Global| Jun 07 2017

Global| Jun 07 2017German Orders Log Sharp Fall in April; Still Hold Momentum

Summary

German real orders fell by a sharp 2.1% in April, but after rising by 1.1% in March and by 3.5% in February. The monthly declines have rolled off German momentum like water off a duck's back. German total orders are still accelerating [...]

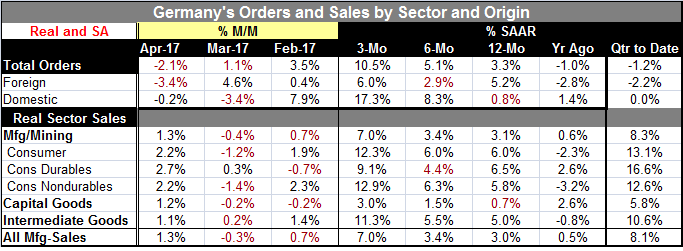

German real orders fell by a sharp 2.1% in April, but after rising by 1.1% in March and by 3.5% in February. The monthly declines have rolled off German momentum like water off a duck's back. German total orders are still accelerating on a timeline from 12 months, from a pace of 3.3%, to 5.1% over six months and 10.5% over three months (all annualized).

German real orders fell by a sharp 2.1% in April, but after rising by 1.1% in March and by 3.5% in February. The monthly declines have rolled off German momentum like water off a duck's back. German total orders are still accelerating on a timeline from 12 months, from a pace of 3.3%, to 5.1% over six months and 10.5% over three months (all annualized).

Foreign orders

German foreign order trends prevaricate a bit with 12-month growth at 5.2%, slipping to 2.9% over six months then surging back to gain at a 6% pace over three months.

Domestic orders

German domestic orders are simply explosive, rising modestly by 0.8% over 12 months, then stepping up at an 8.3% pace over six months and to an incendiary 17.3% pace over three months. The domestic trend is riding a 7.9% month-to-month gain logged in February.

German orders in Q2

On a quarter-to-date basis, German real order trends are not so strong. Total orders are falling at a 1.2% pace on the first month in the new quarter while foreign orders are dropping at a 2.2% pace and domestic orders are flat. The quarter-to-date framework puts some of the strength in recent order growth in Q1, raising the hurdle for the calculation of Q2 growth rates from that elevated Q1 base.

Germany and the rest of EMU

New orders from fellow EMU members fell by 1.4% in the recent month, just another reminder that German growth preys on demand in the rest of the euro area. There are also Markit and EU Commission gauges for Germany and the rest of the EMU. The Markit PMI gauge for German manufacturing showed the slightest step back in the German sector gauge for April and a strong rise in May to its highest level in over five years. The EMU gauge for April shows the German industrial sector stronger in April and level at that high mark in May with the Germany gauge in the top 11% of its queue of values back to May 1996. The overall EMU industrial gauge actually improved in April although France and Spain still sputtered with negative readings. On balance, while German orders show weakness in orders sourced to the rest of the EMU, the EU Commission overall and country-level gauges still show high industrial sector standings in the rest of the EMU and ongoing improvement through May for the EMU as well as for each of the Big-Four EMU economies.

Real sector sales in Germany

While German real order trends seem somewhat scatter shot even if mostly strong, the real sector sales trends in Germany remain quite solid. Total sales rise by 3.1% over 12 months, edging up to a 3.4% pace over six months and to a 7% pace over three months. Consumer goods sales have ramped up from a strong 6% pace over six months and 12 months to expand at a 12.3% pace over three months. While there are balanced sales and mostly acceleration in both durable and nondurable goods, real sector sales oddly are led by strength in nondurables at least over three months when the pace of growth at 12.9% exceeds durables at 9.1%. Still, year-on-year durables at a 6.5% pace are slightly faster than nondurables at a still robust 5.8%. Both German capital goods and intermediate goods show sequential growth rates expanding at a quickening pace. For capital goods, the growth rates crescendo over three months at a 3.0% pace; for intermediate goods, they top out at an 11.3% pace over three months.

Sales run solid and strong in the new quarter

Unlike orders, real sector sales growth rates also are solid in the quarter-to-date, rising at an 8.3% pace overall with true strength in all categories led by consumer goods especially consumer durables. German data may show some volatility. Orders are particularly susceptible to that. But German sales portray much more solid and consistent momentum for the German industrial sector.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief