Global| Aug 18 2017

Global| Aug 18 2017German PPI Inflation Downshifts

Summary

In the short term, much of what happens to PPI inflation is determined by oil prices as the chart (on the left) reminds us. However, the mapping is not one-to-one and is not without its lags. Still, it is clear that recent hiatus in [...]

In the short term, much of what happens to PPI inflation is determined by oil prices as the chart (on the left) reminds us. However, the mapping is not one-to-one and is not without its lags. Still, it is clear that recent hiatus in PPI inflation in Germany has a lot to do with oil prices going weak again.

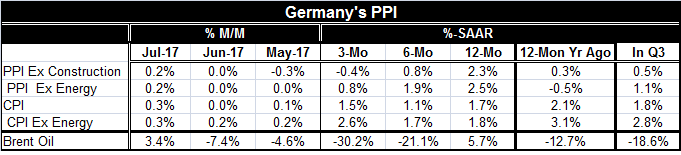

The German PPI rose by 0.2% in July after being flat in June. It is decelerating form 12-month to six-month to three-month as the chart (on the right) and table (below) demonstrate. The PPI excluding energy also is on a steady deceleration course with a 12-month PPI gain at 2.5% and a three-month annualized gain less than 1%.

In the just stated quarter-to-date (Q3 2017), the PPI is rising at a 0.5% annual rate with the ex-energy PPI rising at a 1.1% annual rate. Oil prices are falling at a better than 18% annual rate in early Q3. OPEC still appears unwilling and unable to get control of oil prices as fracking activity in the U.S. keeps making the job of controlling oil prices harder by increasing its capacity.

Inflation continues to be kept under wraps. For Germany, its CPI shows a bit more inflation with a headline cruising at or around a 1.5% pace and an ex-energy pace that is closer to 2% and early in Q3 rising at a 2.8% annual rate.

Germany has been more touchy about inflation than the rest of the EMU partly because of its inbred ideology and partly because the German economy simply has performed much better than the rest of Europe and it is closer to creating classical Keynesian bottleneck inflation (if economies do that anymore) than any other economy in Europe. Its unemployment rate is at a post-reunification low.

Mario Draghi, head of the ECB, will be participating in the Federal Reserve's Jackson Hole Symposium this year but will not be dropping any nuggets about monetary policy in the EMU. The ECB is still keeping its policy unchanged, but it may be on the verge of peeling back some of the more expansive elements of its policy such as ongoing securities purchases.

For the moment, inflation is not knocking at the door of the ECB nor is it at the door of the BOJ or the Federal Reserve, The Bank of England found some inflation pressure as the pound sterling fell sharply. But now that the pound has stopped falling inflation pressure has been easing there. Inflation is simply hard to conjure in this new world of excess supply and with so many developing countries bent on extending development further and therefore continually bringing new low-paid workers into the mix.

There are some signs that growth is getting firmer and looks less fragile in both in the U.S. and in Europe. But we have seen these signs come and go before in this cycle. Still, central bankers seem emboldened to take the next step in their respective processes. Markets are braced for that to happen and are currently handicapping prospects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief