Global| Apr 25 2016

Global| Apr 25 2016Germany's Ifo Gauge Slips Amid Crosscurrents

Summary

The Ifo business climate index slipped to 106.6 in April from 106.7 in March but had been expected to rise. We plot the chart and offer a table of the diffusion version of the overall and sector indices which afford a look at Ifo [...]

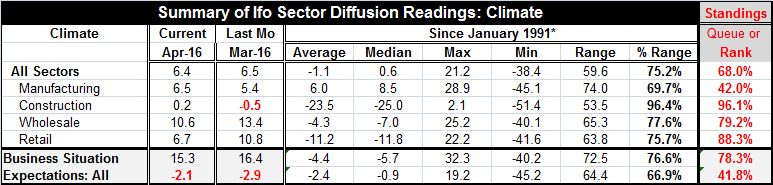

The Ifo business climate index slipped to 106.6 in April from 106.7 in March but had been expected to rise. We plot the chart and offer a table of the diffusion version of the overall and sector indices which afford a look at Ifo sectors up to date through April. Note that wholesaling and retailing fell hard in April while manufacturing and construction improved.

The Ifo business climate index slipped to 106.6 in April from 106.7 in March but had been expected to rise. We plot the chart and offer a table of the diffusion version of the overall and sector indices which afford a look at Ifo sectors up to date through April. Note that wholesaling and retailing fell hard in April while manufacturing and construction improved.

Overall, the Ifo sectors have been stepping backward steadily in recent months.

Sector issues and trends

The all-sector reading and its four principle components, manufacturing, construction, wholesaling and retailing show persistent declines in the levels of their respective diffusion readings over the last three months, six months and 12 months. The exceptions are that construction and retailing each are now stronger over 12 months and that construction is higher on balance over three months. But the overwhelming picture is of sectors lowering their standing over three months, six months and 12 months.

In addition, the sector standings have lost strength, but show relatively firm-to-strong readings. Construction remains as the strongest sector in relative terms with a queue standing that has been higher only about 4% of the time historically. Retailing has been higher about 12% of the time and wholesaling has been higher about 21% of the time. But manufacturing remains the black sheep of the sectors with a below-median standing at its 42nd percentile, dragging the all-sector index down to a moderate 68th percentile standing. Clearly, Germany shows a disappointing manufacturing sector with an economy being held aloft by its service sector readings and by construction.

Business situation and expectations

The overall business situation and expectations readings show a slightly different take on the German condition. While the business conditions index fell in April, expectations improved slightly, albeit posting a still negative reading. The standing metrics show expectations as below their median (below 50) with a queue standing at their 41st percentile while the business situation is still regarded as having a firm 78th percentile standing.

In terms of changes, the business situation index actually is on an improving path. While it is lower by 1.4 points over 12 months, it is higher by 0.9 points over six months and higher still by 1.3 points over three months. However expectations belie that improvement as expectations are lower by 5.4 points over 12 months and lower by even more - by 6.7 points- over six months and still net lower by 3.7 points over the most recent three months.

The paradox for Germany is that current situation seems to be improving while expectations continue to get scaled back. This is an ongoing paradox and dilemma. The insulated construction sector is one reason for this. Another seems to be the relative resiliency in retailing which has eroded by only 0.6 points over the last three months although it fell very sharply in April compared to March as wholesaling eroded alongside it.

Some issues for Germany

Europe has put a stop to the steady stream of migrants that was threatening to overwhelm it. A series of high profile attacks on German citizens by their new influx of migrants raised warning flags of problems to come and culminated in border EU countries shutting their borders to insulate Germany from further inflows. A deal between the EU and Turkey has migrants landing in Greece being shipped back or interdicted prior to landing in EU territory. Apart from migrants, there are still weak global conditions in manufacturing trade with the goods sector still out-producing the global demand for goods. Globally, while services sectors are doing better that than goods sectors, they also have been exhibiting erosion recently.

Stimulus of any sort has yet to make a clear mark. All the sense of progress from stimulus efforts comes from statistical studies that argue how much worse things would have been without stimulus of various sorts.

Still, the Ifo readings shows that only the manufacturing index is below its historic median (even it is above its average) while expectations are below their median and (slightly) above their average.

Germany shows evidence of dislocations in manufacturing but evidence that the rest of the economy is coping relatively well. The need to make arrangements for the settling of accepted migrants is even boosting the construction sector in Germany. However, most of the momentum in Germany is negative. The great exception is the business situation where we see evidence of progress still in train. That is a curious development to keep an eye on. Is Germany getting a grip on this weakness and it is ready to swing ahead or is its business sector improvement on borrowed time and will it, too, be overwhelmed by global weakness? Which should be focus on, the improving trend in German business conditions or the erosion in expectations?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief