Global| Dec 22 2014

Global| Dec 22 2014Germany Is Still Importing Deflation: How Long?

Summary

German import prices are holding relatively steady in negative territory, bringing a steady deflation impulse to the German economy. At the same time, German export prices have accelerated, rising at a 0.3% pace over 12 months to a [...]

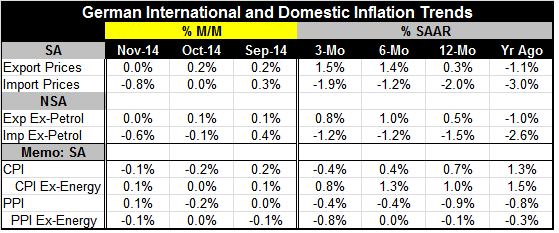

German import prices are holding relatively steady in negative territory, bringing a steady deflation impulse to the German economy. At the same time, German export prices have accelerated, rising at a 0.3% pace over 12 months to a 1.4% pace over six months and then ticking up to a 1.5% pace over three months. German exports are exhibiting some pricing power and are rising even faster than German domestic inflation, keeping exporting as a lucrative activity. The same trends hold excluding petroleum. With German export prices rising faster than import prices on a steady basis, Germany's terms of trade are improving. An improvement in a country's terms of trade raises its welfare since that country is getting more from what it sells than it is paying for what it buys. This is true as long as the country remains competitive with those faster-growing export prices.

German import prices are holding relatively steady in negative territory, bringing a steady deflation impulse to the German economy. At the same time, German export prices have accelerated, rising at a 0.3% pace over 12 months to a 1.4% pace over six months and then ticking up to a 1.5% pace over three months. German exports are exhibiting some pricing power and are rising even faster than German domestic inflation, keeping exporting as a lucrative activity. The same trends hold excluding petroleum. With German export prices rising faster than import prices on a steady basis, Germany's terms of trade are improving. An improvement in a country's terms of trade raises its welfare since that country is getting more from what it sells than it is paying for what it buys. This is true as long as the country remains competitive with those faster-growing export prices.

In this case, Germany's export prices (measured in euro terms) are rising as the euro falls. A cheaper euro improves German (and all EMU members') competitiveness. As the foreign currency cost of EMU members exports falls, it permits that member to raise its euro-based prices somewhat and to still achieve competitive inroads vs. foreign pricing as well as to increase profitability. However, a weak euro should raise import prices, too. And while German ex-petroleum import prices are still weaker than overall German import prices, they are still falling.

About one third of German exports and imports are to/from countries within the EMU region. That portion of German trade is unaffected directly by exchange rate movements.

On balance, Germany is prospering in this environment relative to most of its counterpart EMU members. Still, Germany has a special problem since it sends about 3.5% of its exports to Russia, a country that is under trade sanctions. Germany gets just less than 3% of its imports from Russia, most of that energy and, so far that, import flow has been maintained.

The German economy with its strong trade orientation and fiscal conservatism has been able to weather the storm that has engulfed Europe and the EMU. Still the Bundesbank has been cutting its outlook for growth. If it were to continue, the weak German (ex-energy) import price would pose a problem for German import-competing industries. But at some point, the falling euro should cause the opposite trend: import prices should start to rise as the euro falls and as imports become more expensive just as German exports become cheaper to their competitors' prices. And at that point, we would expect import prices to start providing an inflation impulse.

But German inflation is still low and inflation throughout the EMU is running at 0.3% year over year. For now, that weakness is reinforced by falling energy prices. The falling euro is occurring in a weak EMU economy. It is not impacting import prices as expected. But we expect the euro drop to continue for some time. The weak euro is having an impact on German exports and we see that in export prices as well as in the German trade surplus which, as large as it is, is sure to get bigger. But we don't see much impact on the import side because demand conditions and consumption are still so tempered in the EMU. So far, there is a pass-through asymmetry.

For now, Germany is still growing and doing better than the rest of Europe. We expect the falling euro to have some impact on German import prices and on European events, but possibly not until mid-2015. Meanwhile, Germany is opposed to the QE plan that most of the rest of the EMU wants, which is somewhat disingenuous since Germany is doing better than the rest of the EMU. I think we can be sure of three things. One is that the ECB will find a way to launch QE, given the widespread need. The second is that the Germans will find a way to keep the program small and largely ineffective. The third is that, that will keep the euro on its downward path throughout 2015.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief