Global| Dec 06 2016

Global| Dec 06 2016German Orders Leap Ahead

Summary

German orders surged in October, rising on a broad front. Both foreign and domestic orders jumped. Overall orders rose by 4.9% in October led by a 6.3% surge in domestic orders supported by a 3.9% gain in foreign orders. Order trend [...]

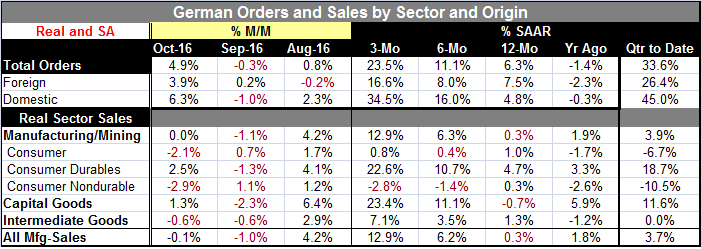

German orders surged in October, rising on a broad front. Both foreign and domestic orders jumped. Overall orders rose by 4.9% in October led by a 6.3% surge in domestic orders supported by a 3.9% gain in foreign orders.

German orders surged in October, rising on a broad front. Both foreign and domestic orders jumped. Overall orders rose by 4.9% in October led by a 6.3% surge in domestic orders supported by a 3.9% gain in foreign orders.

Order trend is higher

In the wake of this order largesse, orders are now rising and accelerating on all horizons. Domestic orders show the strongest acceleration pattern followed by foreign orders. Year-on-year, however, orders are up by 6.3% led by a 7.5% gain in foreign orders and followed by a 4.8% gain in domestic orders. In the previous year to that, both foreign and domestic orders had declined.

Quarter-to-date

Since this is the first month of a new quarter, the quarter-to-date calculations are eye popping for overall orders as well for domestic and foreign components.

Orders by broad geography

Orders within the euro area were flat on the month while orders from destinations outside the euro area surged by 6.7%. Capital goods orders to destinations outside the euro area rose by 9.2% while capital goods orders within the euro area advanced by 3.1%. Consumer goods outside the euro area saw orders increase by 3.3% in the month. Within the euro area, consumer goods orders fell by 4%. Consumer durable goods orders surged both inside and outside the euro area while consumer nondurable goods orders contracted to both destinations.

Real sector sales trends show life

Real sector sales did not show any special strength in October and in fact came in flat. For all of manufacturing sales fell by 0.1%. But real sector sales as well as manufactures sales are on strong accelerating trends. For manufacturing sales are up by 0.3% over 12 months, at a 6.3% annual rate over six months and at a 12.9% annual rate over three months. Consumer goods sales are solid, underpinned by consumer durable goods sales that are accelerating and strong. Consumer nondurable goods sales are the opposite, weak, falling and decelerating. But capital goods sales are strong and accelerating sharply especially over three months. Intermediate goods sales also show a firm and accelerating profile of gains. The pick-up in sales is news that adds to the validity of October's orders rise.

Summing up

As things stand, the German orders seem to be fully back and strong. The strength, however, is largely outside the euro area and as yet it is not clear what the source of the strength may be. China, Japan and most of Asia are still struggling. It is never a good idea to make these calculations in the month of an orders surge and think that the trend has been properly captured. Orders tend to be volatile and momentum tends to ebb and flow. For now there is a good deal of reassurance about the path of German orders, but there can be no certainty about whether the pop in orders will stay or how much of it might erode in the coming months. To be sure it is good news, but it is also news of unknown quality at this point.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief