Global| Nov 05 2020

Global| Nov 05 2020German Orders: Acceleration Meets Deceleration

Summary

It has not been the best of times or the worst of times, but the German economy has been rapidly rebounding from an ugly hit to economic activity in the wake of the coronavirus shutdown and after seeing orders crater then surge, the [...]

It has not been the best of times or the worst of times, but the German economy has been rapidly rebounding from an ugly hit to economic activity in the wake of the coronavirus shutdown and after seeing orders crater then surge, the order rebound now seems to be charting a milder course.

It has not been the best of times or the worst of times, but the German economy has been rapidly rebounding from an ugly hit to economic activity in the wake of the coronavirus shutdown and after seeing orders crater then surge, the order rebound now seems to be charting a milder course.

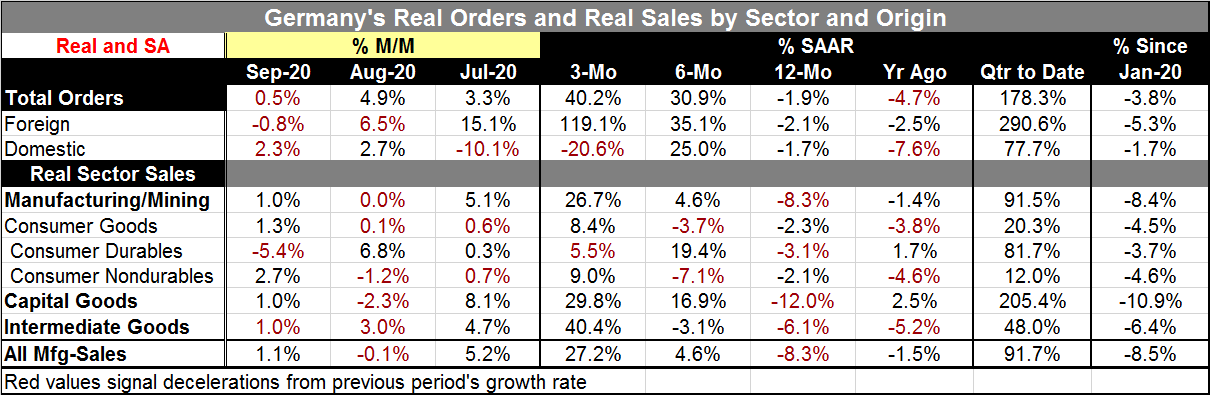

After a 26.0% drop in April, German orders gained 10.4% in May, 28.8% in June, 3.3% in July, 4.9% in August and now they rose by just 0.5% in September. Foreign orders actually fell in September.

From their April lows orders have risen 54%. Foreign orders are up 63% while domestic orders are up by a smaller 43%. In addition to their sharp fall in April, German orders generally also fell in February and March. Looking at order performance from January shows that total orders, despite this strong pick up since April, remain 3.8% below their level in January. These are real (inflation adjusted) data so there is a 3.8% decline in real terms on the books since January. That in turn implies that real orders have actually been falling at a 5.8% annualized rate over those eight months. This calculation simply puts things in perspective among the super strong data and outrageously weak data. Clearly a single growth rate of the period does not begin to describe what has happened. But despite the massive drop and impressive rebound, orders remain short of their year starting mark. Foreign orders are 5.3% below their January levels while domestic orders are 1.7% below their January level.

These growth rates help to position the level of orders for us, and that is half the battle in understanding what the net impact on the economy has been and is at the present time. But the other half of it is about momentum and momentum is hard to gauge. The table shows a number of different growth rate calculations and each one gives a very different perspective on how fast orders are moving forward. The good news is that although the year-to-date growth rate shows a net decline that is not the best way to understand momentum in these circumstances. The quarter-to-date calculation which captures growth in the just completed third quarter over the second quarter is not a good gauge either since it catches the slingshot recovery at its best relative to a depressed base. That QTD growth rate is at 178.3% on a compounded basis--substantially higher than the still excessive three-month growth rate for real orders at 40.2%.

The problem with these growth rates is that we know recovery has been in gear and we can see that it is slowing down. In the second paragraph (above) I presented month-by-month headline growth rates since May. May and June were gains at double digits. That slowed to a pace less than half that in July and August. For September, the month-to-month gain is just 0.5% and that seems much more like reality. The fast growth phase is now over.

Moreover, not only is the fast growth phase over, but there could be another setback in the works because quite apart from trying to extract trajectory from a series of oscillating growth rates we have new policies in place in Germany and across the EMU that are restricting growth again. There could be more monthly negative growth rates for orders before the end of the year. At this point, the prospect for getting December orders above their January level is not a good one. However, one thing we have learned about these shutdowns is that while they can hammer growth rates lower, once restrictions are removed, growth can make a comeback at a speed that rivals its pace of decline.

The data in the lower panel of the table on real sector sales show a more gradual recovery. These data are based on real world results and actual shipments not just order numbers scrawled in a book (or tapped into a computer). Monthly sales data show weakness over the last two months of August and September generally. The slowdown is evident here as well.

On balance, we cannot pin down a specific growth rate for orders. We know it has slowed and we know that Germany is entering another challenging period as coronavirus restrictions are back in play. These restrictions will hobble output more than crush it as happened last time because they are not being imposed on the same scale with the same severity. The message is that Europe is not out of the woods yet when it comes to its fight with the virus. But a second message is that there has been learning and there are now different and more flexible ways to deal with the virus that do not disrupt the economy by quite as much. We are looking forward to those policies having success.

Nonetheless on the day the EU Commission has issued new weaker forecasts for the euro area. Not only is Germany itself a part of this area, but German firms have a lot of industrial relationships with customers in this area. The EU now sees euro area Real GDP shrinking by 7.8% in 2020 then rebounding by 4.2% in 2021. These number represent an upgrade to growth in 2020 (from -8.7% previously) largely because the rebound was much stronger than previously expected and more complete than expected. However, the outlook for 2021 is downgraded from a previous mark of 6.1%. Growth in 2021 has been knocked down more than growth in 2020 has been boosted up. This is the result of a more somber assessment of ongoing risks from the virus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief