

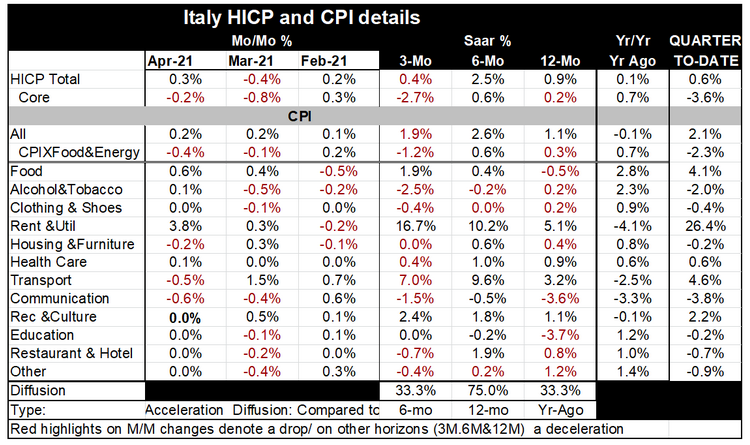

Italy has become a sort of low inflation barometer in EMU. This month it keeps that story alive. Italy's 12-month HICP is up by less than one percent. The core is up by 0.2%. And while the headline is up by 0.3% on the month (after a -0.4% drop in March) the Italian core is down by 0.2% in April and is up by just 0.2% over 12-months.

But inflation in Italy has undergone some bumps in the road. The 0.9% rise over 12-months escalated to a 2.5% annual rate of increase over 6-months. That rise, in turn, gave way to a 0.4% annual rate over 3-months. Core HIPC inflation logged 0.2% over 12-months with the annualized rate rising to 0.6% over six-months and then contracting at a 2.7% annual rate over 3-months.

The Italian domestic CPI numbers tell a similar story. The domestic gauge shows 12-month core inflation rising by 0.3%, accelerating to a still-weak 0.6% over 6-months them falling at a 1.2% clip over three-months.

Inflation diffusion shows inflation rising across most categories over 6-months but falling broadly over 12-months compared to 12-months ago and falling broadly over three-months compared to six-months ago.

Italian inflation data quarter-to-date, one month into the new quarter, show the core falling sharply on both measures and the headline rising at a 0.6% pace for the HICP and at a 2.1% pace for the domestic CPI measure.

Italian inflation remains well behaved and low at a time that inflation in EMU remains low as well. Meanwhile global inflation pressures on commodities are spurting in the dollar sector and US-based inflation is also rising strongly. Some of that is technical because of low base prices from a year ago when the virus struck. But that is not the whole story. There is enough inflation in the dollar sector that inflation expectations are rising. In EMU Italian bond yields rose to their highest level in eight months on concerns over Italy's reform direction and concerns that the rapid European rebound could slow the ECB bond buying program that has been supporting Italian bond prices.

Economic financial and market conditions are changing rapidly. The covid-19 situation is changing more slowly but it is closer to coming under control. As these progressions encroach on past trends market conditions are going to be affected. And as that happens the feedback to the economic situation will become a secondary fluid factor. Keeping inflation under control is still a big help because even in the face of improved growth, low inflation keeps the ECB off the war path. But with better growth any move to get rate levels back to normal will be an adverse development for bond market yields. This interaction has become the new frontier of policy uncertainty.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief