Global| Oct 27 2014

Global| Oct 27 2014Germany Continues to Slip, Says Ifo Survey

Summary

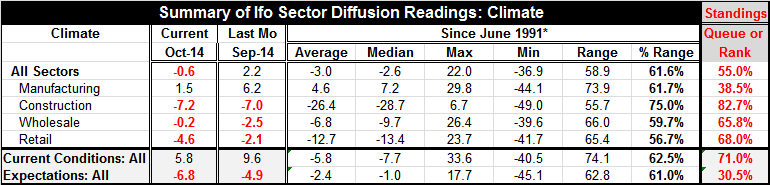

The Ifo climate index, the most closely watched of the German economic indicators, fell by 0.6 points in October. The index stands at the 55th percentile of its historic rank, meaning it's only five percentage points above its [...]

The Ifo climate index, the most closely watched of the German economic indicators, fell by 0.6 points in October. The index stands at the 55th percentile of its historic rank, meaning it's only five percentage points above its historic median which lies at 50.

The Ifo climate index, the most closely watched of the German economic indicators, fell by 0.6 points in October. The index stands at the 55th percentile of its historic rank, meaning it's only five percentage points above its historic median which lies at 50.

Each of the components except one fell in October. Manufacturing fell sharply from a level of 6.2 in September to just 1.5 in October. Manufacturing stands at the 38.5 percentile of its historic queue - an extremely weak reading. Construction, which is persistently negative, edged lower from its -7 reading in September to a -7.2 reading in October. Wholesaling alone saw improvement, moving up to -0.2 in October from -2.5 in September. Retailing took a large step back, declining from its -2.1 reading in September to -4.6 in October. The construction sector reading sits in the 82nd percentile of its historic queue; wholesaling is in the 65th percentile of its queue; and retailing is in the 68th percentile of its queue. The reading for construction, while the most deeply negative, is historically relatively firm at the 82.7 percentile. Despite its rebound, wholesaling is still quite moderate while retailing is also in the moderate space.

The current conditions index fell from 9.6 in September to 5.8 in October, sitting in the 71st percentile of its historic queue. Expectations fell from -4.9 in September to -6.8 in October, sitting in the 30th percentile of its historic queue.

By sector, manufacturing is worrisome and weak. By tenor, the current situation is fine but expectations have slipped to the 30.5 percentile of their historic queue. Those two developments are very worrisome. And there is no sector that is particularly strong.

The monthly change in the levels of the indicators was relatively severe for some of the components. Manufacturing was particular weak with its change (month-to-month) being worse only about 9% of the time historically. The retailing drop is only worse about 25% of the time historically. Business expectations index drops by more month-to-month only about 25% of the time historically. What we see are some relatively large monthly changes (drops) on indices that are already weak. This is not a good development.

On balance, the Ifo index made a weak showing in October, weaker than most expected. The report adds to other weak signals, ranging from the Markit flash indicators to the ZEW opinion index from the responses of its financial experts. The Ifo is more heavily favored by the market compared to ZEW because Ifo surveys the firms involved in the various sectors, not just financial experts.

While the weekend release of the ECB stress tests may not have been as bad as (some) expected -no major banks failed the test- there still were 25 laggards and that's after central banks have had all this time to apply their pressure. Since the ECB test was not stringent enough to fail any major European banks and since we know these banks generally still need to raise more capital, it raises questions about how tough the ECB test was and how it dealt with sovereign debt on bank balance sheets. While the ECB did manage to pass all the major banks in Europe, we have seen it do this before and still have found that banks failed. In short, this test has not reassured many market participants.

Markets continue to look at the weakening economic data. European stock markets have been ravaged by markets that have grown increasingly skeptical of European economic conditions. The ECB stress test does not go very far in mending those concerns and the German Ifo report heightens those concerns even more. Money supply and loan data, just reported today, also show a reason for concern: credit is dropping. Money supply growth has edged up, but the ECB program to encourage lending is not bearing any fruit at all. Despite the ECB's attempt to spur private lending and to mend perceptions of European banks, concerns continue to abound. The only upbeat message from today's reports came from U.K. retailers as the CBI survey showed upbeat news on expected retail sales. In Germany, the Ifo dropped and the German chamber of Commerce (DIHK) cut its outlook. The ECB stress tests could not trump all of that. The ECB is swimming against a strong current.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief