Global| Dec 17 2019

Global| Dec 17 2019Has Europe's Trade Trend Turned?

Summary

Europe's trade trend this month but is it sustainable? Two aspects of the EMU trade trend are notable. One is that exports are accelerating. And export acceleration applies to manufactured exports and pretty-much to nonmanufacturing [...]

Europe's trade trend this month but is it sustainable?

Europe's trade trend this month but is it sustainable?

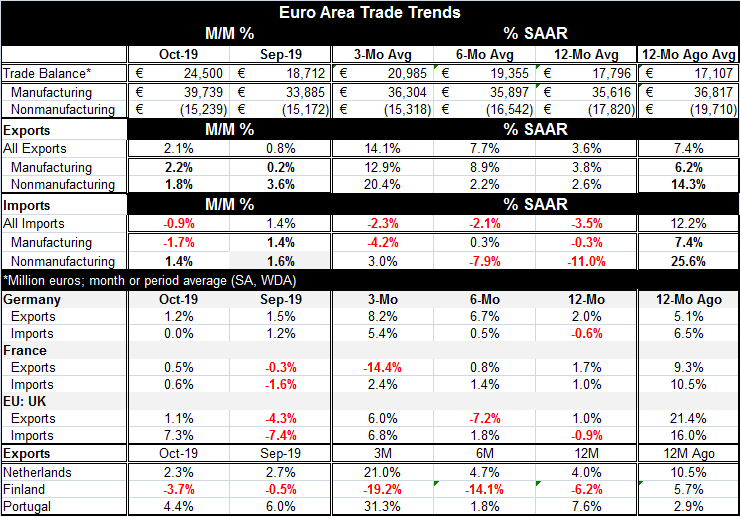

Two aspects of the EMU trade trend are notable. One is that exports are accelerating. And export acceleration applies to manufactured exports and pretty-much to nonmanufacturing exports as well (slight exception because of slightly weaker growth over six months- with the emphasis on 'slightly'). The second trend is weak imports as import growth is negative over all horizons, but overall it is only declining not decelerating. However, manufactured imports are closer to showing actual deceleration. Nonmanufacturing imports sequentially show growth rate improvement but still decline over 12 months and six months. However, the year-on-year trend (see Chart) clearly show a steady, ongoing, import deceleration as exports stabilized and began a recent acceleration.

What we would like to see for a sustainable trend would growth in both series with exports growing a bit faster than imports and for those trends to be clearly present in manufacturing trade. Over time imports should grow because GDP grows and imports, of course, are an outcropping of domestic demand. When the trade balance trend is driven by falling imports, it's a sign of a cyclical trend and one related to oncoming economic issues (possibly recession). For these reasons, the EMU trade trend, while clearly driving the surplus to a higher level (a much higher surplus on the month as the chart shows), is still not one that looks to be sustainable.

In the details in the lower panels of the table, German exports show accelerating trends while French exports show decelerating trends and French exports even decline on balance over three months. German import trends are accelerating as are French imports contrary to the EMU-wide pattern (still the French nominal growth rates are very low). The U.K. shows accelerating import trends and a wild mixture of growth rates for exports over 12 months, six months and three months. There is no trend there.

The exports of other early reporting EMU members show idiosyncratic patterns. Dutch exports show acceleration and growth. Portugal demonstrates a somewhat erratic tendency to accelerate. Finland's exports are simply imploding and decelerating strongly from 12-months, to six-months to three-months.

Trade for the EMU while showing some strong overall trends seem to have uneven underpinnings as well as mixed fundamentals in their trends. The export side of things actually is a good bit brighter and more consistent. But without more consistency in imports, the overall trade picture is still incomplete.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief