Global| Nov 06 2013

Global| Nov 06 2013German Orders Begin to Show Some Real Life

Summary

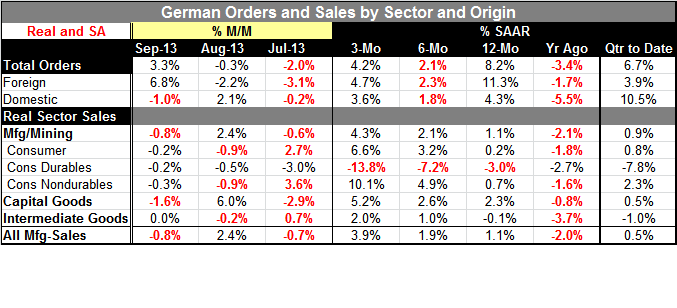

Germany's orders advanced by 3.3% in September after dropping by 0.3% in August. Foreign orders were super-charged, boosting the headline by rising by 6.8% in the month after two months of significant month-to-month losses. Domestic [...]

Germany's orders advanced by 3.3% in September after dropping by 0.3% in August. Foreign orders were super-charged, boosting the headline by rising by 6.8% in the month after two months of significant month-to-month losses. Domestic orders pulled back, falling by 1% and are dropping in two of three most recent months.

Germany's orders advanced by 3.3% in September after dropping by 0.3% in August. Foreign orders were super-charged, boosting the headline by rising by 6.8% in the month after two months of significant month-to-month losses. Domestic orders pulled back, falling by 1% and are dropping in two of three most recent months.

Viewed over a span of three-months, foreign and domestic orders have a more similar rate of growth: 4.7% for foreign orders compared to 3.6% for domestic orders. In the quarter-to-date calculations (quarter average over quarter average), domestic orders oddly outpace foreign orders by a long shot. Their gain in Q3 is at a 10.5% annual rate compared to a 3.9% annual rate for foreign orders. This is because of the somewhat odd pattern of growth that is serendipitous for domestic orders growth. Domestic orders were strong in June after a previously weak quarter. As a result the level for sales in July and the rest of the quarter was boosted even though Q2 as a whole was weak and the growth for the rest of Q3 was not exciting (three-month growth of 3.6%).

Moving away from the quarter-over-quarter figures (and looking at the graph), it is clear that foreign orders are really accelerating while domestic orders are much tamer. Over 12-months foreign orders are up by 11.3% compared to a gain of 4.3% for domestic orders. Over the previous 12-months foreign orders fell by 1.7% while domestic orders fell by a sharper 5.5%. On balance it is the foreign sector that is driving German growth. Germany seems to be ready to broaden its already large current account surplus that is becoming an issue within the EMU.

German real sector sales show that capital goods are the backbone of demand over 12-months while consumer goods sales are up by only a thin 0.2%. Intermediate goods sales are still contracting.

On balance the German economy continues to make inroads. But its strength is putting it in a position within The Community such that it appears to be prospering at the expense of fellow members. The European Community has rules regarding the permissible size of a current account deficit relative to GDP and Germany is in violation of what's allowed. The next question is going to regard what The Community is willing to do to enforce its rules. Will it act in a way that will benefit other Community members and not simply penalize the German economy for its prosperity? This is one of the interesting aspects playing out in the background that has not gotten too much attention yet. But Germany is about to become a victim of its own success.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief