Global| May 08 2017

Global| May 08 2017German Orders Rise on the Back of Foreign Order Strength

Summary

German orders rose by 1% in March on the back of a strong gain in foreign orders. Foreign orders advanced by 4.8% on the month, their strongest gain since March of last year. Foreign orders broke a seesaw pattern of orders in March, [...]

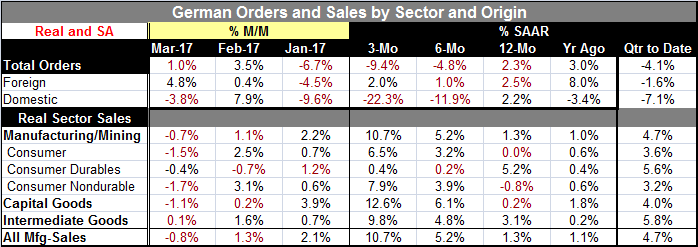

German orders rose by 1% in March on the back of a strong gain in foreign orders. Foreign orders advanced by 4.8% on the month, their strongest gain since March of last year. Foreign orders broke a seesaw pattern of orders in March, an alternatively rising and falling pattern that had been in pace over the last five months, as the March strong order gain came on the heels of a soft rise in February. Domestic orders have been alternatively up and down since April of last year. Domestic orders fell by 3.8% in March but in the wake of a 7.9% rise in February which was in part a reaction to a 9.6% fall the month before that, and so on. This has been the most volatile string of four months for domestic orders since the four months ended August 2011. And it is the second most volatile episode on data back to 1996. Only the 2011 episode is even comparable to this sort of volatility. The volatility experienced over the past four months ranks in the top 2% for domestic orders and in the top 30% for foreign orders.

German orders rose by 1% in March on the back of a strong gain in foreign orders. Foreign orders advanced by 4.8% on the month, their strongest gain since March of last year. Foreign orders broke a seesaw pattern of orders in March, an alternatively rising and falling pattern that had been in pace over the last five months, as the March strong order gain came on the heels of a soft rise in February. Domestic orders have been alternatively up and down since April of last year. Domestic orders fell by 3.8% in March but in the wake of a 7.9% rise in February which was in part a reaction to a 9.6% fall the month before that, and so on. This has been the most volatile string of four months for domestic orders since the four months ended August 2011. And it is the second most volatile episode on data back to 1996. Only the 2011 episode is even comparable to this sort of volatility. The volatility experienced over the past four months ranks in the top 2% for domestic orders and in the top 30% for foreign orders.

Such volatility makes the calculation of growth rates less meaningful, especially when the pattern is so strongly up and down in adjacent months. As things stand, overall and domestic orders show a pattern of sequentially decelerating orders growth culminating in contraction over both three months and six months. In contrast, foreign order growth patterns do not have a clear trend over three months, six-months and 12 months but do show growth on all those frequencies in the tight range of 1% to 2.5% on an annualized basis.

In the quarter-to-date, all order measures are weak and declining. Total orders, foreign orders and domestic orders all are declining with domestic orders down at an annualized pace of 7.1% and foreign orders dropping at an annualized pace of 1.6%.

Sales show a much steadier profile. For all of manufacturing, sales are accelerating from a 12-month growth rate of 1.3% to a six-month pace of 5.2% to a three-month pace of 10.7%. All three major sectors, consumer goods, capital goods and intermediate goods, show the same patterns of steadily accelerating sales. Inside of one year, there is a very different pattern for sales than for orders.

In the quarter-to-date, sales are expanding at a pace of 4.7% with real sector sales rates only varying on a range of 3.6% for consumer goods to 5.8% for intermediate goods. As volatile as orders have been, sales have been just about that stable as an offset.

Real orders, however, do have a strong correlation to real sales and that relationship is strong between 12-month growth rates where real orders have been much more stable. Real orders lead sales by two to three months and explain about 86% of the variance in real sales on year-over-year changes. While there is a great deal of monthly volatility, the year-on-year results continue to show solid order growth with the current 12-month pace at a positive 2.3% and are already expressed in real terms. On balance, there is a lot of volatility in German orders. But the year-on-year trends that have the most meaning continue to be stable and to point to continued growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief