Global| Apr 07 2010

Global| Apr 07 2010German Orders Hold Gains

Summary

German orders were flat in February as they held the 5.1% m/m gain from the month before. Foreign orders built on a 3.7% gain in January by rising an additional 1.8% m/m as domestic orders gave back 1.9 percentage points of their 6.7 [...]

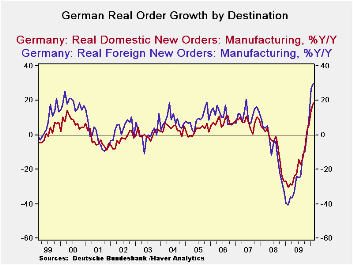

German orders were flat in February as they held the 5.1% m/m gain from the month before. Foreign orders built on a 3.7% gain in January by rising an additional 1.8% m/m as domestic orders gave back 1.9 percentage points of their 6.7 percentage point spurt in January. Over three months foreign orders are rising at an 11.8% pace while domestic orders are right behind at a 9.7% pace. Overall orders are up by 24.5% Yr/Yr, they are lower over six months, but are back strong on the three-month horizon.

In the quarter to date German orders are showing a strong lift rising at a 24.1% annual rate, with nearly identical foreign and domestic order rates of growth. Sales of consumer durables and capital goods are advancing the fastest in Germany in the quarter.

The orders news in Germany for February is good buffer to the revised Q4 e-Zone GDP growth rate which has been cut to show zero growth. But, looking ahead, the OECD now expects G-7 growth to slow although growth in the US is expected to lead the pack. Europe is having a hard time getting growth lined up. Its broader social safety net put a quicker bottom on the decline in GDP in the Zone during the downturn, but the enlarged public sector deficits and fiscal problems throughout the e-Zone put any further fiscal help off limits. Europe’s more stifled job market means that private sector jobs will not comeback quickly leaving its hope for stronger growth in the hands of the export sector.

German orders data are encouraging from that standpoint. Germany seems to making its export-led progress and the domestic sector appears to be in tow. The Service sector is coming along in Europe as well. That is important because that will be the sector of job creation that will sustain recovery.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | QTR to Date |

|||||

| Feb-10 | Jan-10 | Dec-09 | 3-MO | 6-Mo | 12-Mo | YrAgo | ||

| Total Orders | 0.0% | 5.1% | -2.4% | 10.5% | 5.1% | 24.5% | -36.2% | 24.1% |

| Foreign | 1.8% | 3.7% | -2.5% | 11.8% | 5.7% | 30.1% | -40.7% | 23.5% |

| Domestic | -1.9% | 6.7% | -2.1% | 9.7% | 4.8% | 18.7% | -30.6% | 24.9% |

| Real Sector Sales | ||||||||

| MFG/Mining | -0.1% | 1.3% | -1.1% | 0.4% | 0.2% | 8.2% | -24.1% | 3.0% |

| Consumer | -2.0% | -4.0% | 2.2% | -14.6% | -7.6% | -1.5% | -11.7% | -12.8% |

| Cons Durables | -2.5% | 4.1% | -2.1% | -2.6% | -1.3% | 5.3% | -22.2% | 10.8% |

| Cons Non-Durable | -2.0% | -5.0% | 2.8% | -16.3% | -8.5% | -2.4% | -9.8% | -15.6% |

| Captial Gds | 1.0% | 2.6% | -1.3% | 9.4% | 4.6% | 10.9% | -29.9% | 11.9% |

| Intermediate Gds | -0.1% | 2.6% | -2.8% | -1.2% | -0.6% | 12.3% | -24.3% | 2.7% |

| All MFG-Sales | 0.0% | 1.2% | -1.1% | 0.4% | 0.2% | 8.4% | -24.3% | 2.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief