Global| May 08 2015

Global| May 08 2015German IP Surprisingly Sours

Summary

German industrial output fell by 0.5% in March, a drop that was not expected. Furthermore, German exports rose by 1.2% on the month, faster than expected, driving a wedge of inconsistency between the IP and export results for the [...]

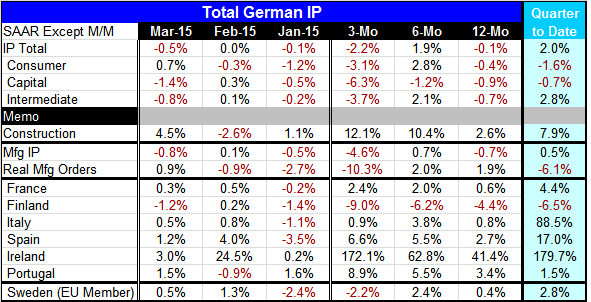

German industrial output fell by 0.5% in March, a drop that was not expected. Furthermore, German exports rose by 1.2% on the month, faster than expected, driving a wedge of inconsistency between the IP and export results for the month. German manufacturing PMI data have been weak and Germany is among many countries in the EMU that have been seeing their economic strength created in the services sector, not in manufacturing. This month's manufacturing data underline that result as IP in the manufacturing sector fell by 0.8% and is falling at a 4.6% annual rate over the last three months with real orders even weaker.

German industrial output fell by 0.5% in March, a drop that was not expected. Furthermore, German exports rose by 1.2% on the month, faster than expected, driving a wedge of inconsistency between the IP and export results for the month. German manufacturing PMI data have been weak and Germany is among many countries in the EMU that have been seeing their economic strength created in the services sector, not in manufacturing. This month's manufacturing data underline that result as IP in the manufacturing sector fell by 0.8% and is falling at a 4.6% annual rate over the last three months with real orders even weaker.

With the euro exchange rate so weak and Germany as such a competitive economy, the manufacturing weakness has been surprising. At least this month brings some strength to exports that we expect to do better in this low euro-exchange rate environment. German exports now are outpacing imports (not a great stretch since imports are not even up 2% year-over-year) and moving ahead at a 5.1% pace. Still, this growth rate is down from 8.4% a year ago in March. The exchange rates magic simply isn't working as well as expected and that has to do with the very weak global environment. Japan has been encountering the same difficulty and has begun only recently to see some real export lift.

German IP is up in the just concluded quarter rising at a 2% annual rate. And manufacturing output is also up at a weak 0.5% annual rate. Construction output is especially strong, rising at a 7.9% annual rate in Q1 2015. Apart from that, the strength in IP is mostly in intermediate goods as consumer goods output and capital goods output both are falling in the quarter. Real manufacturing orders are net lower in Q1, falling at a 6.1% annual rate. That doesn't exactly encourage us to have an upbeat outlook despite the weak euro and all the ECB stimulus.

Other EMU Members

Looking at other early IP reporters in the euro area, we find of six reporters five have IP improving on the month - all but Finland. Even France has IP gaining in March, rising by 0.3% in the month for its second gain in a row and a rise at a 4.4% pace in Q1 2015 to boot. In fact, only Finland, among this group, fails to have IP growth in Q1. Portugal shows a small gain while Italy, Spain and Ireland are showing gains that range from extremely strong to spectacular. But the muted overall gain for IP in the EMU as a whole tells us that this sort of strength is mostly in the smaller countries with smaller weights in the EMU since the overall EMU gain in Q1 is quite modest at 2%.

On balance, there are some hopeful signs for the EMU. At least IP is still growing and some of the members that had been struggling the most are now getting their industrial sector back in gear. But the large EMU member economies, especially Germany, still seem to be floundering. We highlighted in a report yesterday that Germany is seeing too much weakness in its foreign orders to justify a very buoyant outlook for Germany, the EMU or the global economy. We expect Germany, one of the most powerful and competitive advanced economies in the world, to benefit from the low EMU exchange rate. When we instead are presented with prevaricating industrial data and a still-unimpressive export report, it is a reason to pause and reassess the outlook. Today's data remain in that camp. This report still requires further explanation- unless the explanation is that the global economy really is slowing down despite all of the best efforts to revive growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief