Global| Aug 06 2020

Global| Aug 06 2020German Orders Surge in June

Summary

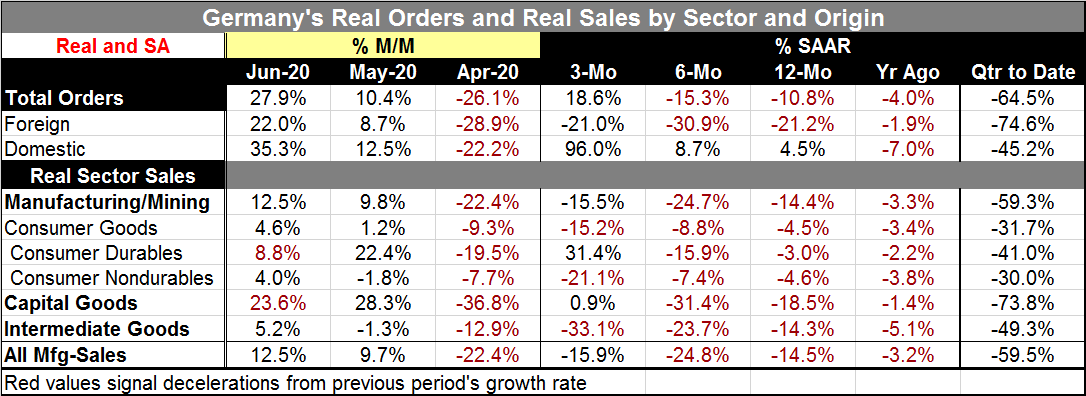

German orders made a spectacular comeback in June, rising by 27.9% on the back of a 10.4% gain in May. Orders had fallen in February (-1.2%), March (-15.0%) and April (-26.1%) as the coronavirus began to dog Europe. Sequential order [...]

German orders made a spectacular comeback in June, rising by 27.9% on the back of a 10.4% gain in May. Orders had fallen in February (-1.2%), March (-15.0%) and April (-26.1%) as the coronavirus began to dog Europe.

Sequential order growth now has some momentum. For domestic orders, order growth rates rise from 4.5% over 12 months to 8.7% over six months to 96.0% over three months (at a compounded annual rate on real flows). However, foreign orders are not so clear cut as they still fall by -21.1% over 12 months and at a -30.9% pace over six months and at a -21.0% pace over three months. Total orders show a mixed pattern but do return a large positive annualized growth rate of 18.6% over three months.

Assessing Order Growth

I present two charts below to track and understand German orders because the growth rates are so wild it is hard to get a sense of what is going on with orders on a net basis. Chart 1 graphs year-over-year percentage changes in orders. There the drop and rebound in orders is clear. Domestic orders have been weak for some time going back to well before the arrival of the virus. Domestic orders are higher year-over-year in June for the first time since July 2018. Domestic orders have in a very short time shrugged off 'all the weakness' from the coronavirus. Not so foreign orders that are still falling by 21.1% over 12 months. However, that series last showed positive growth in February of this year.

Order Levels

Chart 2 on the level of orders shows the increase in domestic orders for what it is: an easy comparison. While domestic orders have grown more than foreign orders (that fell over 12 months in June), the 12-month ago comparison for domestic orders is easy because German domestic orders began falling, erratically at first back in December 2017 before they continued on their unbroken monthly weakening streak that has just ended this month. Domestic orders were at this peak strength in this cycle in mid-2017 as part of a sideways oscillating pattern while foreign orders peaked in December 2017 after rising strongly and reaching a sharply higher peak value. Even so, the rebound in domestic orders in Germany is impressive.

Real Sales

Real manufacturing shipments show some life as well as they jumped by 12.5% month-to-month in June. However, shipments still bear negative growth rates over 12 month, six months and three months. All three sectors saw manufacturing sales advance in June: consumer goods, capital goods and intermediate goods.

Quarter-to-Date

Quarter-to-date data are now for the completed Q2 period. These growth calculations apply to order and shipment averages in Q2 compared to Q1 still show massive weak and declining rates of growth. However, on the doorstep to Q3, we find there is some very strong momentum as the second quarter ends. I call the assessment of this growth stepped-up inherited growth. Formally it is the level of a series (say orders) in the last month of the quarter (here, June) taken as a ratio to the current quarterly average (here Q2) and positioned as a growth rate; here that means compounded by the 12th power (since June is one month from the middle of the quarter). The compounding exaggerates the signal, but it does convert the percentage change to a growth rate. Viewed this way, the growth at the end of Q2 in orders is massive on the order of 800-plus percent. If we assume this level of orders only holds in July and recalculate the gain using a sixth power to compound the growth (as if it is over a two-month instead of one-month period), it drops to a still colossal 206%. The point is that the recovery of growth in May and the surge in June leave orders in a very good position at the end of Q2 heading into Q3 where strong growth is being signaled by the orders data; that would be true even with some give back in July.

Summing Up

I feel a bit guilty relying on numbers since we know that this is a sort of rock-paper-scissors game. However, rock-solid our data seem, the real world of the virus can paper it over and wrap it up, stopping it in its tracks. So momentum is nice, but it is not to be relied upon. And Germany is having a virus setback as is much of Europe… and German orders are largely exposed to Europe. On balance, we have to admit that as rollicking as the German numbers look, they are still not to be trusted. They may hang on as strong or not. It is hard to tell. Clearly, there is risk to growth, but there is also momentum.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief