Global| Mar 26 2021

Global| Mar 26 2021IFO Indexes Move Sharply Higher But Are Still Lacking

Summary

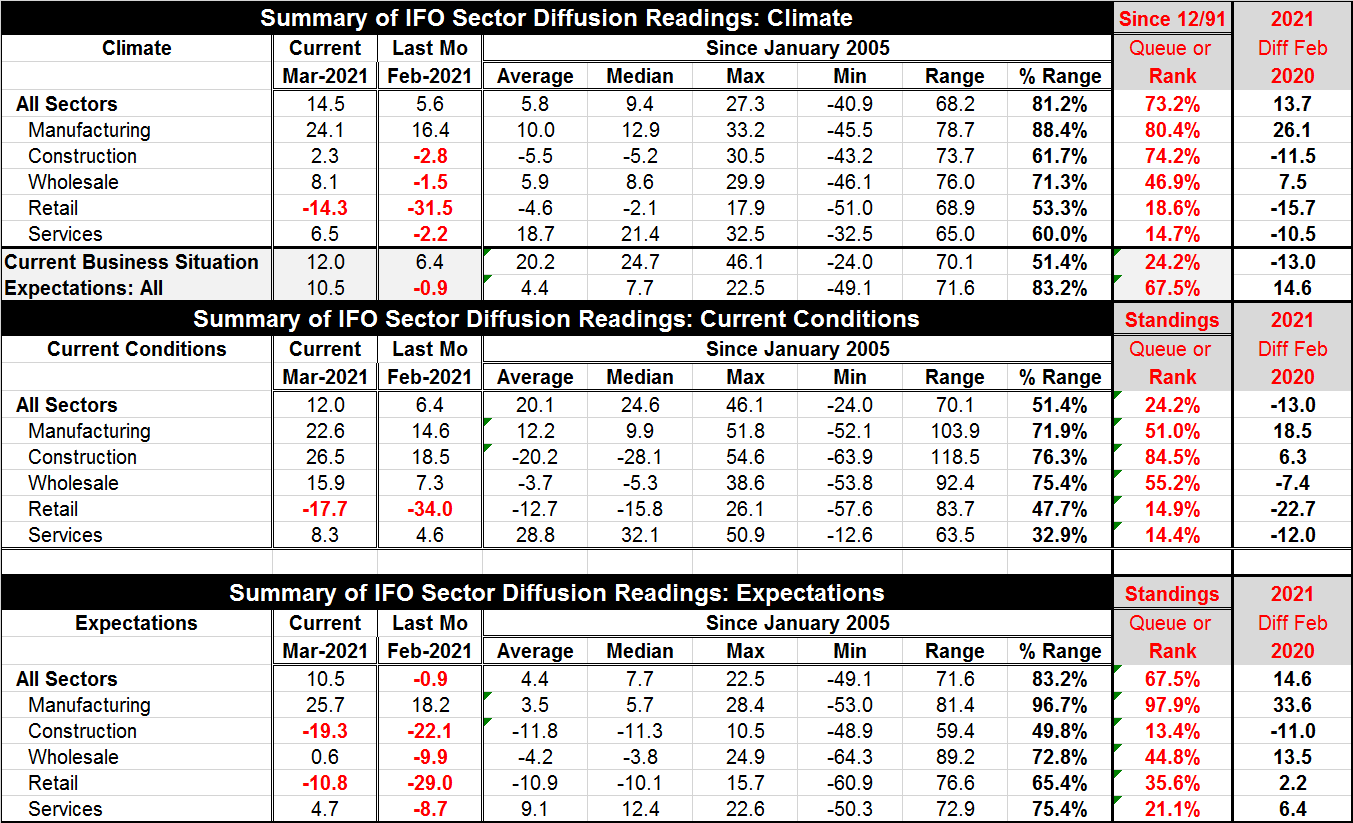

The IFO indexes moved higher in March. The chart plots the indexes while the table presents sector results and aggregate gauges based on diffusion indexes. The graph shows a very strong gain in business expectations and a solid rise [...]

The IFO indexes moved higher in March. The chart plots the indexes while the table presents sector results and aggregate gauges based on diffusion indexes. The graph shows a very strong gain in business expectations and a solid rise in current conditions and in climate.

The IFO indexes moved higher in March. The chart plots the indexes while the table presents sector results and aggregate gauges based on diffusion indexes. The graph shows a very strong gain in business expectations and a solid rise in current conditions and in climate.

The climate headline is firm

The all-sector climate reading rose to 14.5 in March from 5.6 in February. Since 1995 that is the fourth strongest one-month change on record. It has boosted the climate index to a 73rd percentile queue standing. That is a moderately strong reading. For context, on diffusion data the median lies at a queue standing of 50%. Also, the climate reading is now 13.7 points above where it stood just before the virus struck in February of last year.

Climate gauge

The details of the climate gauge are a bit trickier. The sector readings show what I means since manufacturing has a strong 80.4% standing on climate, construction has a 74.2 percentile standing, wholesaling is below its median at a 46.9 percentile standing, retail checks in at an 18.6 percentile standing with services at a very weak 14.7 percentile standing. The headline does not begin to capture this diversity. Climate overall has a nice firm standing. But jobs tend to be in the service sector where conditions are weakest and weak. It is the low-employment manufacturing and construction sectors that have strong readings. It is probably a good idea not to try to evaluate the IFO based on headlines just yet because of those differences among sectors and the peculiarities of what they might mean.

Current conditions

The current conditions reading also brings us back to earth. Here the change from February 2020 is still a negative number. The current all-sector reading is some 13 diffusion points lower than it was before the virus struck. And the queue standing of the all-sector diffusion index is in its 24.2 percentile, well below its historic median. The strongest current reading is in construction at its 84.5 percentile followed by wholesaling then manufacturing at 51. After that, retailing and services come in with rankings below their respective 15th percentiles. Retailing is some 22 points below its February 2020 level. Among other current indexes, only manufacturing and construction show gains compared to February of last year.

Expectations

All-sector expectations are up by 11.4 points on the month and have a 67.5 percentile queue standing; they are 14.6 points above their value in February 2020. As an overview, that is pretty good. But expectations are not uniformly solid. There is a lot of weakness despite the solid headline reading. Manufacturing with its 97.9 percentile standing is a big part of the reason that expectations overall look so strong. But once we get past that sector, wholesaling at a below median 44.8 percentile standing is the next best, followed by retailing at 35.6%, services at 21.1% and construction sitting at the bottom of the heap with a 13.4 percentile standing.

Summing up

Germany is still fighting off virus effects as we detailed in earlier reports. It is reported to be applying more stringent border screening as well. In the EU summit of yesterday, it is far from clear what the EU decided. We are told that it did not put on vaccine export controls but that it does expect AstraZeneca to give the EU priority. It looks a lot like a veiled threat. To be sure, the EU is behind in vaccinating its people, but at the start of the process, vaccinations are a zero sum game. The EU can’t get more without giving someone else less. And since it was slow in ordering, its rightful place is back in the queue and the EU is unwilling to accept that. As long as EU vaccinations lag the growth stories from the EMU and EMU member countries are going to be cautious and shaded toward weakness. The German IFO headlines look pretty good this month, but on closer inspection, Germany still has a long way to go to achieve normalization.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief