Global| May 09 2017

Global| May 09 2017German Surplus Erodes As Exports Fade

Summary

German trade data features the headline balance which shows the surplus having diminished in March and export and import data that show a bit of an import surged juxtaposed to an export weakening. The commodity detail lags by one [...]

German trade data features the headline balance which shows the surplus having diminished in March and export and import data that show a bit of an import surged juxtaposed to an export weakening. The commodity detail lags by one month so growth rates for the component trends are expressed on a lagged basis to permit trend calculations.

German trade data features the headline balance which shows the surplus having diminished in March and export and import data that show a bit of an import surged juxtaposed to an export weakening. The commodity detail lags by one month so growth rates for the component trends are expressed on a lagged basis to permit trend calculations.

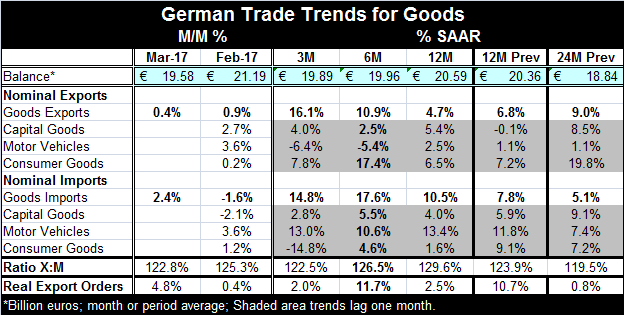

We can isolate two different sorts of trends in the table above. There are the sequential annual trends for trade on yearly growth from 24 months ago, 12 months ago and now. There are also the growth rates inside one year for three-month, six-month and 12-month.

Annual trends

The annual growth rates show exports are still slowing; the annual-periods show growth rates falling from 9% to 6.8% to 4.7% in the most recent year period. Imports, under the influence of now of rising oil prices, have accelerating annual trends. Nominal import growth rises from 5.1% to 7.8% to 10.5% in the most recent 12 months.

Overall trends within the last year

However, within the last year, exports are accelerating from 12-month to six-month to three-month as growth accelerates from 4.7% to 10.9% to 16.1%. On the same timeline, imports are more or less without trend but have double-digit growth rates on each horizon.

Export details

Export commodity categories show mixed trends. Across annual data motor vehicle exports are improving, but within the year the trend is shrinking and culminating in contraction. Consumer goods exports are decelerating over the annual periods with unclear trends within the year. No other trends prevalent.

Import details

Import categories show acceleration over the annual data for motor vehicles and deceleration for capital goods. Within one year all trends are mixed.

Broader trends

The ratio of exports to imports is still high although it has backed off in March as imports surged while exports only nudged higher. Real export orders provide an upbeat message, rising by 4.8% in March although the trend for real export orders under one year is convoluted as is the multi-year trend. The German trade surplus is still large but has declined from its largest position largely thanks to rising oil imports as prices have risen. Neither exports nor imports show any particular underpinning in their component trends even though import annual trends are rising and export trends inside one year are accelerating after their annual trends had pointed lower. All in all, trade still appears to be in engaged in a sort of tug-of-war transition state, even though we can conclude that exports and imports both have 'generally accelerated' and that the overall trade deficit has withered; there are not solid fundamentals to support that continuing. The import trends are largely driven by oil and oil prices while the export trends have cooled then heated up without clear support across the export components. All of this makes the outlook still a bit of a mystery.

The outlook

Globally the IMF has barely lifted its outlook for Pacific regional growth. The Bank of France is looking for French growth to step up to 0.5% in Q2 while the Austrian central bank has upgraded its outlook for Q2 to 0.6% growth. There are now more widespread upward revisions in play than downward revisions, but the changes in the outlook remain small. The underpinnings of strength are still elusive. And while markets dodged a bullet on the French elections, there is still restlessness in Europe that has not gone away. Europe has to deal with that reality and at the same time punish the U.K.'s giving into those same forces in order to squelch the restive movements within the EMU. Of course, EMU members do not present their case that way, but there is hardly any other way to understand the hard line they are taking on the U.K. over Brexit that will harm them as much as it will harm the U.K. I guess in the end breaking up really is hard to do.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief