Global| Feb 19 2016

Global| Feb 19 2016German PPI Inflation Continues to Sink

Summary

Germany's PPI (excluding construction) fell by 0.8% in January. It fell by 1.1% in manufacturing and by 0.2% in manufacturing excluding energy. Overall manufacturing and ex-energy manufacturing inflation all are falling over three [...]

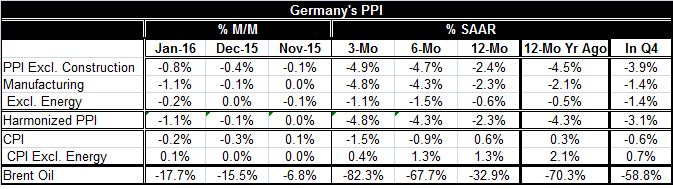

Germany's PPI (excluding construction) fell by 0.8% in January. It fell by 1.1% in manufacturing and by 0.2% in manufacturing excluding energy. Overall manufacturing and ex-energy manufacturing inflation all are falling over three months, over six months and over 12 months. This is a striking development underscoring how much negative inflation trends still are in play.

Germany's PPI (excluding construction) fell by 0.8% in January. It fell by 1.1% in manufacturing and by 0.2% in manufacturing excluding energy. Overall manufacturing and ex-energy manufacturing inflation all are falling over three months, over six months and over 12 months. This is a striking development underscoring how much negative inflation trends still are in play.

Except for manufacturing excluding energy, sequential inflation rates are falling at increasingly faster rates. For manufacturing ex-energy, that sequence is not fully in place, but inflation there is still lower over three months than over 12 months (prices are falling faster).

Moving on to the more closely-watched CPI trends, we see the same sorts of trends in place although prices are not falling on all horizons. But CPI, HICP and energy inflation trends in Germany all are falling. The trend for Brent continues to show accelerating price declines which should pass on to other price trends. Thus, our best view of the data is that price trends are lower and will continue to have downward pressures for some time to come. Yet, the ECB remains well behind the curve on hitting its inflation target as it has for some time.

Germany, one of the most consistent and strong economies in Europe, is not seeing any forestalling of deflation pressures because of its growth or low unemployment rate. Instead, Germany seems to have the same deflation issues as the rest of the euro area.

Germany for most of EMU history has long had the lowest inflation rate in the EMU but not anymore. Still, German inflation was close to the EMU just under 2% target last in April 2012 on the PPI. But since April 2014, the German PPI has been consistently falling. Germany's CPI headline has been below a 1% year-on-year pace since May 2014. It was just below 2% last in July 2013.

Germany's economy continues to show a persistent tendency to create inflation that is too low. Since energy declines are ongoing, there will be more of that weakness to come. Of course, ECB policy will be made on EMU-wide trends, but those trends also continue to show rampant inflation undershooting. Germany is simply not an exception to the needs of the region as it has often been in the past.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief