Global| Nov 19 2013

Global| Nov 19 2013Germany's ZEW Barometer Improves- But for How Long?

Summary

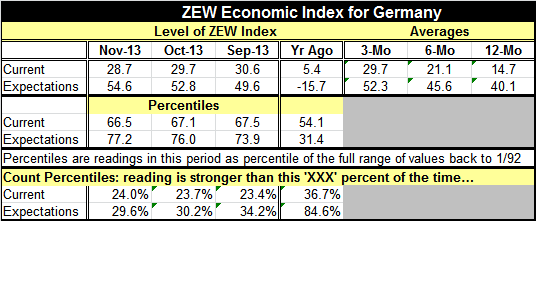

The main focus for watchers of the ZEW index is its expectations reading. That reading rose to 54.6 in November from 52.8 in October. The current index declined to 28.7 from October's 29.7. The two indices are now roughly at the same [...]

The main focus for watchers of the ZEW index is its expectations reading. That reading rose to 54.6 in November from 52.8 in October. The current index declined to 28.7 from October's 29.7.

The main focus for watchers of the ZEW index is its expectations reading. That reading rose to 54.6 in November from 52.8 in October. The current index declined to 28.7 from October's 29.7.

The two indices are now roughly at the same relative position in their historic ranges and generally this configuration does not last. The expectations index is higher only 29.6% of the time and the current index is higher only 24% of the time. These readings are not always so synchronous. For example, we would expect, if the current reading were extremely high, that the expectations reading would be much lower. The ZEW survey participants would recognize that the economy does not stay at such a strong pitch for too long and would downgrade expectations. We see that in the chart in the behavior of the ZEW index components in late 2010 and into 2011 when the current reading rose and expectations were cut at the same time.

What we have now are relatively strong readings in both these components. The question is: which will break first? Will current conditions erode or will expectations falter? How much longer can both these gauges - each of which is better only about 25% of the time- continue to improve together? At some point further improvement in current conditions will outright erode expectations as it is realized that `things can't continue to improve like this.'

This month the current index already has taken a slight notch lower. Metrics on EMU as a whole have continued to improve, but just today the OECD has cut its outlook for OECD-area growth. How will Germany fare in this environment?

Germany is a special case in EMU; it generally has not been the fastest growing economy in the eurozone - by a long shot! But it has had the steadiest growth. It is the `strongest' economy in EMU and has been the best performing since the crisis hit. Here you should conjure images of the `tortoise and the hare' or of the Germany economy as a vehicle stuck in first gear: powerful, relentless, dependable. but slow.

Germany also has some issues it will have to deal with that could erode confidence and expectations. Already this month the evaluation of stocks by ZEW financial experts has been downgraded compared to last month. Bonds, while still given a negative rating, are improved from October and are at their best standing since July. In evaluating sectors, the German financial experts have downgraded just a bit more than they have upgraded on the month.

The four months of steady increases in ZEW expectations is a significant run for that index, but compared to previous episodes when the index has risen for four months in a row, this one has the weakest net gain over four months. The ZEW index is only an indicator. And given the problems in the eurozone and issues being confronted by Germany, including its currently too-large current account surplus, there should be some concern about where the economy goes from here. One of the issues that battered the eurozone in the crisis was that the countries were moving at different speeds.

Germany to some seems to be an economy of almost mystic strength if we evaluate its growth relative to the other original eurozone members. Germany's growth ranks as 11th out of 12 from the start of EMU up to the first quarter of 2007. Given the relatively better growth of Germany since the crisis, its ranking from the start of EMU now is 7th out of 12. Germany's growth has now surpassed France, the Netherlands, Portugal and Italy. Germany has grown much slower than most of the eurozone members. Because of that and its reliance on export-led growth, it has stayed more financially viable. The faster growing European counties were growing fast, maybe too fast, but they were also trying to develop, not just to maintain themselves.

Developmental issues and relative growth rates are big problems in the eurozone that need to be addressed. In the crisis Germany took control and tried to have austerity programs run in problem countries to bring those other economies in line with it. But who wants to grow in line with the 10th fastest EMU economy? Germany may be strong, but it is not fast. How EMU decides to bridge this growth gap, to address productivity differences among member countries and to deal with the deficit-surplus issues in trade as well as for fiscal issues, has huge ramifications for Germany. Germany may only now be on the cusp of realizing that the country too will have to make changes. The rest of the eurozone is not simply going to become Germany.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief