Global| Aug 07 2017

Global| Aug 07 2017German IP Takes a Step Backward As the German Profile Turns to One of Solid If More Moderate Growth

Summary

Germany's industrial production took an unexpected step lower in June, but its upward thrust is still in place with only the sense of relentless momentum diminished. German IP is now up by 2.5% over 12 months, at a 7.7% pace over six [...]

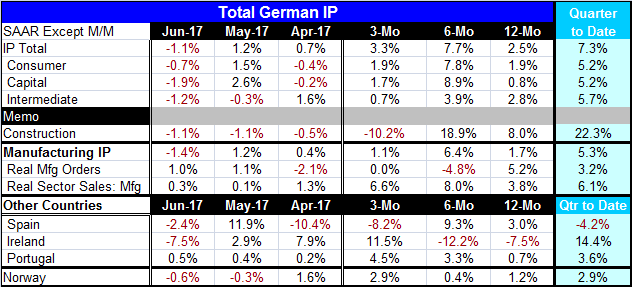

Germany's industrial production took an unexpected step lower in June, but its upward thrust is still in place with only the sense of relentless momentum diminished. German IP is now up by 2.5% over 12 months, at a 7.7% pace over six months, and at 3.3% pace over three months. Previously, the three-month pace was at an 8.4% annual rate. With the backing off in June, Germany's growth rates settle into a more moderate framework of sustainability.

Germany's industrial production took an unexpected step lower in June, but its upward thrust is still in place with only the sense of relentless momentum diminished. German IP is now up by 2.5% over 12 months, at a 7.7% pace over six months, and at 3.3% pace over three months. Previously, the three-month pace was at an 8.4% annual rate. With the backing off in June, Germany's growth rates settle into a more moderate framework of sustainability.

The drop back in output in June seems like nothing more than a resetting of the pace of output growth in Germany which otherwise would be raging at a super strong pace and inconsistent with every other measure we have of the German industrial sector and overall economy. At this point, the manufacturing sector looks solid and has expansion clearly in its grasp, but it no longer looks like it is running away from the rest of the economies in Europe.

On the month, German IP stepped back in consumer goods, capital goods and intermediate goods. Construction output is now lower for three months running. Manufacturing IP has a 1.7% rate of growth over 12 months and a 1.1% annualized pace over three months.

Manufacturing output is now lagging real sales and real orders over 12 months. Output is up by 1.7% over 12 months with real orders up by 5.2% and real sales up by 3.8%. However, if we compare these categories' sequential growth rates, there is a lot of disconnection among them over these different horizons of three-month and six-month and 12-month. For the moment, I would not judge the differences in these growth rates or signals as a problem or even as mixed signals. Orders tend to fit the output series but not tightly and they tend to lead it by three months or so. Everything signals growth, but depending on the horizon the speed signal is different. And this is normal.

On a quarter-to-date basis, all these signals are more in tune with manufacturing IP up at a 5.3% pace, real orders up at a 3.2% pace and real sales up at a 6.1% pace.

Only four other European countries have IP reported early. Three of them show IP higher on balance over 12 months with Ireland as the exception. Among them only Spain has a decline in output over three months. And only Spain has a decline in output on a quarter-to-date basis (a calculation that is for the full quarter at this point).

IP data are volatile by nature. The German year-over year series was up by 4.9% over 12 months last month; that was its strongest 12-month gain since August 2011. Having a pull-back from that pace is no surprise. At 1.7% the German manufacturing IP gain is still over twice its average pace since 2012. And at 1.7% German manufacturing IP growth is substantially stronger than the 1.1% order growth has averaged since 2012.

On balance, I don't think the June drop in German IP has any real economic meaning other than to bring its growth rates back into a one of moderation and normalcy. With this monthly setback in output, the notion of acceleration is stuffed back into the tube with the rest of the toothpaste. Other economic reports for Germany, like the Markit manufacturing PMI reading, have been positive but not effusive. These readings now all seem to coexist better as German growth is solid and it is not running way ahead of the rest of Europe as it may previously have hinted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief