Global| Jul 31 2007

Global| Jul 31 2007IFO Detail Fills in the Missing Pieces for Germany’s Trends…Strong but Slowing

Summary

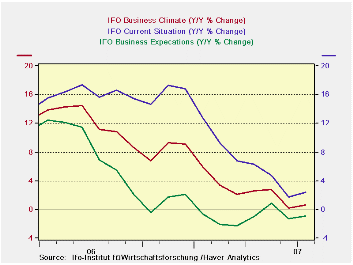

The main IFO gauges show that while the current readings for IFO are still very strong, the current indices are trending lower. As index numbers the index for expectations hit a bit of a ceiling and has formed what is essentially a [...]

The main IFO gauges show that while the current readings for IFO are still very strong, the current indices are trending lower. As index numbers the index for expectations hit a bit of a ceiling and has formed what is essentially a double top. Expectations rarely get much stronger than an index reading of 105. The accompanying chart shows these indexes as percent changes and the downward slide of momentum is apparent.

Now, as the IFO gauges began to poster lower numbers, we look to see what the detail of the IFO report tells us about that step-back.

In terms of Y/Y percentage changes the current situation index continued to rise. However MFG is now lower Y/Y as it has been for two months running. Not shown in the table below is the detail for wholesaling which has fallen for the second straight month or construction, now off for three months in a row. Retailing is up in July after being off Yr/Yr in June.

Expectations are off across most main sectors with the MFG index off by 0.5% Yr/Yr and off on that basis for five of the past six months. Wholesaling expectations are off for one month in a row; retail is off for three months in a row and for five of the past six months.

Within MFG the overall sector shows a decline in activity Yr/Yr and that decline is seen in intermediate goods and consumer goods but capital goods activity rebounded in July after having made its first Y/Y drop in June.

Assessments of demand for MFG sectors are dropping in most sectors and have been dropping for five months more or less. The exception is the consumer sector where demand is seen as up in July; it was also up in May.

Also in MFG, orders on hand are somewhat mixed. The total is lower Y/r (-2.7%). But that is mostly weakness in intermediate goods since capital goods orders and consumer goods are still growing.

Foreign orders continue to grow, by 1.9% in all of MFG but intermediate orders are off. Foreign capital goods orders are up strongly but are slowing their rate of ascent; consumer goods orders are flat.

The outlook for three months ahead (bottom panel of table) is still mostly positive, but with some mixed trends. MFG export expectations are flat, despite good orders responses above. Orders expectations for retailing are on a long string of declines although the pace of decline is withering. Wholesale orders are positive but their strength is withering. Export expectations for three months ahead have turned flat for manufacturing in July. Employment expectations over the next three months do continue to be upbeat.

The German economy still is emitting a lot of very positive signals. However do not get lost in the high level of the indexes since they are also losing momentum. While retailing seems to be one improving sector its ability to offset slippage elsewhere has not been established.

| Percent: Yr/Yr | INDEX NUMBERS | ||||||||

| Jul-07 | Jun-07 | May-07 | Apr-07 | Mar-07 | CURRENT | Average | Curr/Avg | Percentile | |

| Biz Climate | 0.7% | 0.2% | 2.8% | 2.6% | 2.1% | 106.4 | 95.7 | 111.2% | 90.3% |

| Current Situation | 2.4% | 1.7% | 4.7% | 6.3% | 6.7% | 111.3 | 94.7 | 117.5% | 87.6% |

| Biz Expectations: Next 6-Mos | -0.9% | -1.2% | 0.9% | -0.9% | -2.3% | 101.8 | 96.7 | 105.3% | 82.9% |

| Jul-07 | Jun-07 | May-07 | Apr-07 | Mar-07 | CURRENT | Average | Curr/Avg | Percentile | |

| Current Situation | |||||||||

| MFG | 4.5% | 4.4% | 6.6% | 7.6% | 9.4% | 111.3 | 92.2 | 120.8% | 95.3% |

| Biz Expectations: Next 6-Mos | |||||||||

| MFG | -0.5% | -2.8% | 0.9% | -1.4% | -3.0% | 100.9 | 96.4 | 104.7% | 79.1% |

| Activity (m/m) | |||||||||

| MFG | -1.8% | -3.7% | 2.0% | -0.5% | 0.4% | 102.9 | 96.9 | 106.2% | 77.8% |

| Demand M/M | |||||||||

| MFG | -3.3% | -7.1% | 0.4% | -3.6% | -1.7% | 101.2 | 97.0 | 104.3% | 68.5% |

| Orders on hand | |||||||||

| MFG | -2.7% | -3.6% | -0.9% | -3.0% | -2.7% | 104.0 | 96.4 | 107.9% | 79.0% |

| Foreign orders on hand | |||||||||

| MFG | 1.9% | 2.0% | 2.5% | 1.9% | 5.4% | 111.5 | 94.2 | 118.3% | 96.5% |

| Yr/Yr percentage changes in underlying Indices | |||||||||

| IFO outlook for 3-Months ahead | |||||||||

| 3-Mos ahead | Percent: Yr/Yr | INDEX NUMBERS | |||||||

| Expected Activity | Jul-07 | Jun-07 | May-07 | Apr-07 | Mar-07 | CURRENT | Average | Curr/Avg | Percentile |

| MFG | 1.0% | 3.4% | 0.5% | 0.7% | -1.6% | 103.0 | 96.7 | 106.5% | 94.0% |

| Orders expectations | |||||||||

| Retail Order Expectations | -1.2% | -10.8% | -4.6% | -10.9% | -10.0% | -11.6 | -17.5 | 66.5% | 70.6% |

| Wholesale | 0.7% | 5.7% | 15.7% | 15.0% | 10.7% | 7.1 | -14.0 | -50.7% | 83.1% |

| EXPORT Biz Expectations | |||||||||

| MFG | 0.0% | 0.4% | -0.5% | -1.1% | -1.9% | 103.5 | 98.3 | 105.3% | 89.4% |

| Employment Expectations | |||||||||

| MFG | 7.4% | 8.4% | 7.5% | 6.4% | 8.2% | 105.9 | 95.9 | 110.4% | 100.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief