Global| Jul 10 2002

Global| Jul 10 2002Import Prices Fell Sharply

by:Tom Moeller

|in:Economy in Brief

Summary

Prices for imported commodities fell much more than expected last month versus May. Consensus estimates were for a 0.2% gain. May figures were little revised. Petroleum import prices fell for the first month this year. So far in July, [...]

Prices for imported commodities fell much more than expected last month versus May. Consensus estimates were for a 0.2% gain. May figures were little revised.

Petroleum import prices fell for the first month this year. So far in July, the price of Arab Light crude oil has averaged roughly $22.64/bbl versus $22.00 in June.

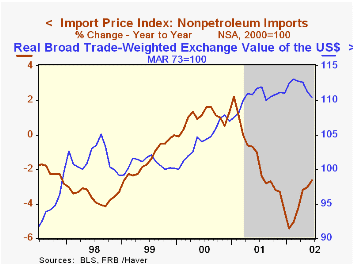

Nonpetroleum import prices rose slightly for just the third month this year.

Prices for imported capital goods were unchanged and are down 1.1% YTD. Nonauto consumer goods prices were flat for the second consecutive month, down 0.6% YTD and auto prices rose slightly.

Export prices were flat, mostly reflecting a jump in food prices that were offset be sharply lower prices of capital goods.

| Import/Export Prices (NSA) | June | May | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Import - All Commodities | -0.6% | 0.1% | -3.9% | -3.5% | 6.5% | 0.9% |

| Petroleum | -6.6% | 1.6% | -7.9% | -17.2% | 66.5% | 34.2% |

| Nonpetroleum | 0.1% | -0.1% | -2.6% | -1.5% | 1.0% | -1.4% |

| Export - All Commodities | 0.0% | -0.1% | -1.5% | -0.8% | 1.6% | -1.3% |

by Tom Moeller July 10, 2002

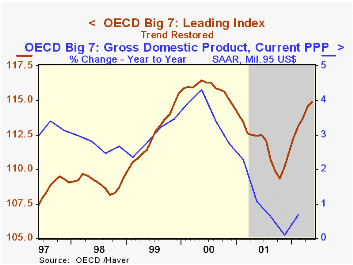

Prospects for improved real economic growth recently have improved, according to the OECD Index of Leading Indicators. Since November, the index has been trending higher, although the rate of improvement has slowed somewhat in the last three months

Real economic growth in the Big Seven OECD countries surged 4.4% (AR) in 1Q02. That followed three consecutive negative growth quarters. The surge was due to strong 6.1% growth in the US as well as 5.7% growth in Japan. Growth in the European Union was 0.7% after a 0.5% 4Q decline.

In Japan, industrial production has been climbing steadily since the lows of this past winter. Production gains in Germany also have been positive but moderate.

Inflation in Big Seven countries has been tame, with the Implicit Price deflator up 1.7% y/y. A 2.9% 1Q surge followed a decline in 4Q prices. The CPI in Japan was down 0.9% y/y in May though prices may have showed signs of stabilizing in recent months.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief