Global| Dec 01 2016

Global| Dec 01 2016Global PMIs Are Improving But Mixed

Summary

The Markit finalized PMI gauges ticked higher in November on balance. The unweighted average moved up to 51.7 in November from 51.5 in October and its average has been steadily rising when calculated over 12 months, six months and [...]

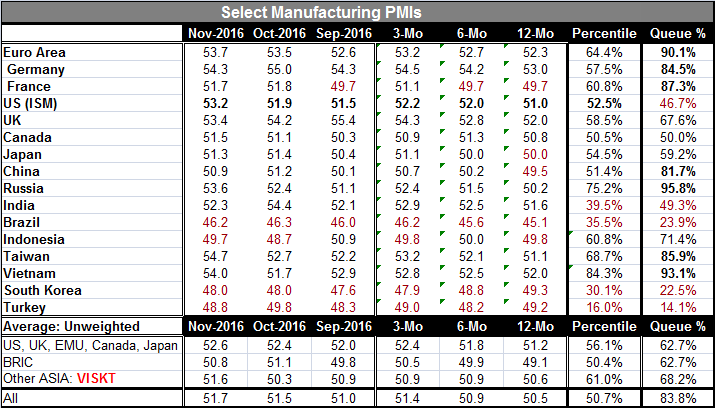

The Markit finalized PMI gauges ticked higher in November on balance. The unweighted average moved up to 51.7 in November from 51.5 in October and its average has been steadily rising when calculated over 12 months, six months and three months. The overall unweighted average stands in the 83rd percentile of its unweighted queue of values back to January 2011. That's a pretty strong reading, but it may not be reflective of what the global manufacturing sector is actually experiencing. That ranking is only a comparative standing over the past six years when conditions have been weak.

The Markit finalized PMI gauges ticked higher in November on balance. The unweighted average moved up to 51.7 in November from 51.5 in October and its average has been steadily rising when calculated over 12 months, six months and three months. The overall unweighted average stands in the 83rd percentile of its unweighted queue of values back to January 2011. That's a pretty strong reading, but it may not be reflective of what the global manufacturing sector is actually experiencing. That ranking is only a comparative standing over the past six years when conditions have been weak.

Only four countries have manufacturing sectors with indices below 50, showing contraction in November. They are Brazil, Indonesia, South Korea and Turkey. Four countries have queue percentile standings that place the current manufacturing observation below its roughly six year median. They are the United States, India, Brazil, South Korea and Turkey. Only Canada, Indonesia and South Korea have weakened on balance over three months compared to six months. Only South Korea is weaker over three months than over 12 months but on that basis Indonesia is unchanged. There is a clear case to be made for saying the global manufacturing sector is improving and few are in truly dire straits.

Despite the strong move up by the U.S. PMI, it continues to underperform its median since January 2011. The euro area is doing especially well with a PMI reading of 53.7 that resides in the top 10% of its observations over the last six years. France and Germany have roughly top 15% performances over that period as of November.

While the global average has been moving higher, it is moving up at a slow pace. Seven countries' manufacturing sectors out of 16 reported in the table worsened month-to-month. China continues to report out a borderline manufacturing reading. It is technically expanding but has little margin over the line that separates expansion from contraction. We are still holding our breath on China.

We are making a lot here out of some very small differences and we need to be aware of it. This month the dispersion among the PMI values in the table stands only at its 53rd percentile when ranked over the last six years - a more or less normal reading. But just three and four months ago the dispersion ranking was in its bottom 20th percentile - quite weak. Firms are showing highly similar PMI numbers in manufacturing; the notion of separation is new. And the PMI readings/rankings are only starting to get up to and above readings of normalcy in many places. Five of 16 countries have queue PMI standings below their medians (of the past six years). There are seven countries with standings in their 80th to 90th percentiles with few left in the middle. It is now a sort of feast or famine recovery. But even that fails to adequately describe what this recovery is like.

Looking back at a full U.S. history of ISM values, since the ISM makes long data series freely available back to the 1950s, we find that the average ISM value over various six-year periods in the U.S. is in the range of 53. Only the U.S., the U.K., Canada and India have PMIs averages near that value in the 52 to 53 range. For the weakest reporters, France (48.7), South Korea (49.5), China (49.7), and others with averages in the range of 50 to 50.9 (Vietnam, Taiwan, Russia, China, and the euro area). These evaluations are being made against a period of depressed economic conditions. The relatively high current rankings are misleading because the standard for comparison is so poor. For example, the EMU at a diffusion 53.7 reading exceeds the U.S. reading of 53.2, but its queue standing at its 90.1 percentile is distorted compared to the U.S. where the standing at its 46.7 percentile, below its median and for a reading highly similar to the EMU reading.

On the whole, global manufacturing is still limping ahead. We can take heart from the gathering strength. But conditions are still far from ideal or even normal and are still well-short of 'good.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief