Global| Feb 14 2003

Global| Feb 14 2003Industrial Production Rebounded

by:Tom Moeller

|in:Economy in Brief

Summary

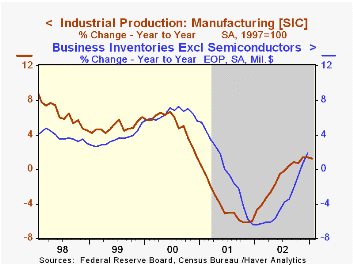

Industrial production rose more than Consensus expectations for a 0.3% gain in January. The rise followed a sharp decline in December that was downwardly revised from a 0.2% drop reported last month. Output in the manufacturing sector [...]

Industrial production rose more than Consensus expectations for a 0.3% gain in January. The rise followed a sharp decline in December that was downwardly revised from a 0.2% drop reported last month.

Output in the manufacturing sector rose 0.5% (1.3% y/y). The gain followed a 0.4% December decline that was double the initial estimate.

Excluding a 4.9% jump in motor vehicle and parts factory output rose just 0.1% (0.5% y/y), the second tepid monthly gain following three months of decline. Appliance, furniture & carpeting output fell 0.6% (+1.4% y/y) for the first monthly decline since August. Computer output rose 1.2% (-5.2% y/y) was strong for the third consecutive month.

Output of business equipment rose 1.0% (-2.8% y/y) following a sharp 1.2% December decline. Output of information processing equipment rose 1.2% (-0.5% y/y) following two down months. Output of transit equipment rose 1.2% (-14.6% y/y) following the 4.8% December collapse.

Capacity utilization rose but remained near the 2002 average.

| Production & Capacity | Jan | Dec | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Industrial Production | 0.7% | -0.5% | 1.9% | -0.7% | -3.5% | 4.7% |

| Capacity Utilization | 75.7% | 75.2% | 75.0%(1/02) | 75.6% | 77.3% | 82.7% |

by Tom Moeller February 14, 2003

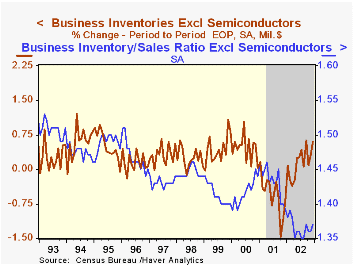

Total business inventories rose more than expected in December. It was the eighth consecutive month of accumulation.

The effort to accumulate inventory has been sufficient to pull the inventory to sales ratio off record low levels but has generated only modest gains in industrial production.

Retail inventories rose strongly led by strong gains across the board. Auto inventories rose just 0.1% but were up 18.9% y/y.

Nonauto retail inventories clearly turned the corner toward accumulation as inventories at apparel stores jumped 1.1% (4.1% y/y). At general merchandise stores inventories surged 1.3% (2.7% y/y), the second consecutive month of accumulation at that rate. Inventories of building materials jumped 1.2% (6.6% y/y) for the third double digit gain in the last four months.

Overall business sales rose 0.2% (3.7% y/y). Gains in 4Q eased markedly from 2Q and 3Q.

The inventory-to-sales ratio rose to 1.37, off the monthly lows but on a quarterly basis stable at 1.36 since 2Q.

| Business Inventories | Dec | Nov | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Total | 0.6% | 0.3% | 1.9% | 1.9% | -6.4% | 5.6% |

| Retail | 0.6% | 0.8% | 5.3% | 7.7% | -5.0% | 6.1% |

| Retail excl. Autos | 0.8% | 0.5% | 3.1% | 3.1% | -2.1% | 4.1% |

| Wholesale | 0.8% | 0.3% | -0.0% | -0.0% | -5.7% | 6.6% |

| Manufacturing | 0.5% | -0.2% | -2.0% | -2.0% | -8.0% | 4.5% |

by Tom Moeller February 14, 2003

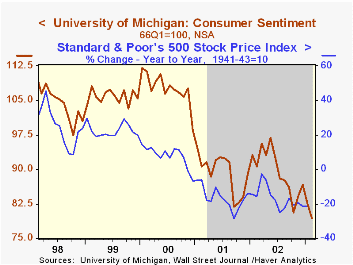

The mid-February reading of Consumer Sentiment from the University of Michigan fell 3.9% from January to a level of 79.2. The figure is versus Consensus expectations for 82.0.

The index of current conditions fell moderately. The expectations index fell sharply for the second month and was down roughly 15% over the period.

Over the last 10 years there has been a 52% correlation between the level of consumer sentiment and the y/y change in the S&P 500. That correlation rose to 86% during the last five years.

The University of Michigan survey is not seasonally adjusted.

| University of Michigan | Mid-Feb | Jan | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 79.2 | 82.4 | -12.7% | 89.6 | 89.2 | 107.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief