Global| Nov 11 2013

Global| Nov 11 2013Greek Trade Trends Set to Sour

Summary

For most of the period since the financial crisis ended, Greek exports continued to outpace weak imports. But over the last year exports have fallen by 2.3% while imports have risen by 2.0%. As a result of that mix, the Greek [...]

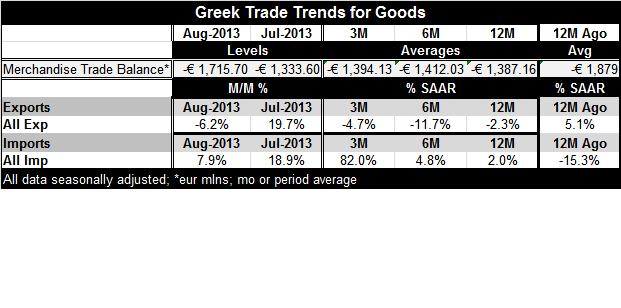

For most of the period since the financial crisis ended, Greek exports continued to outpace weak imports. But over the last year exports have fallen by 2.3% while imports have risen by 2.0%. As a result of that mix, the Greek merchandise trade balance went from a deficit of ?1.39 billion in August 2012 to a deficit of ?1.71 billion in August 2013.

For most of the period since the financial crisis ended, Greek exports continued to outpace weak imports. But over the last year exports have fallen by 2.3% while imports have risen by 2.0%. As a result of that mix, the Greek merchandise trade balance went from a deficit of ?1.39 billion in August 2012 to a deficit of ?1.71 billion in August 2013.

Within the last year trends have developed to keep this trend in place; over 6 months exports have fallen at an 11.7% annual rate while imports have risen at a 4.8% annual rate. Over three months results are quite stark. Imports have surged at an 82% annual rate, while over the same period exports have fallen at a 4.7% annual rate.

It is not quite clear what these growth metrics are telling us, but some of the implications of this shift are quite clear.

Since the year 2010 Greek exports have actually been faring quite well despite the problems in the country. And over that same period, especially since the year 2010, Greek imports have been weak. Now suddenly these relationships are flip flopping.

The Greek economy is still under a great deal of pressure and is still being pressed to make even more reforms in order to get its next tranche of funds from the Troika. Yet import demand is starting to elevate. And, surprisingly, Greek exports that had been making headway seem to have slowed. The table shows that Greek exports have slowed over the past year rather consistently; the drop off does not seem to be something that has come and, now will go. There is no special reason for it.

The import revival seems to say good things about Greek domestic demand. Perhaps some of it is a revival of tourism. But the drop in Greek exports says something bad about the evolution of Greek competitiveness. And the combination will widen the Greek trade deficit as we have seen over the past year. That will get Greece deeper into debt- if anyone will lend to them. While the revival of demand is a good sign, the further loss of competiveness at a time that past reforms were supposed to have helped to boost competitiveness is surely a bad one. The Greek economic response to the policies imposed by the Troika remains elusive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief