Global| Sep 05 2014

Global| Sep 05 2014German IP Recovers

Summary

Germany's industrial production rose by 1.9% in July, marking a strong gain in the German industrial sector. It is the largest monthly gain since April 2013. The output of consumer goods rose by 0.1%. Intermediate goods output rose by [...]

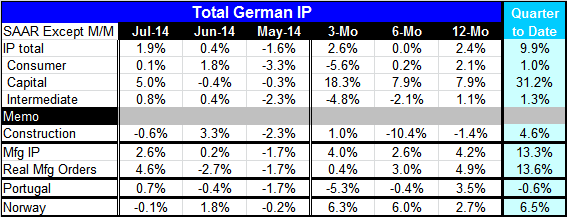

Germany's industrial production rose by 1.9% in July, marking a strong gain in the German industrial sector. It is the largest monthly gain since April 2013. The output of consumer goods rose by 0.1%. Intermediate goods output rose by 0.8%. The gain was led by a surge in capital goods output, which rose by 5% in July after falling by 0.4% in June and failing to rise for five consecutive months.

Germany's industrial production rose by 1.9% in July, marking a strong gain in the German industrial sector. It is the largest monthly gain since April 2013. The output of consumer goods rose by 0.1%. Intermediate goods output rose by 0.8%. The gain was led by a surge in capital goods output, which rose by 5% in July after falling by 0.4% in June and failing to rise for five consecutive months.

The gain in the industrial production leaves the sector rising at a 2.6% annual rate over three months, up sharply from its flat performance over six months; its 2.6% gain is slightly higher than its 12-month pace of 2.4%.

In the quarter to date, output is dazzling in the face of what had been weak economic data all around. Overall output is rising at a 9.9% annual rate in the quarter to date, which involves compounding the current month's level in July over the average level of output in the second quarter. Such calculations can be extreme and may not be indicative of the quarter's path. Still, they are useful. In Q3, overall IP growth is driven by the exceptional growth in capital goods output which is up at a 31% annual rate, on the quarter-to-date basis in the quarter. Meanwhile, consumer goods output and intermediate goods output both are growing between 1% and 1.5% in the quarter, much more indicative of the current situation in Germany and in Europe.

The European Central Bank, just a day earlier, had decided to step up its program of accommodation with Bundesbank President Jens Weidmann apparently in dissent. Weidmann wanted to wait for further results from the past programs launched by the ECB, and as we can see from the data, the German economy would seem to be fine with a wait-and-see policy. However, German Finance Minister Wolfgang Schauble has also just announced that it looks that Germany, instead of being above its 1.8% growth objective for this year, will be below it. Germany, too, is being affected by the sluggishness in Europe. The rest of Europe has a much more pressing need for the kind of the stimulus being offered up by the ECB.

In the table, we only see two other early reporters of industrial production data, Norway and Portugal. They do not offer much insight on the assessment of what the European economy is doing, as one of them is weak in the quarter to date and one of them is quite strong.

However, even for Germany, the strong surge in capital goods output leads an industrial sector that is otherwise struggling. Moreover, the July surge seems out of character with past German trends and out of step with current trends in Europe. Germany's revival does not seem to be destined to last because it does not have a broad base of support.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.