Global| Dec 01 2008

Global| Dec 01 2008German Retail Sales Hit the Skids Again in October

Summary

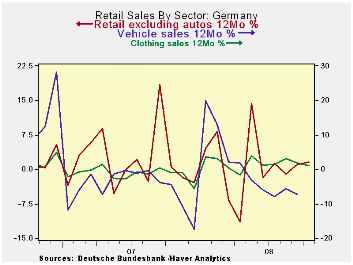

No hunt for this red October… German retail sales were unexpectedly weak in October. The ‘unexpectedly’ part is just as important as the ’weak’ part since Germans have been deluding themselves with a view of how this crisis is going [...]

No hunt for this red October…

German retail sales were unexpectedly weak in October. The

‘unexpectedly’ part is just as important as the ’weak’ part since

Germans have been deluding themselves with a view of how this crisis is

going to pass them by. Chancellor Merkel is disdainful of what she

regards as competition over who can launch the largest stimulus plan

and has in contrast to much of the rest of the world continued to sit

on the sidelines and watch as Germany’s economy unravels. Retail sales

in Germany are steadily and progressively deteriorating. Real ex auto

sales are down at a 3.9% annual pace over three months compared to a

-2.2% pace over six months and -1.4% over 12-months. What is the

surprise there? Why should that sequence of growth rates, that is so

very well-behaved, be called ‘unexpected?’ Sales had risen by a strong

2.1% in August and after a rise of 0.3% in July. But September and

October sales now tell a different story and one that is consistent

with the world surrounding the German economy as well. The progression

of growth rates shows the August ‘burst of strength’ to have been a

false signal. Real and nominal series tell pretty clear stories if

anyone is watching. Now Germany’s auto sector is getting hit harder as

short hours are being planned.

| German Real and Nominal Retail Sales | ||||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Oct-08 | Sep-08 | Aug-08 | 3-mo | 6-mo | 12-mo | Yr Ago | QTR Saar |

| Retaill excl Auto | -1.7% | -1.1% | 2.1% | -3.0% | -0.2% | 1.1% | -1.0% | -10.1% |

| Food Beverage & Tobacco | -0.4% | -1.7% | 3.4% | 5.0% | 0.4% | 0.0% | 2.6% | -2.6% |

| Clothing & Footwear | -4.4% | 4.1% | -0.1% | -2.5% | 9.3% | 1.6% | 0.5% | -10.9% |

| Real | ||||||||

| Retail excl Auto | -1.6% | -1.0% | 1.6% | -3.9% | -2.2% | -1.4% | -2.4% | -9.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.