Global| Feb 20 2020

Global| Feb 20 2020GfK Consumer Climate Readings for Germany Continue to Erode

Summary

The German consumer sentiment projection for March is available way ahead of consumer readings for Italy, France and the United Kingdom. There is erosion present in the German data and some of that is put at the feet of the [...]

The German consumer sentiment projection for March is available way ahead of consumer readings for Italy, France and the United Kingdom. There is erosion present in the German data and some of that is put at the feet of the Coronavirus.

The German consumer sentiment projection for March is available way ahead of consumer readings for Italy, France and the United Kingdom. There is erosion present in the German data and some of that is put at the feet of the Coronavirus.

The global threat

The global economy, the IMF, WHO, economists and the Fed still don't know quite what to make of the Coronavirus threat. China is in the trenches fighting with it and has reported fewer infections over the last several days. But China has too much 'skin in the game' and has played too fast and loose with the numbers for its 'reports' to be taken at face value. Maybe the spread is slowing, maybe it is plateauing...and maybe not.

The virus beyond China

Iran that has reported no infections has just reported two deaths that it thinks are virus-related. Death does not occur without infection. And not all who are infected die. That leads to the supposition that there may be more and potentially many more cases of Coronavirus undiagnosed and spreading without any detection or control in Iran. The IMF has called the virus a threat. In its just released minutes, the Fed tells us it is carefully watching. You can't fault that but once action become necessary – if it does- it's hard to see how to fight a virus with monetary policy. Basically, I am arguing that the virus will be a steamroller if it is not contained. The cruise ship docked in Yokohama is an example of what damage it can do. It can't be ignored. Hoping that it will slow or go away of its own accord is not a viable plan.

Germany under pressure

Germany is laboring under several different strains. The Bundesbank has urged the use of fiscal stimulus to bolster the economy. Meanwhile, Germans are pressuring the ECB to bring interest rates up to a more normal level and to jettison negative rates- others are wary that such actions may have growth consequences that could be untimely. The ZEW experts have just cut back their assessments of conditions for future growth in Germany and the EMU. And they see inflation forces as weaker. The virus has played a part this shift. Germany also faces ongoing domestic dislocations as the recent bar-shooting of migrants demonstrates. Angela Merkel's handpicked successor is dropping out having failed to fill Angela's shoes and now the political leadership of Germany is in doubt. German economic data continue to tell a story of an economy under strain. Ironically the consumer readings remain among some of the more buoyant assessments of the economy.

German consumer climate

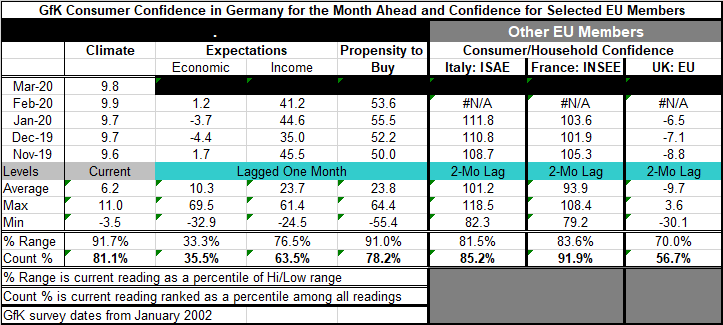

The GfK climate reading has eroded steadily since late-2017. It has recently showed some firmness, but with the March reading it is flattening out again. Economic and income expectations have been eroding. Economic expectations have been falling and falling fast since early-2018. However, they have recently begun to hover near the bottom on their two-decade range. Income expectations made a high, broad, plateau from about 2014-2017 – albeit with come volatility. But since early-2018, income expectations have begun to slide leaving that reading considerably lower than it has been since 2014. The 'propensity to buy' reading is also 'somewhat stable' since 2014, but a close look shows an eroding reading with a downtrend over that span.

Queue standing evaluations

As a result of all these ups and downs, the queue standing for climate is at its 81st percentile, still a strong reading. Economic expectations have a low 35.5 percentile standing; income expectations have a moderate still-above-median 63.5 percentile standing. The 'propensity to buy' has a 78.2 percentile standing. And of course, the German unemployment rate continues to hover at a post-unification low.

New threats?

And while there are no new reports of an influx of migrants, the new Syrian offensive has made more people homeless there than ever before. There could be another wave of migration ready to assail the EU.

Consumer attitudes elsewhere

On data up-to-date only through January, Italy shows some firming trends in confidence. The French consumer has been losing some ground. The U.K. is seeing improvement but on still net negative readings. French confidence has a 91.9 percentile standing; Italy has an 85.2 percentile standing; and the U.K. has a 56.7 percentile standing.

Consumers are surprisingly buoyant

Consumers continue to exude much more confidence and show higher readings of satisfaction than do most simple indicators of economic performance. For example, Europe (EMU), Germany, France, Italy and the U.K. GDP figures have been disappointing. Italy and France both showed a drop in GDP in Q4. German GDP rose by just 0.1% (annualized!). France, Germany, Italy and the EMU all have year-on-year growth rates for GDP below 1%. The U.K. logged a year-on-year gain of 1.1%. Obviously, the economy is not doing all that well but unemployment rates are 'universally' low across Europe and that largely explains the much higher evaluation for consumer attitudes.

The threat of Coronavirus...on top of everything else

In calling the Coronavirus a threat, the IMF is trying to make sure that it is being taken seriously. The disease, while global in reach, is not deemed to be a pandemic since it does not yet show that it is spreading independently in areas outside China (except perhaps for the cruise ship in Yokohama; that is clearly a special case- but one to learn from). The flu has been and still is hitting China hard. China is a large economy and the knock-on impact to global commodity prices has been severe. There are also supply chain issues that affect industries and companies differently since not all firms source non-China destined parts from factories inside China. But some do. Germany is very plugged into the global economy. That is why events that impact global trade are a big problem for Germany. German exports plus imports are 88% of nominal GDP. No other major economy in the world is as exposed to international events. This kind of diversification has given German growth resilience. And that works until it doesn't. In this environment with U.S. sanctions slapped on Russia, then on Iran, with the U.S.-China trade war taking its toll and now the Coronavirus and next - who knows what will happen to German access to the U.K. market when the Brexit transition deal is struck? Germany has seen various export markets implode one after the other. There is still a U.S.-EU trade deal pending. The German economy is reeling; yet, it has not shown persistent GDP declines and the job market has been insulated. But for how much longer can that miracle last?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief