Global| May 07 2015

Global| May 07 2015Grim News from Germany Despite Order Rebound

Summary

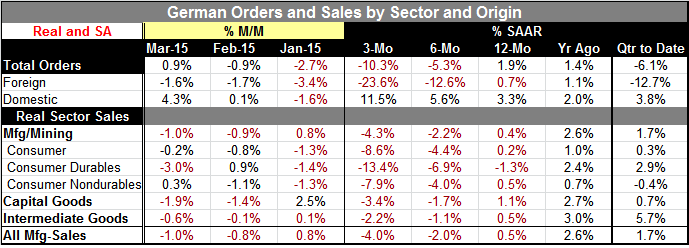

German real orders rose by 0.9% in March after two months of falling. Orders, however, are still falling at a 6.1% annual rate in the just completed first quarter. But this drop is not the reason for my pessimism over this report. [...]

German real orders rose by 0.9% in March after two months of falling. Orders, however, are still falling at a 6.1% annual rate in the just completed first quarter. But this drop is not the reason for my pessimism over this report.

German real orders rose by 0.9% in March after two months of falling. Orders, however, are still falling at a 6.1% annual rate in the just completed first quarter. But this drop is not the reason for my pessimism over this report.

What distresses me about this report is that with Germany as the hands-down most competitive economy in Europe and running one of the largest current account surpluses in the world and with the euro exchange rate having fallen substantially this year, German foreign orders are still contracting. Overall orders are up in March wholly on the back of a 4.3% hike in domestic orders as foreign orders are lower by 1.6%. Foreign orders are lower for three months in a row and in four of the last five months. Foreign orders are falling at a 23.6% annual rate over three months. That's not good news.

If German foreign orders are doing this badly, what can we expect from anyone else? Or, put another way, if the most competitive advanced economy in the world that is further underpinned by a very weak exchange rate cannot mount an increase in foreign orders, then the global economy must be doing even worse than we thought. That is a frightening thought. Everyone has been looking for growth to accelerate. The U.S. was accelerating. The ECB implemented a new QE program. The global economy was supposed to be on the mend. Has it instead caught a snag and is it unraveling?

We have recently chronicled the results of the Markit PMI data that show services are leading the euro area higher as manufacturing has remained weak. According to the orders data, German manufacturing has turned inward as only domestic orders are expanding. Foreign orders are up by just 0.7% over 12 months while domestic orders are up by 3.3% on that period. None of this is going to stoke much growth.

Also, inflation adjusted German sales (real sector sales in the bottom section of the table) are weak across the board with sales falling in each and every category over three months over six months and decelerating year-over-year over 12 months compared to the previous 12 months. That is pretty grim too.

Germany is an economy led by its foreign sector and capital goods prowess. What we see instead is a German economy forced to limp ahead and being led by its services sector - that is very un-German. While there appears to be some domestic business on the books, I am very worried about what the weakness in German foreign orders means for the rest of the world as well for Germany.

Is growth worldwide slowing faster than we thought? Is there some German idiosyncrasy operating? Of course, with the strong dollar we are seeing a sympathetic weakness in the U.S. economy and even worse weakness in the U.S. manufacturing PMI gauge (the manufacturing ISM). In the U.S. as in Germany, the nonmanufacturing sector is helping move growth ahead but the lack of manufacturing strength is still a worry.

I mark this as a negative report despite a headline that will likely be embraced by markets. The old saying is that the devil is in the details and that surely is true of this report. On the day, Germany is not in the markets' sights. Today is a day to watch the elections in the U.K. Also the news for Greece suggests that it is still being stubborn about what it is willing to continue to say it will try to do in exchange for more funds. All of these events probably are higher on the list of what the market is reacting to today. Yet, the real troubling news on the day is from Germany, but the wolf is hiding in sheep's clothing and for now his secret remains unrevealed. When will we see the broader impact of the abject weakness that this report only hints at?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief