Global| Aug 16 2007

Global| Aug 16 2007HICP is Losing Momentum

Summary

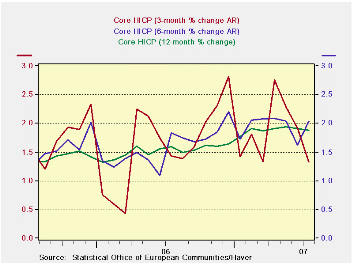

Inflation trends are peaking and falling in the Euro area with the key core measure. Still that core measure is hugging the 2% ceiling rate for the overall HICP. While Year/year inflation is lower and 3-month inflation is lower [...]

Inflation trends are peaking and falling in the Euro area with the key core measure. Still that core measure is hugging the 2% ceiling rate for the overall HICP. While Year/year inflation is lower and 3-month inflation is lower 6-month inflation is NOT.

Overall and core rate of inflation are mostly conforming to the ECB ceiling across major countries. There is no sense of accelerating inflation in this group and that is certainly good news. The bad news is that the trends for the components of inflation are more decidedly mixed. While goods price inflation is still falling (and that one contains oil and gas price effects), services inflation is high and accelerating. It may contain some energy price impacts as well, but the speed right now is over the top of acceptability. Internal inflation (services) can be more stubborn than goods inflation. These days, due to international competition, goods price inflation tends to be better behaved. Pressure from services prices tends to be longer lived while goods price oscillations may not be so permanent. As a result the drop in goods prices that helped to contain the overall HICP is to be closely watched in the coming months. We obviously want to see as well the service sector trends and how much they are able to deflate.

| M/M % Change | % SAAR | ||||||

| Jul-07 | Jun-07 | May-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.1% | 0.2% | 0.2% | 2.0% | 2.6% | 1.8% | 2.4% |

| Core | 0.1% | 0.1% | 0.1% | 1.3% | 2.0% | 1.9% | 1.6% |

| Goods | -1.0% | 0.0% | 0.2% | -2.9% | 2.6% | 1.2% | 2.7% |

| Services | 0.8% | 0.2% | 0.2% | 5.2% | 4.5% | 2.6% | 2.1% |

| HICP | |||||||

| Germany | 0.2% | 0.2% | 0.2% | 2.3% | 2.5% | 2.0% | 2.1% |

| France | 0.0% | 0.2% | 0.2% | 2.0% | 2.1% | 1.2% | 2.2% |

| Italy | -0.1% | 0.3% | 0.3% | 1.9% | 2.7% | 1.7% | 2.3% |

| UK | -0.3% | 0.3% | 0.1% | 0.4% | 1.5% | 1.9% | 2.4% |

| Spain | 0.2% | 0.3% | 0.3% | 3.1% | 3.4% | 2.3% | 4.0% |

| Core:xFE&A | |||||||

| Germany | 0.2% | 0.1% | 0.3% | 2.4% | 2.4% | 2.1% | 1.0% |

| France | 0.0% | 0.1% | 0.1% | 1.1% | 1.3% | 1.4% | 1.5% |

| Italy | 0.0% | 0.1% | 0.2% | 1.2% | 3.0% | 1.8% | 1.7% |

| UK | -0.1% | 0.1% | 0.3% | 1.2% | 1.6% | 1.8% | 1.2% |

| Spain | 0.2% | 0.2% | 0.1% | 2.2% | 2.3% | 2.4% | 3.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief