Global| Mar 11 2013

Global| Mar 11 2013German Trade Deteriorates: Is Growth Reviving?

Summary

German imports jumped more sharply than exports in January suppressing the German trade surplus. Still, the trend for that surplus is rising as export growth has been exceeding import growth for nearly one year. Import growth at 2.3% [...]

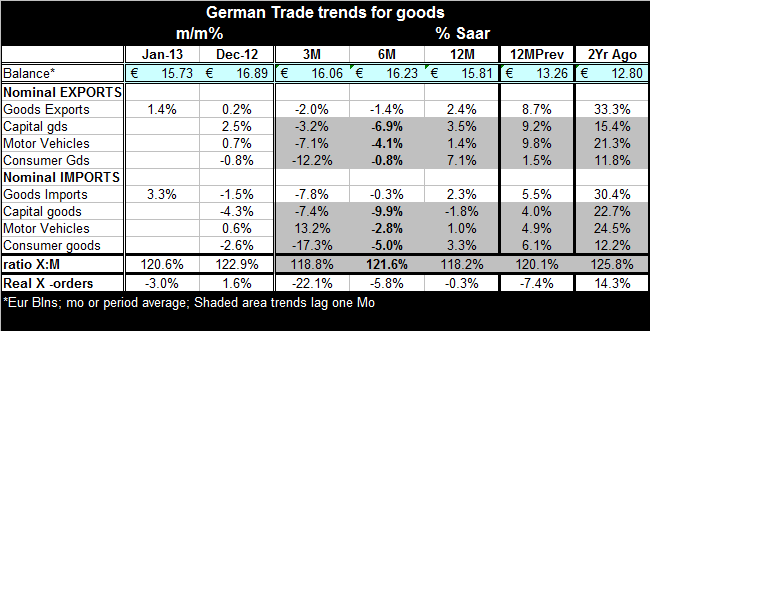

German imports jumped more sharply than exports in January suppressing the German trade surplus. Still, the trend for that surplus is rising as export growth has been exceeding import growth for nearly one year. Import growth at 2.3% yr/yr is just behind and on-the-heels of exports at 2.4% in yr/yr terms. This is the strongest import growth in three-months and the second strongest in eight months. Yet it begs the question of whether the German economy is beginning to improve or not.

German imports jumped more sharply than exports in January suppressing the German trade surplus. Still, the trend for that surplus is rising as export growth has been exceeding import growth for nearly one year. Import growth at 2.3% yr/yr is just behind and on-the-heels of exports at 2.4% in yr/yr terms. This is the strongest import growth in three-months and the second strongest in eight months. Yet it begs the question of whether the German economy is beginning to improve or not.

Rising imports are usually a sign of a reviving economy. But imports also are volatile. These monthly numbers are not definitive. The import signal actually takes on greater validity over longer periods or through a signal that is a sharp move.

Import performance does not go over any of these more stringent hurdles for Germany. Imports have risen more than exports month-to-month (2.2% Vs 1.4%) but that is thin ice indeed. Over three-months imports are falling at a 7.8% annual rate compared to exports falling at a 2% pace. There is simply is not enough push in imports to take them as a signal of German economic revival. Moreover, German manufacturing orders are still falling and the domestic component of orders is weaker than the foreign component.

Germany is an export-orient economy. Right now exports are not showing much leadership for the economy as a whole. Industrial production is weak and orders are weaker.

While Germany has showed some signs of revival, most notably in the performance of the PMI signals for MFG and Services, traditional economic variables continue to show Germany still stuck in the morass of downturn. Imports have not yet turned the corner sharply enough of clearly enough to represent an upbeat assessment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief