Global| Jan 14 2010

Global| Jan 14 2010German Posts Lowest Annual Inflation Rate In 20-Years

Summary

German inflation, while beginning to edge up at year-end in its HICP and CPI formats has registered the lowest annual pace in 20-years. The small two-line panel at the table top shows overall statistics for the German CPI (as opposed [...]

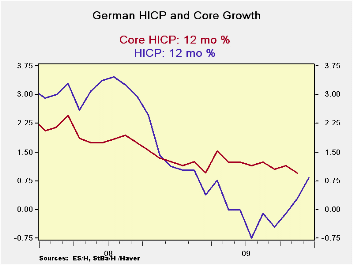

German inflation, while beginning to edge up at year-end in its HICP and CPI formats has registered the lowest annual pace in 20-years. The small two-line panel at the table top shows overall statistics for the German CPI (as opposed to the harmonized HICP treatment) where the core measure is available for December (the core reading is not yet available for the HICP format). In terms of the Germany’s CPI while the headline rate rose at year end, the core rate’s 3-month pace was still declining.

Diffusion measures the breadth of inflation’s acceleration regardless of the pace across categories. Calculated on the various 3-mo 6-mo and 12-mo periods, inflation rates of the HICP across categories reveal that inflation is not accelerating. The diffusion reading of 45.5% over three months is below the neutral mark of 50%.. That statistic means, roughly, that inflation is only accelerating in 45.5% of the categories over three months (compared to six months) and that it is decelerating in 54.5% of the categories. Thus even with the bump up in overall inflation, diffusion tells us that inflation forces are not widespread. And, of course, inflation is low to boot.

While the Bundesbank and the ECB are headline inflation-watchers it must be some solace to them that the Core rate remains so subdued and so steady. In the last cycle the core rate proved to be a very good signal about inflation and how entrenched it had become. Headline inflation failed as an inflation siren as it howled too shrilly in the recession as oil and other commodity prices soared. But the core rate remained pretty low and stable even as the headline soared. The Fed, which takes its cue more from the core rate (it does not target inflation however) had the flexibility to cut rates when it chose. The ECB, in contrast, needed to cut rates as part of international deal on the ‘expectation’ that inflation would recede. Of course, it did recede, but central banks do not like to be cutting rates with inflation over their stated targets.

Nonetheless it is a good end to 2009 on the inflation side. The bump up in headline inflation at year- end is oil- related and it appears to have exerted no pull on core prices. These developments leave us in good stead to take a fresh a look at 2010. So far 2010 is looking like a year in which growth will be a hotter topic than inflation.

| German HICP | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Dec-09 | Nov-09 | Oct-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.3% | 0.1% | 0.2% | 2.3% | 0.9% | 0.8% | 1.1% |

| Core | #N/A | -0.2% | 0.1% | #N/A | #N/A | #N/A | 1.3% |

| CPI | |||||||

| All | 0.2% | 0.1% | 0.2% | 1.9% | 0.7% | 0.8% | 1.1% |

| CPIxF&E | 0.2% | -0.1% | 0.0% | 0.4% | 1.1% | 1.0% | 1.3% |

| Food | -0.2% | 0.5% | -0.1% | 0.7% | -2.3% | -2.0% | 1.9% |

| Alcohol | -0.3% | -0.5% | 0.0% | -2.9% | -2.0% | -0.9% | 0.7% |

| Clothing & Shoes | 2.3% | -1.4% | 0.2% | 3.9% | 3.9% | 2.5% | 0.7% |

| Rent &Util | 0.0% | 0.2% | -0.1% | 0.4% | -0.2% | -0.2% | 2.5% |

| Health Care | 0.1% | 0.1% | 0.0% | 0.8% | 0.8% | 0.8% | 1.8% |

| Transport | -0.3% | 2.1% | 0.0% | 7.5% | 5.6% | 4.1% | -2.8% |

| Communication | 0.0% | -0.4% | 0.1% | -1.3% | -0.9% | -1.8% | -3.3% |

| Rec &Culture | -0.1% | -0.4% | 0.2% | -1.2% | 0.2% | 0.5% | 1.2% |

| Education | 0.7% | 1.5% | 0.2% | 9.8% | 5.9% | -1.1% | -3.8% |

| Restaurant & Hotel | 0.7% | -0.4% | 0.5% | 3.4% | 2.4% | 1.9% | 2.6% |

| Other | 0.4% | -0.4% | 0.7% | 3.0% | 3.0% | 2.1% | 1.7% |

| Diffusion | -- | -- | -- | 45.5% | 54.5% | 45.5% | -- |

| Type: | Diffusion: Current Compared to | 6-mo | 12-mo | Yr-Ago | |||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief